Learning Outcomes

After reviewing this article, you will be able to calculate and evaluate Return on Investment (ROI), Residual Income (RI), and Economic Value Added (EVA) for divisional performance. You will understand how short-termism and investment myopia arise from certain performance measures. You will compare the features, strengths, and weaknesses of these methods and apply them critically to ACCA APM exam questions.

ACCA Advanced Performance Management (APM) Syllabus

For ACCA Advanced Performance Management (APM), you must understand how divisional performance measures affect managerial behaviour and strategic decision-making. This article focuses on:

- Calculation and interpretation of ROI, RI, and EVA for divisional performance appraisal

- Strengths and weaknesses of these financial measures, including their impact on goal congruence and dysfunctional decision-making

- The risk of short-termism and investment myopia from poorly designed incentive systems

- The role of value-based management (VBM) in aligning divisional and shareholder objectives

- Strategies to mitigate short-term decision-making risks using appropriate appraisal techniques

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

When a manager is rewarded solely on divisional ROI, what is a likely behavioural risk?

- a) Overinvestment in all available projects

- b) Rejection of projects that would increase shareholder value

- c) Perfect alignment with long-term strategy

- d) Strong focus on innovation and training

-

Which of the following best describes a positive Residual Income (RI)?

- a) The division earns less than the cost of capital

- b) The division is generating value above the required return

- c) The division has increased next year’s budget

- d) The division’s ROI is automatically satisfactory

-

True or false? Economic Value Added (EVA) requires adjustments to accounting profits and capital to reflect economic reality.

-

Briefly define "investment myopia" and explain how it may affect divisional managers’ decisions.

Introduction

Financial measures for divisional performance play a critical role in shaping managerial decisions. However, measures like ROI can encourage managers to focus too narrowly on the short term, potentially rejecting value-adding investments. This article explains how ROI, RI, and EVA are calculated and applied, examines their advantages and limitations, and analyses their behavioural effects—especially the problems of short termism and investment myopia. The role of value-based performance management and risk mitigation strategies will also be discussed.

Key Term: Return on Investment (ROI)

ROI is the ratio of divisional operating profit to the capital employed, shown as a percentage. It measures the efficiency of generating profits from investments made.

ROI: Calculation, Application, and Limitations

Calculating ROI

ROI is calculated as: ROI = (Operating Profit / Capital Employed) × 100% Capital employed should reflect the assets under divisional management, including appropriate profit figures as per divisional responsibility.

Strengths and Weaknesses of ROI

- Simple, widely understood and facilitates comparisons between divisions.

- Encourages managers to focus on asset utilisation.

- However, ROI can lead to dysfunctional behaviour:

- Managers may reject projects with returns lower than current ROI, even if above the cost of capital.

- Older divisions with depreciated assets may report artificially high ROI.

- ROI-based targets encourage short-term cost-cutting at the expense of investment.

Key Term: Investment myopia

A tendency for managers to avoid or postpone projects which are profitable in the long term because they negatively affect short-term performance measures.

Worked Example 1.1

A division has capital employed of $600,000 and operating profit of $120,000 (ROI = 20%). A project requiring $100,000, earning $15,000 (ROI = 15%), is available. The company's hurdle rate is 10%. Should a manager appraised solely on ROI accept this project?

Answer:

The new project will reduce average divisional ROI to 19.3%, below its current level. The manager may therefore reject the investment to protect personal performance, even though its return exceeds the company's 10% cost of capital. This is dysfunctional from the group’s viewpoint.

Short Termism and Dysfunctional Decisions

Managers rewarded only for one-year profit or ROI are incentivised to:

- Delay or cancel long-term investments that harm current ratios

- Cut costs in areas such as R&D or marketing that are essential for the future

- Hold outdated assets to report higher ROI as asset value falls

These short-sighted actions threaten strategic goals.

Worked Example 1.2

A divisional manager’s bonus is based on annual ROI. A sizeable IT upgrade has a payback after 4 years but reduces current ROI. What decision might the manager take, and why?

