Learning Outcomes

After reading this article, you will be able to identify the responsibilities of auditors and management regarding the going concern basis, explain common indicators casting doubt on going concern status, describe required audit procedures, and distinguish between adjusting and non-adjusting subsequent events. You will also understand the reporting implications of going concern uncertainties for the auditor’s report, as required by ISA 570.

ACCA Audit and Assurance (AA) Syllabus

For ACCA Audit and Assurance (AA), you are required to understand how going concern, subsequent events, and related audit procedures affect opinion formation and audit completion. This article covers:

- The concept and significance of the going concern assumption and the relevant responsibilities of both management and auditor.

- Common indicators that an entity may not be considered a going concern (typical warning signs).

- The specific procedures auditors must perform when going concern doubts arise (ISA 570).

- The difference between adjusting and non-adjusting subsequent events.

- The reporting implications for the audit opinion and auditor’s report where material uncertainties exist.

- The nature and purpose of written representations concerning going concern.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- List three possible indicators that cast doubt on an entity's ability to continue as a going concern.

- Explain the difference between an adjusting and a non-adjusting event after the reporting date.

- State two audit procedures required by ISA 570 if there are doubts about the going concern basis.

- What should an auditor do if a material uncertainty exists regarding going concern and management has made adequate disclosure?

Introduction

The going concern concept requires financial statements to be prepared on the basis that the business will continue operations for at least the next 12 months. Auditors must evaluate management’s assessment of going concern, perform procedures to identify events or conditions that may cast doubt over this assumption, and determine whether disclosures are adequate. ISA 570 Going Concern guides the auditor’s responsibilities in this area, including necessary responses, audit evidence, and potential implications for the audit opinion.

Key Term: going concern

The assumption that an entity will continue in business for the foreseeable future—typically at least twelve months from the date of the financial statements.

GOING CONCERN—CONSIDERATIONS AND RESPONSIBILITIES

Responsibilities for Going Concern

Management is responsible for assessing whether the business can continue as a going concern and for preparing or disclosing any material uncertainties. The auditor’s duty is to obtain sufficient appropriate evidence regarding the appropriateness of the going concern basis and to conclude if material uncertainty exists.

Key Term: material uncertainty

A circumstance where the magnitude and likelihood of an event could cast significant doubt on the entity’s ability to continue as a going concern, requiring disclosure for fair presentation.

Common Indicators of Going Concern Issues

Entities may show signs suggesting doubt over their going concern status. These indicators fit into financial and operational categories.

Financial indicators

- Net liabilities or negative equity

- Overdrafts or borrowings at, or near, their maximum limits

- Loan defaults or breaches of covenants

- Negative cash flows, recurring losses, or inability to pay debts when due

Operational and other indicators

- Loss of key customers, suppliers, or staff

- Pending legal actions that may result in substantial liabilities

- Unplanned sale of assets to generate cash

- Reluctance of suppliers to provide credit

- Major catastrophes uncovered by insurance

Worked Example 1.1

Scenario: As auditor for Dune Ltd, you identify that the company breached its loan agreement, has negative cash flows, and delayed supplier payments post-year end.

Answer:

You have detected classic financial going concern indicators—breach of loan covenants, cash shortages, and overdue payables. These signs should lead you to perform procedures focusing on liquidity and future cash flows. Key Term: indicators of going concern

Conditions or events that may suggest significant doubt about the entity’s ability to continue as a going concern, requiring further investigation.

AUDITOR PROCEDURES (ISA 570)

Evaluating Management’s Assessment

The auditor must understand and evaluate management’s going concern assessment period, fundamental assumptions, and plans to remedy potential issues. This includes considering events and conditions up to the date of the auditor’s report.

Required Audit Procedures

- Analyse cash flow forecasts, budgets, and future trading estimates; check the reliability of management’s forecasts by reviewing past performance.

- Assess compliance with loan and other agreements.

