Learning Outcomes

After reading this article, you will be able to identify the key features of Islamic finance as a source of capital for organisations. You will understand the main Islamic finance contracts, their adherence to Sharia principles, and how they differ from conventional debt and equity. You should be able to evaluate the benefits and limitations of these instruments and assess their suitability for corporate financing strategies in the context of ACCA AFM exam scenarios.

ACCA Advanced Financial Management (AFM) Syllabus

For ACCA Advanced Financial Management (AFM), you are required to understand the role and practical application of Islamic finance. In particular, revision should focus on the following areas:

- The rationale for Islamic finance in corporate funding and the prohibition of riba (interest)

- The main types of Islamic financial contracts: murabaha, ijara, sukuk, mudaraba, musharaka, salam, and istisna

- Sharia compliance requirements and the function of Sharia boards

- Advantages and limitations of Islamic finance instruments for companies

- How Islamic finance affects capital structure, risk, and tax treatment

- The impact of Islamic finance on the financial position and reported results of an organisation

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is prohibited under Sharia law in Islamic finance?

- a) Equity investment

- b) Interest-bearing loans

- c) Asset-backed leasing

- d) Partnership-based profit sharing

-

True or False? Sukuk are Islamic financial instruments most similar in function to conventional bonds, but grant investors asset ownership rather than debt claims.

-

Briefly explain the key difference between a murabaha contract and a conventional bank loan.

-

List two risks or limitations faced by organisations when using Islamic finance compared to conventional finance.

Introduction

Islamic finance has become an important consideration in global corporate funding strategies. Unlike conventional finance, Islamic funding methods must comply with Sharia law, which prohibits interest (riba), excessive uncertainty (gharar), and investment in certain activities. Corporations seeking funds from Islamic sources must use contracts that channel funds into productive assets or ventures, sharing profit and loss between participants. Understanding these instruments is essential for ACCA AFM candidates, both for technical calculations and for strategic recommendations involving a diverse range of financial options.

Key Term: Sharia compliance

The requirement that all financial transactions conform to Islamic law, including bans on interest and speculation, and restrictions to approved economic activities. Key Term: riba

The charging or payment of interest on loans or deposits, expressly forbidden in Islamic finance. Key Term: gharar

Excessive uncertainty or ambiguity in contractual terms, which is also not permitted under Islamic law.

ISLAMIC FINANCE PRINCIPLES

Islamic finance ensures transactions are underpinned by ethical and social values. The central tenets include:

- Prohibition of riba (interest)

- Avoidance of gharar (prohibited uncertainty/speculation)

- Asset-backing: financing must relate to real assets

- Profit and loss sharing between parties

- Restriction from investing in sectors considered harmful or unethical (e.g. alcohol, gambling)

To oversee compliance, Islamic financial institutions employ independent Sharia boards.

Key Term: Sharia board

A panel of Islamic scholars and financial experts who review and authorise financial products and ensure adherence to Sharia principles.

