Learning Outcomes

After reading this article, you will be able to explain what real options are and why they add value to project appraisal. You will understand how to recognise real options in staged investments, describe how learning effects influence financial decisions, and apply basic real option valuation using option pricing models such as Black-Scholes. You should be able to evaluate the impact of flexibility on project value and identify relevant ACCA exam requirements.

ACCA Advanced Financial Management (AFM) Syllabus

For ACCA Advanced Financial Management (AFM), you are required to understand the application of real options in investment appraisal, especially for projects involving uncertainty or staged commitment. Focus your revision on the following syllabus points:

- Explain the concept of real options and distinguish them from financial options

- Identify and evaluate real options in major projects, such as the option to delay or stage investments

- Assess the financial impact of incorporating learning effects and flexibility into appraisal decisions

- Use option pricing techniques, including the Black-Scholes model, for valuing simple real options

- Advise on how real options and learning may alter project value and investment decisions

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is a real option in the context of capital investment?

- Why would a company stage an investment rather than commit all at once?

- True or false? The presence of learning effects increases the potential value of a real option embedded in a project.

- What are the five primary variables required to value a real option using the Black-Scholes model?

- Briefly explain how the option to delay investment can change the net present value of a project.

Introduction

Conventional investment appraisal techniques such as Net Present Value (NPV) and Internal Rate of Return (IRR) do not always capture the flexibility and strategic value available in uncertain, multi-stage investments. Real options analysis allows financial managers to account for the value of flexibility—particularly where management can stage investments and learn from market feedback or technical progress before fully committing additional resources.

In this article, we discuss the core concepts of real options, examine how staging and learning create value, outline how to identify embedded options, and highlight the practical steps required for valuation in the ACCA AFM exam.

Key Term: real option

A right, but not an obligation, for management to make a future business decision—such as delaying, expanding, reducing, or abandoning a project—based on information that becomes available after the initial investment.

THE VALUE OF FLEXIBILITY IN INVESTMENT APPRAISAL

NPV calculations typically assume that all investment decisions are made upfront with no opportunity to revise course. In reality, large projects often progress through multiple stages. Management has the ability to alter future investments based on observed performance, market changes, or technological developments—this flexibility adds financial value.

Key Term: investment staging

Dividing a project into sequential phases where a decision to move to the next phase depends on the success or information gained from earlier stages. Key Term: learning effect

The process by which new information obtained during a project phase updates future forecasts, reducing uncertainty and allowing more informed decision-making.

The main types of real options relevant to investment appraisal include:

- Option to delay or defer investment

- Option to expand or scale up the project

- Option to abandon or cut losses

- Option to redeploy assets to alternative uses

Projects with higher uncertainty, especially in emerging industries or R&D-intensive sectors, benefit most from real options analysis.

How Staging and Learning Create Value

Staging allows management to commit a portion of the capital initially, conserving resources until key uncertainties are resolved. If early results are positive, the company can proceed; if not, it can avoid further losses. The learning gained from initial phases makes subsequent appraisal more accurate.

A traditional NPV may undervalue such projects, as it ignores learning and flexibility. Incorporating real options can transform a negative or marginal NPV into a valuable investment opportunity.

IDENTIFYING AND VALUING REAL OPTIONS

Real options analysis in project appraisal identifies timing, expansion, abandonment and redeployment flexibility as sources of incremental project value.