- Enquire with management about plans for future actions (e.g., cost cutting, raising finance).

- Examine post-reporting date events, board minutes, correspondence with lenders.

- Obtain written representation on management’s view and plans.

Key Term: written representation

A written statement provided by management to the auditor, confirming matters or supporting audit evidence, such as the appropriateness of the going concern basis.

Additional Actions If Doubt Exists

- Seek external confirmation of support from banks, investors, or group companies.

- Investigate post-year-end receipts and payments for evidence of improved or deteriorated liquidity.

- Consult legal advisors if legal or regulatory issues are involved.

- Review correspondence with suppliers or lenders for evidence of strain or renegotiation.

Worked Example 1.2

Question: You discover that Everest Co has negative cash flows, is heavily reliant on a single customer now in liquidation, and is struggling to secure fresh financing. List three audit procedures you should perform regarding going concern.

Answer:

- Assess cash flow forecasts and the assumptions used.

- Obtain confirmation from potential financiers or review negotiations for new credit.

- Review post-year-end bank statements and sales to see if income sources are recovering or further deteriorating.

Exam Warning: Be careful not to conclude on going concern based solely on one indicator. Always evaluate the overall situation, combining financial and operational evidence, and assess the adequacy of management plans and disclosures.

SUBSEQUENT EVENTS—IMPACT ON GOING CONCERN

ISA 560 requires the auditor to consider events between the reporting date and the auditor’s report signing date. Some of these subsequent events may confirm existing concerns over going concern or create new uncertainties.

Key Term: subsequent events

Events occurring between the date of the financial statements and the date the auditor’s report is signed, which may affect the financial statements or the auditor’s conclusions.

There are two categories:

- Adjusting events: Provide evidence of conditions that existed at the period end (e.g., customer insolvency relating to a balance at year-end).

- Non-adjusting events: Indicate conditions arising after the period end (e.g., fire destroying inventory after the year-end).

Key Term: adjusting event

An event after the reporting date giving evidence of conditions that existed at period-end and requiring adjustment of the financial statements. Key Term: non-adjusting event

An event after the reporting date relating to conditions arising after period-end; disclosed if material but not adjusted in the accounts.