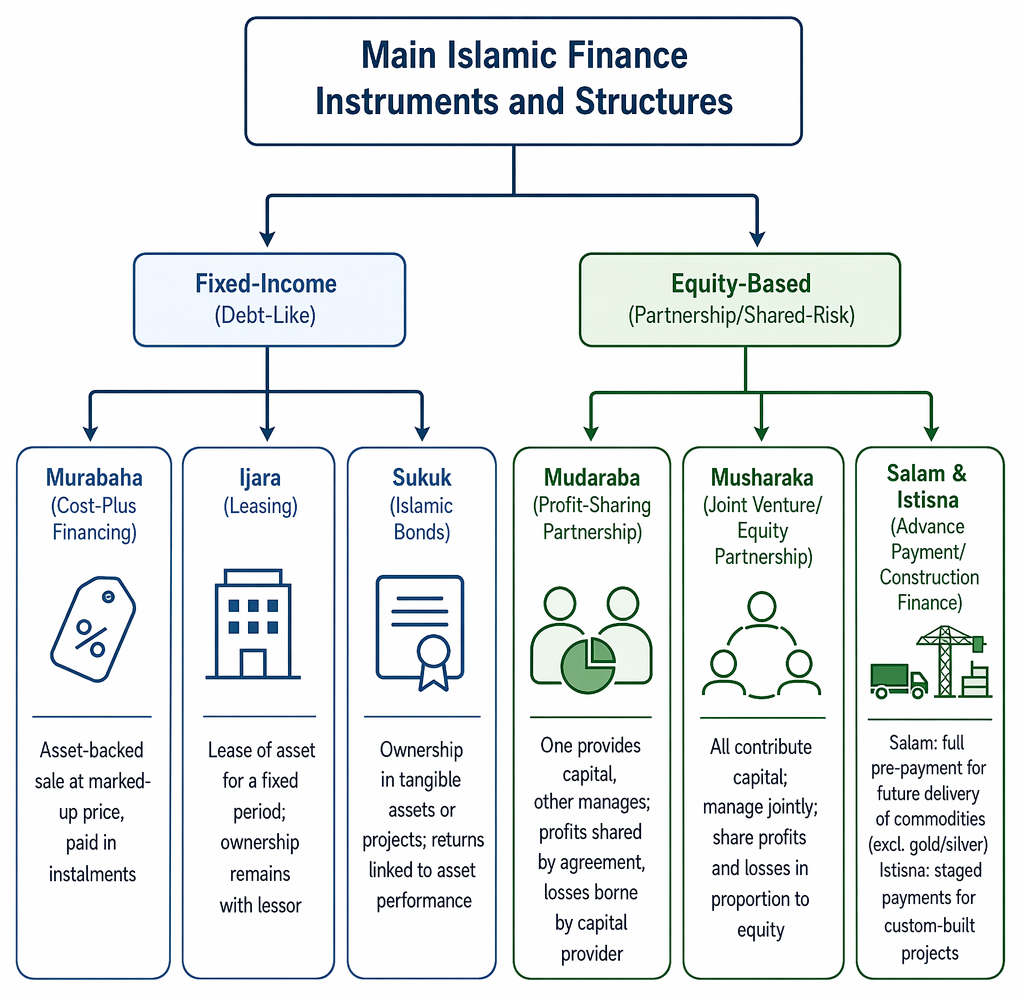

MAIN ISLAMIC FINANCE INSTRUMENTS AND STRUCTURES

Islamic finance contracts can be categorised as either fixed-income (debt-like) or equity-based (partnership/shared-risk). The most common contract types include those below.

Murabaha contract mechanics depict bank purchase, cost-plus resale with profit fixed at inception, instalment payments, and contractual transfer of title and risk.

Murabaha (Cost-Plus Financing)

In a murabaha transaction, the finance provider purchases an asset on behalf of the client and sells it at a marked-up price, payable in instalments. The profit is agreed upfront, and no further charges (interest or penalties) can be added.

Key Term: murabaha

An asset-backed sales contract where a bank buys goods and resells to a client with a disclosed profit margin, repaid over time.

Ijara (Leasing)

Ijara involves a lease agreement for an asset, typically equipment or property. The lessor retains ownership and is responsible for major maintenance, while the lessee pays rental fees for use.

Key Term: ijara

A leasing arrangement in which one party makes use of an asset for a fixed period in exchange for payment, without transfer of legal ownership.

Sukuk (Islamic Bonds)

Sukuk allow investors to participate in ownership of tangible assets or projects and receive a share of profits generated. Unlike conventional bonds, sukuk holders possess an interest in the associated assets, not a debt claim.

Key Term: sukuk

Islamic financial certificates granting partial ownership in the associated assets, with returns linked to asset performance instead of interest payments.

Mudaraba (Profit-Sharing Partnership)

Under mudaraba, one party provides the capital and the other performs entrepreneurial or managerial services. Profits are shared according to a predetermined ratio, while losses are borne only by the capital provider.

Key Term: mudaraba

A profit-sharing partnership where one party supplies capital and the other manages the business, with profits shared by agreement.

Musharaka (Joint Venture/Equity Partnership)

All parties contribute capital to a musharaka, managing ventures jointly and sharing both profits and losses in proportion to equity contributed.

