Learning Outcomes

After studying this article, you will be able to explain how the petty cash imprest system works, including setting up the float, authorising and documenting payments, and managing regular reimbursements. You will also identify key controls, complete petty cash records, and reconcile the float as required by ACCA FA1 assessment.

ACCA Recording Financial Transactions (FA1) Syllabus

For ACCA Recording Financial Transactions (FA1), you are required to understand how petty cash is managed and recorded within a business, focusing on control, authorisation, and reconciliation. Specifically, you should be able to:

- Explain the purpose and operation of the petty cash imprest system

- Set up and replenish a petty cash float

- Process, document, and authorise petty cash payments and reimbursements

- Enter and analyse petty cash transactions, including those with sales tax

- Carry out petty cash reconciliations

- Distinguish between imprest and non-imprest petty cash systems

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main principle behind the petty cash imprest system?

- Which documents are required to support and authorise a petty cash claim?

- If the imprest amount is $150 and petty cash vouchers total $42.70 at top-up, how much should be withdrawn from the bank?

- True or false? The total of the petty cash float and all petty cash vouchers should always equal the agreed imprest amount.

- Who should be responsible for authorising petty cash payments above the normal limit?

Introduction

Businesses often need to pay small expenses such as postage, office refreshments, or minor travel costs. Using the main bank account for these is impractical. To manage these efficiently, many organisations maintain a petty cash system—commonly using the imprest method. Proper control and documentation of petty cash are essential for preventing misuse and ensuring accurate financial records. This article shows how an imprest system operates, how to set and replenish the float, and the checks required for authorising and recording reimbursements.

Key Term: petty cash

Notes and coins kept by a business to pay for small, infrequent expenses.Test Tip: When revising Establishing float and reimbursements, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Petty Cash Imprest System

Overview

The imprest system gives a petty cashier a fixed sum—the float—to use for authorised small payments. At regular intervals, the float is replenished, bringing cash on hand back to the starting amount. This approach helps maintain tight control and accountability, as all expenses must be supported by proper documents.

Key Term: imprest system

A system where the petty cash float is kept at a fixed amount by regularly reimbursing only what has been spent.

Setting Up the Float

The initial float is set at a level that meets expected minor expenses, often covering two to four weeks. The amount is withdrawn from the bank and securely placed with a responsible petty cashier.

Authorising and Documenting Payments

Employees who pay for small business expenses with their own cash can reclaim the amount from petty cash. Each claim must be recorded using a petty cash voucher, supported by receipts or other valid evidence, and authorised according to company policy. Typically, the petty cashier may authorise claims up to a certain limit, but larger claims require higher approval.

Key Term: petty cash voucher

A signed document used to claim reimbursement from petty cash, detailing the expense and attaching the original receipt.

Recording Transactions

Each payment out of petty cash is entered sequentially in the petty cash log or book. The log tracks the date, voucher number, amount, type of expense, and any sales tax included. Maintaining accurate records simplifies later reconciliation and ensures expenses are posted to the proper accounts in the general ledger.

Replenishing and Reconciling the Float

At the end of each period (usually monthly or when funds run low), the petty cashier prepares a reimbursement claim. The sum of all petty cash vouchers since the last top-up is calculated, and exactly this amount is withdrawn from the bank to restore the float to its original level. Thus, at any time: Imprest amount = cash in petty cash box + total value of unpaid vouchers

A reconciliation must be performed by adding the remaining cash and all vouchers; this total should always equal the authorised float. Any difference should be investigated immediately.

Worked Example 1.1

Question: A business operates a petty cash imprest system with a float of $120. Over the week, five petty cash vouchers were issued, totalling $45.20. At the end of the week, how much money should be withdrawn from the bank to restore the float, and what should be the total of the float after top-up?

Answer:

The replenishment required is $45.20, restoring cash on hand to $120. After top-up, the petty cash box will again hold $120 in total (notes, coins, and new vouchers).

Security and Controls

The petty cash float should be kept securely—preferably in a locked box or safe. Access is limited to trained and trusted individuals. All vouchers must be numbered and checked for completeness and authorisation. Unauthorised, undocumented, or excessive claims should be refused.

Key Term: float

The total authorised amount of notes and coins held in petty cash at any point.