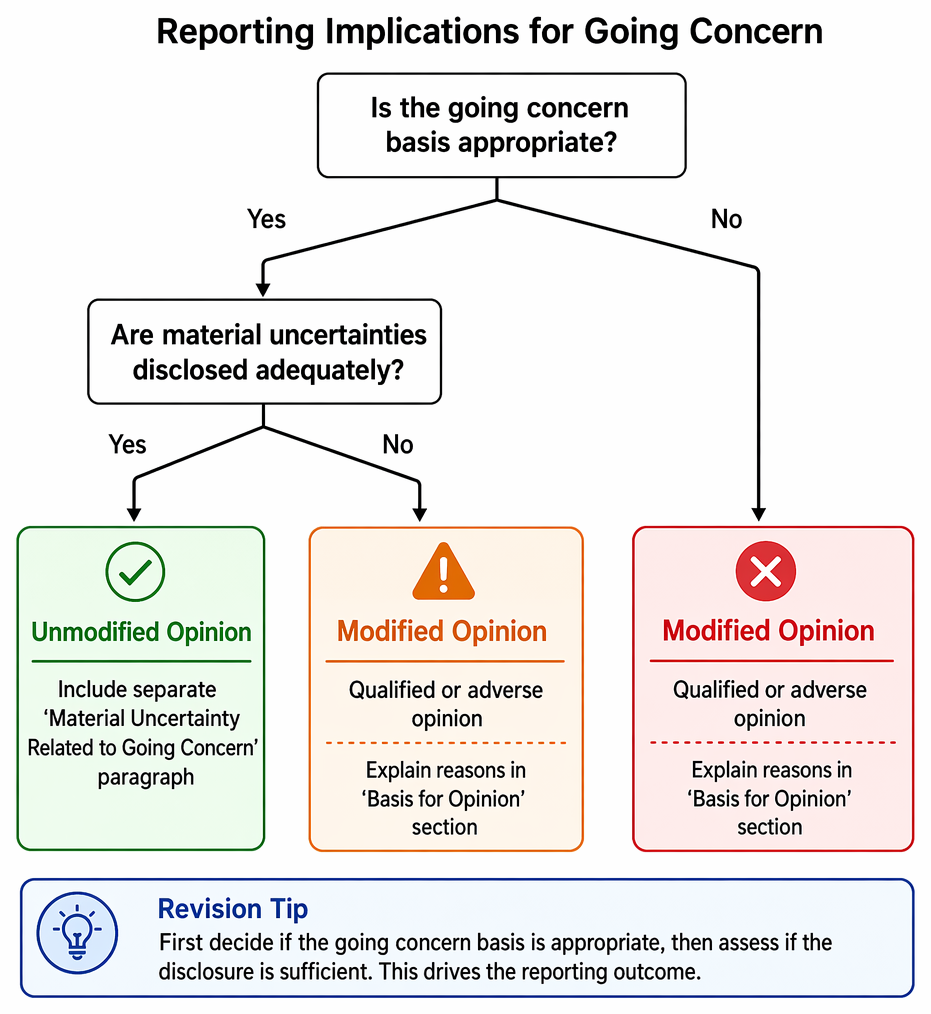

REPORTING IMPLICATIONS

Post-reporting-date events are assessed for period-end conditions, leading to financial statement adjustment or material disclosure and review of going concern effects.

Adequate Disclosure Made

When management has disclosed material uncertainties and the auditor agrees with the going concern basis, the auditor issues an unmodified opinion but includes a separate “Material Uncertainty Related to Going Concern” paragraph to highlight the risk.

Inadequate Disclosure or Inappropriate Basis

If disclosures are missing or inadequate, or the going concern basis is wrongly applied, the auditor must modify the opinion (qualified or adverse), explaining the reasons in the “Basis for Opinion” section.

Worked Example 1.3

Scenario: Moss Co’s cash flow forecasts indicate survival depends on a successful rights issue. The directors disclose this uncertainty fully in the notes.

Answer:

The auditor should issue an unmodified opinion and draw attention to the material uncertainty via a “Material Uncertainty Related to Going Concern” section in their report.Revision Tip: For exam questions on reporting, first decide if the going concern basis is appropriate, then assess if the disclosure is sufficient. This drives whether the opinion stays unmodified, is modified, or includes additional reporting paragraphs.

Summary

- Going concern means preparing accounts as if the business will continue trading into the foreseeable future.

- Auditors must look for indicators that challenge this assumption and carry out ISA 570 procedures.

- Typical warning signs include persistent losses, liquidity issues, overdue debts, loan covenant breaches, and loss of key customers or suppliers.

- Management must disclose any material uncertainties. If they do so and the basis remains appropriate, the audit opinion is unmodified but a dedicated paragraph alerts users to the uncertainty.

- If adequate disclosure is not made, the auditor must qualify or disclaim their opinion.

- Subsequent events discovered before the report date may alter the auditor’s assessment or require changes to disclosures.

Key Point Checklist

This article has covered the following key knowledge points:

- Define going concern and explain why it matters for financial statement preparation and audit.

- State management and auditor responsibilities regarding going concern.

- List common indicators that suggest going concern problems.

- Outline the audit procedures required by ISA 570 when going concern is in question.

- Distinguish between adjusting and non-adjusting subsequent events and describe how each affects financial statements and the audit.

- Summarise the reporting implications for the auditor’s opinion when a material uncertainty exists.

Key Terms and Concepts

- going concern

- material uncertainty

- indicators of going concern

- written representation

- subsequent events

- adjusting event

- non-adjusting event