Answer:

The manager may delay or reject the upgrade, harming the division’s future competitiveness, to preserve a high ROI for the current bonus period—demonstrating investment myopia.

Residual Income (RI): Addressing ROI’s Problems

RI aims to solve several flaws of ROI appraisal by considering the cost of capital as a threshold for value creation.

Key Term: Residual Income (RI)

RI is the operating profit remaining after deducting a notional charge for the capital employed, at the company’s required rate of return.

Calculating RI

RI = Operating Profit – (Capital Employed × Required Rate of Return) A positive RI means the division is adding value above the capital cost.

Advantages of RI

- Promotes acceptance of all projects with returns above the cost of capital, even if their ROI is less than the current divisional average.

- Reduces investment myopia and better aligns divisional and group interests.

Worked Example 1.3

Reconsider the project in Worked Example 1.1: Capital employed increases by $100,000, additional profit $15,000, required return 10%. What is the RI of the project?

Answer:

Notional charge = $100,000 × 10% = $10,000; RI = $15,000 − $10,000 = $5,000 (positive RI). The project should be accepted, as it increases total value.

Limitations of RI

- Absolute measure; can be less useful for comparison between divisions of different sizes.

- Still subject to manipulation through accounting policies and asset valuations.

- Does not eliminate all short-termism if non-financial objectives are ignored.

Economic Value Added (EVA): Towards True Value Creation

EVA refines RI by making further adjustments to profit and capital, aiming to reflect the real economic impact of decisions on shareholder value.

EVA derivation is presented as sequential adjustments to profit and capital, followed by WACC application and value-creation interpretation.