Key Term: musharaka

An equity-based partnership where all participants provide capital, share operations, and split profits and losses as agreed.

Salam and Istisna (Advance Payment/Construction Finance)

Salam permits full pre-payment for future delivery of commodities (apart from gold or silver). Istisna is used for construction contracts, allowing staged payments for assets built to client specifications.

Key Term: salam

A forward contract where full payment is made in advance for a specified commodity to be delivered at a future date. Key Term: istisna

A contract for commissioned manufacturing or construction, with deferred or progressive payments tied to project milestones.

COMPARISON WITH CONVENTIONAL FINANCE

Islamic financial instruments differ fundamentally from mainstream loans and bonds:

- No interest or penalty interest is chargeable.

- Finance must relate to identifiable real assets or ventures.

- Returns are linked to asset performance or pre-agreed profit-sharing.

- Certain contract structuring creates risk-sharing between parties, rather than fixed or guaranteed returns.

Worked Example 1.1

Company A needs to finance $500,000 for new equipment. The finance provider suggests murabaha. Outline the process and key accounting impact.

Answer:

The bank purchases the equipment for $500,000, then sells it to Company A for $550,000, payable over three years in instalments. The $50,000 profit is agreed at outset and is not interest. Company A records an asset at $550,000 and recognises expenses as per instalment payments. The arrangement is Sharia compliant and avoids riba.

Worked Example 1.2

A manufacturing business plans to raise $10 million for expansion through sukuk. How would this differ from issuing a conventional bond?

Answer:

Investors in sukuk acquire a share in the assets or project being financed, such as factory premises or production equipment. Instead of periodic interest, sukuk holders receive a share of periodic income generated by these assets (such as lease rentals or profits). Ownership is evidenced by certificates, and principal is repaid from asset proceeds, not simply by a promise to pay interest and return capital at maturity.

ADVANTAGES AND LIMITATIONS OF ISLAMIC FINANCE

Potential Advantages:

- Diversifies funding sources, attracting capital from markets seeking Sharia-compliant investments

- Imposes ethical restrictions, limiting reputational and compliance risk

- Financing is often structured as asset-backed, potentially reducing default risk

- Encourages long-term risk and profit sharing

Limitations and Risks:

- Approval by the Sharia board is required, possibly delaying product launches

- Some structures can be more expensive, owing to complexity or the cost of legal compliance

- Tax treatment (especially regarding deductibility of payments) may be less favourable than for conventional debt, unless local law provides equivalent treatment

- Interpretation of Sharia can differ between jurisdictions, creating inconsistency

- Instruments may be less flexible, cannot always be traded freely

Exam Warning: Attempting to disguise conventional interest-bearing lending as a Sharia-compliant transaction (so-called "window dressing") will not gain approval and creates risk of non-compliance. All contractual documentation must reflect true asset-backing or profit-sharing, not merely replicate loan terms.

Revision Tip: For AFM, you must be able to contrast the basic features of murabaha, ijara, sukuk, mudaraba, and musharaka, and recognise which solutions are appropriate in practical funding scenarios.

Summary

Islamic finance provides companies with alternative sources of funding through contracts that comply with Sharia law, strictly prohibiting interest and requiring asset-backing or profit-sharing. Each instrument—such as murabaha, ijara, sukuk, mudaraba, and musharaka—has specific structures, benefits, and limitations. These should be assessed when advising on capital structure or evaluating funding proposals in the exam.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the central principles and prohibitions of Islamic finance (riba, gharar, Sharia compliance)

- Identify the main Islamic finance contracts (murabaha, ijara, sukuk, mudaraba, musharaka, salam, istisna)

- Describe how each contract operates and how returns are generated for funders and users

- Evaluate the advantages and limitations of Islamic financing for companies

- Recognise common exam pitfalls, such as misclassifying profit as interest or misunderstanding instrument tax treatment

Key Terms and Concepts

- Sharia compliance

- riba

- gharar

- Sharia board

- murabaha

- ijara

- sukuk

- mudaraba

- musharaka

- salam

- istisna