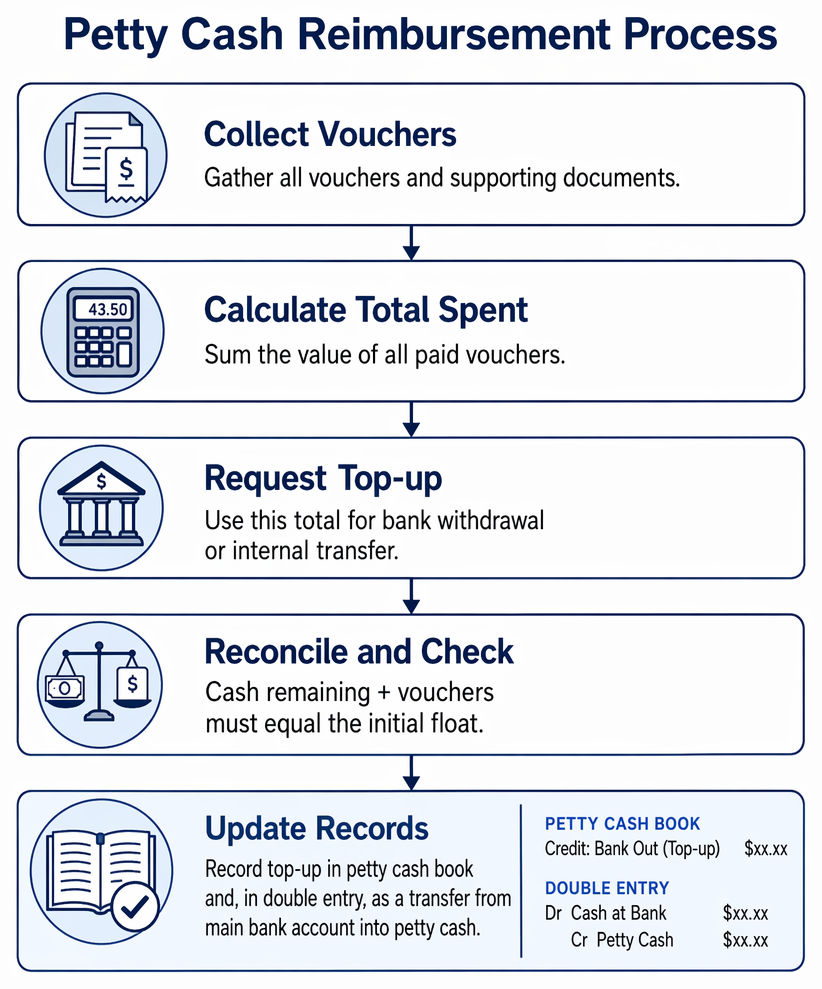

Petty Cash Reimbursement Process

Petty cash claims are validated against receipts, policy, and cashier limits before reimbursement, rejection, or escalation for managerial authorisation.

- Collect Vouchers: The petty cashier gathers all vouchers and supporting documents for the period.

- Calculate Total Spent: The value of all paid vouchers is summed.

- Request Top-up: This total is used for the bank withdrawal or internal transfer.

- Reconcile and Check: Cash remaining plus vouchers must equal the initial float.

- Update Records: Top-up is recorded in the petty cash book and, in double entry, as a transfer from the main bank account into petty cash.

Worked Example 1.2

Question: A petty cashier begins with a $75 float. During the month, the following petty cash vouchers are issued: $9.80 (stamps), $4.30 (refreshments), $17.40 (taxi fares), and $12.00 (stationery, including $2.00 sales tax). At month-end, what is the required top-up? How should this be recorded?

Answer:

Total vouchers: $9.80 + $4.30 + $17.40 + $12.00 = $43.50. Top-up required is $43.50 to restore float to $75. The petty cash book is credited for $43.50 (bank out), and cash at bank is debited for the same amount.Exam Warning: Many students forget that only the amount actually spent (not a fixed periodic sum) is reimbursed under the imprest system. Any discrepancy between cash and vouchers must be treated as an error or possible theft.

Differences: Imprest vs. Non-Imprest Systems

Most businesses use the imprest system for the extra control it provides. A non-imprest system might simply replenish petty cash with a fixed amount at intervals, regardless of actual spend. This risks growing imbalances, weak control, and unrecorded losses.

Summary

The petty cash imprest system means establishing a fixed float, paying out only on proper authorisation and documentation, and regularly reimbursing just the amount spent. All expenditure is recorded using vouchers and supporting evidence, and the float is always maintained through strict reconciliation. This method ensures security, accountability, and reliable records for small cash payments.

Key Point Checklist

This article has covered the following key knowledge points:

- Operation and purpose of the petty cash imprest system

- Setting up and securing the petty cash float

- Authorising and documenting petty cash payments

- Replenishing the float through accurate reimbursement

- Reconciling petty cash (cash plus vouchers equals float)

- Importance of control procedures to prevent loss or misuse

Key Terms and Concepts

- petty cash

- imprest system

- petty cash voucher

- float