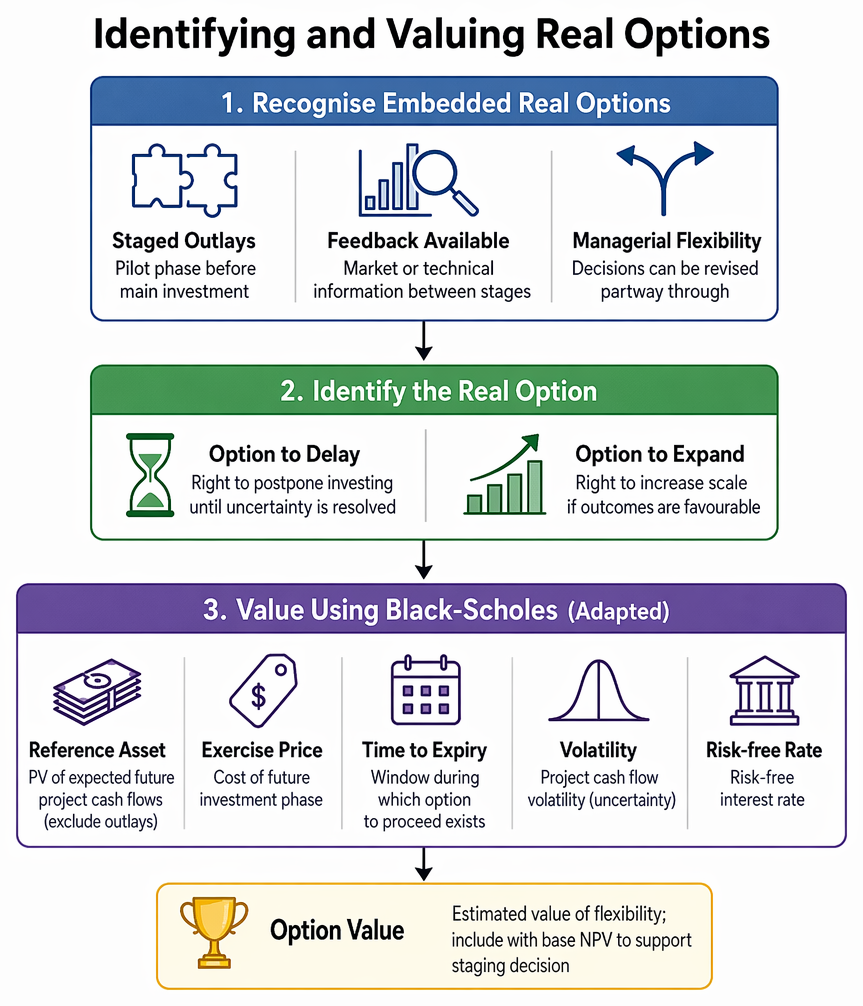

Recognising Embedded Real Options

Look for investments where:

- Outlays can be split into pilot and main phases

- Market or technical feedback is available between stages

- Management decisions can be revised partway through the project

Key Term: option to delay

The right to postpone committing funds until uncertainties are resolved, without losing the opportunity to invest later. Key Term: option to expand

The right to increase the scale of operations if initial outcomes are favourable.

Valuing Real Options Using Black-Scholes

Many real options have characteristics similar to financial options (calls and puts). For basic applications, the Black-Scholes option pricing model is adapted as follows:

Inputs required:

- Value of the reference asset (typically the present value of expected future project cash flows, excluding investment outlays)

- Exercise price (cost of future investment phase)

- Time to expiry (window during which the option to proceed is available)

- Project cash flow volatility (reflecting uncertainty)

- Risk-free interest rate

Where the option is to delay, the firm has a call option: it can choose whether, and when, to invest based on subsequent developments.

Worked Example 1.1

A technology firm can launch a new product in two phases. An initial $3m prototype phase will allow market feedback; a further $12m launch is possible after one year. If the full market launch occurs, the present value of future net cash inflows is projected at $15m (however, these are highly uncertain; assume a volatility of 35%), and the risk-free rate is 4%. What is the value of the option to launch commercially after seeing the prototype results?

Answer:

The firm holds an option to invest $12m (exercise price) for a possible $15m value (asset value). Using the Black-Scholes model, with time to expiry of 1 year, you would input these variables and the given volatility. The calculated option value represents the price management should be willing to pay for this flexibility. If the traditional NPV without option value is not attractive, but the option value is substantial, the staged approach may now be justified.

Worked Example 1.2

A mining company may commit $4m now to an exploratory phase with an option to expand production after geological results. If the expansion outlay is $8m, but only committed if signs are positive, and the PV of expected additional returns at the time is $9m, volatility is estimated at 30%, and the option expires in 18 months. Should the firm take the exploratory phase?

Answer:

By treating the right to invest $8m for $9m as a real call option expiring in 1.5 years, Black-Scholes valuation will estimate the value of this expansion right. If the benefit added by the option (plus the base project NPV) makes the first stage acceptable, proceeding with the exploratory phase is supported.Exam Warning: Be sure to justify clearly why an investment qualifies as a real option scenario. In the exam, marks are available for recognising the conditions under which option pricing applies—such as uncertainty, ability to stage, and presence of managerial flexibility.

Revision Tip: In calculations, always state all five Black-Scholes input variables clearly. If volatility is not provided, explain how it would be estimated in practice (e.g., using historical industry returns).

Summary

Staging investments and incorporating real options enable management to quantify the strategic value gained from flexibility and information. Learning during early project phases informs subsequent choices and may considerably increase overall project value. For ACCA Advanced Financial Management (AFM), being able to describe, identify, and value real options using option pricing models is essential for exam success.

Key Point Checklist

This article has covered the following key knowledge points:

- Define real options and explain their relevance to staged investments

- Describe investment staging and the learning effect in project appraisal

- Identify the main types of real options in capital budgeting decisions

- Apply option pricing concepts, including Black-Scholes, to real option valuation

- Recognise ACCA exam requirements in real option scenarios

Key Terms and Concepts

- real option

- investment staging

- learning effect

- option to delay

- option to expand