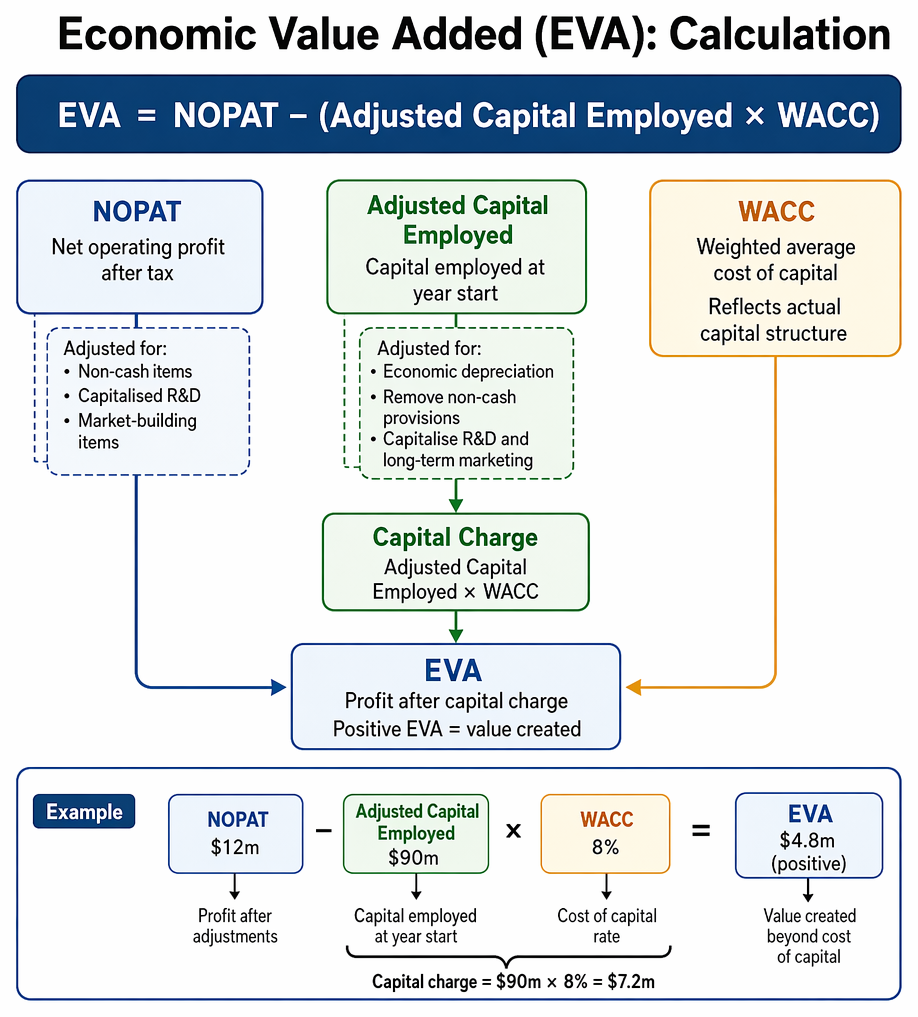

Key Term: Economic Value Added (EVA)

EVA measures profit after adjusting for economic reality and subtracting a charge for the cost of capital employed. It is strongly linked to long-term value creation.

Calculating EVA

EVA = NOPAT – (Adjusted Capital Employed × WACC)

- NOPAT: Net operating profit after tax, adjusted for non-cash and market-building items (e.g. capitalised R&D, economic depreciation)

- WACC: Weighted average cost of capital, reflecting the firm’s actual capital structure

Adjustments to capital and profit are required for items such as:

- Depreciation replaced by economic depreciation

- Non-cash provisions removed

- Expenditure on R&D and long-term marketing capitalised

Advantages of EVA

- Closely tracks changes in shareholder wealth

- Adjusts for differences in accounting policies

- Encourages managers to accept all positive-NPV investments, supporting long-term success

Worked Example 1.4

A division reports NOPAT (after necessary adjustments) of $12 million. Adjusted capital employed at year start is $90 million. WACC is 8%. Calculate EVA.

Answer:

Capital charge = $90m × 8% = $7.2m; EVA = $12m – $7.2m = $4.8m (positive). The division has created value beyond the cost of capital.

Drawbacks of EVA

- Complex; requires many non-standard adjustments

- Can be difficult to explain to non-finance managers

- May not be updated as frequently as simpler measures

Short Termism, Investment Myopia, and Performance Incentives

Short-termism is encouraged when performance systems use only short-term measures. This can result in underinvestment, asset hoarding, and lack of innovation. Investment myopia describes managers’ reluctance to commit resources to projects with longer-term payoffs.

Strategies to Reduce Short-Termism

- Use RI or EVA as performance measures, not just ROI or budget profit

- Set bonus schemes with multi-year horizons, not just annual targets

- Introduce non-financial indicators relating to innovation, customer satisfaction, or sustainability

- Combine financial measures with value-based management to achieve long-term alignment

Exam Warning: ACCA questions may require you to identify dysfunctional behaviour (e.g., rejection of value-adding projects or cost-cutting that harms future performance) caused by ROI-based rewards. Always discuss how using RI or EVA could improve alignment with corporate objectives.

Revision Tip: Always calculate both ROI and RI when a scenario includes a new investment opportunity. Check if a project with lower ROI than current divisional average still produces a positive RI or EVA.

Summary

ROI, RI, and EVA are key financial measures in divisional performance appraisal. ROI is simple but can encourage harmful short-termism and investment myopia. RI overcomes some misalignment by recognising excess returns above the required rate. EVA goes further, adjusting for economic reality and supporting shareholder value. To avoid short-term thinking, combine these financial measures with appropriately structured incentives and strategic, non-financial targets.

Key Point Checklist

This article has covered the following key knowledge points:

- Calculate and interpret ROI, RI, and EVA for divisional performance

- Describe how ROI can create dysfunctional short-termist behaviour and investment myopia

- Explain how RI and EVA can improve goal congruence

- State the strengths and weaknesses of ROI, RI, and EVA in appraisal and motivation

- Identify strategies to mitigate short-termism, including value-based management approaches

- Apply these techniques to ACCA APM exam scenarios

Key Terms and Concepts

- Return on Investment (ROI)

- Investment myopia

- Residual Income (RI)

- Economic Value Added (EVA)