Learning Outcomes

After studying this article, you will be able to explain how the petty cash imprest system operates, describe how the imprest float is established and maintained, record petty cash transactions with vouchers, and process period-end replenishment in line with ACCA FA2 requirements. You will understand the double-entry bookkeeping entries needed and recognize key features that support internal control over small cash payments.

ACCA Maintaining Financial Records (FA2) Syllabus

For ACCA Maintaining Financial Records (FA2), you are required to understand how businesses control and record small cash payments using the petty cash imprest system. Focus your revision on:

- Recording cash and petty cash transactions in the general ledger

- Explaining the purpose and operation of the petty cash imprest system

- Setting up, maintaining, and replenishing the petty cash float

- Using vouchers to document petty cash payments and support internal control

- Posting petty cash records to expense accounts and the bank account

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the main purpose of the petty cash imprest system?

- a) To avoid using cash

- b) To provide a fixed amount of cash for minor expenses

- c) To record all purchases on credit

- d) To replace regular bank reconciliations

-

At the end of a period, a petty cash float of $100 has $21 in coins and $79 in petty cash vouchers for expenses. How much cash should be withdrawn from the bank to restore the float?

-

Name two benefits of using numbered petty cash vouchers for recording expenses.

-

Which is the correct double-entry to record petty cash replenishment from the main bank account?

- a) Debit petty cash, Credit bank

- b) Debit expenses, Credit petty cash

- c) Debit bank, Credit petty cash

- d) Debit vouchers, Credit expenses

Introduction

Small, routine expenses—such as office refreshments, cleaning supplies, or taxi fares—are often paid with cash rather than through the main bank account. To manage and record these outlays properly, many businesses use a petty cash imprest system. This system issues a fixed sum of cash (the imprest) which is topped up at regular intervals to the original float amount. Supporting each payment, a petty cash voucher is completed, providing evidence of the transaction.

The imprest system ensures tight control over physical cash and prevents misuse or loss of funds. Used correctly, petty cash procedures help maintain accurate accounting records, support regular reconciliations, and reduce the risk of errors or fraud.

Key Term: imprest system

A method for managing petty cash where a fixed float is issued, and at all times the sum of cash on hand and vouchers equals the original float. Key Term: petty cash voucher

A pre-numbered document completed for each petty cash payment, detailing the date, amount, purpose, and authorisation.

The Petty Cash Imprest System Explained

The imprest system operates by holding a fixed amount of cash—called the imprest or float—in a locked box. The petty cashier issues cash to employees for minor, approved expenses and collects a completed, authorised voucher with each payment and (where possible) the supporting receipt.

Petty cash control procedures show verification against the imprest amount, reimbursement processing, float reinstatement, and immediate investigation of discrepancies.

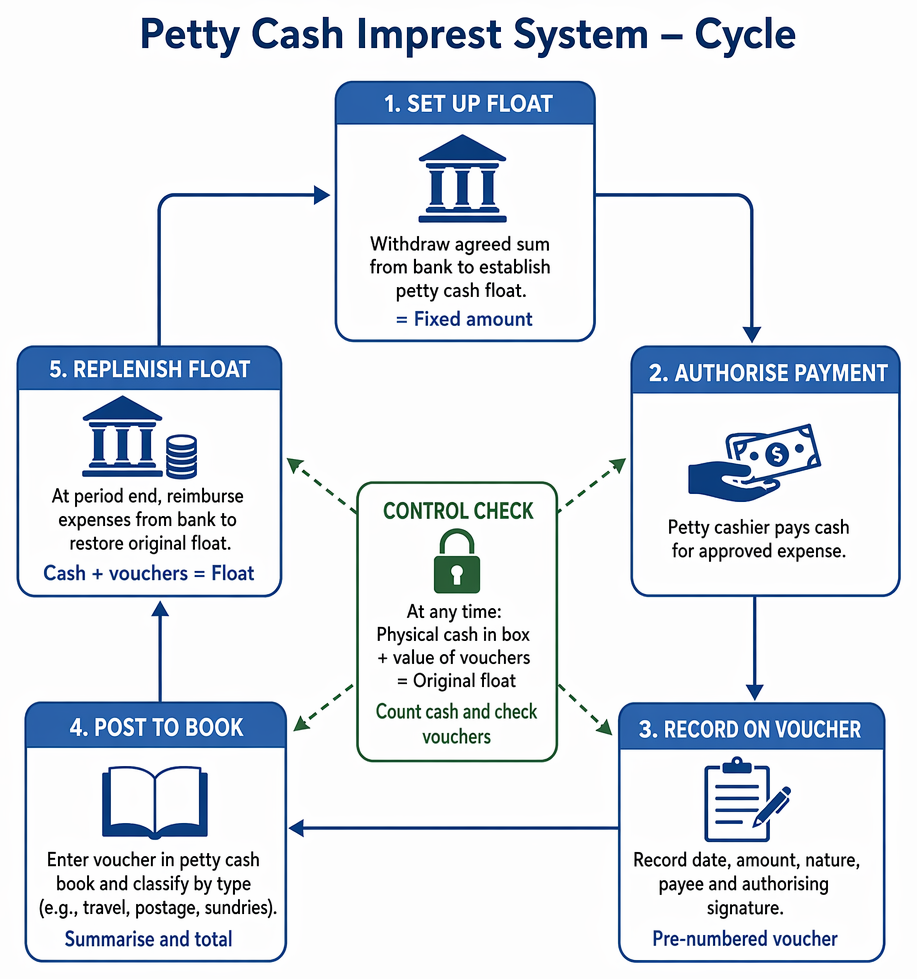

Setting Up the Imprest Float

A petty cash float is established by withdrawing an agreed sum from the main bank account. This amount should cover expected small payments for a set period (often a week or month).

Example: The business decides on an imprest float of $80. The petty cash account is set up by transferring $80 cash from the bank.

Key Term: petty cash float

The fixed amount of cash maintained in the petty cash box at the start of each period.

Authorising and Recording Payments

Each time cash is paid out, details are recorded on a petty cash voucher. The voucher specifies the date, amount, nature of the expense, the person receiving the cash, and the authorising signature. Vouchers are pre-numbered for control. Where possible, staff provide supporting receipts.

These transactions are entered into the petty cash book, classified under appropriate columns (e.g., travel, postage, sundries). This ensures expenses are summarised by type and totalled for posting to the ledger.

Maintaining Effective Control

At any time, the total of physical cash in the box plus the value of vouchers should equal the original float. Management or an independent person can count the cash and check the vouchers to verify the balance remains correct. Missing cash or unapproved vouchers are indicators of errors or potential misuse.

Replenishing the Imprest

At the end of the period, the petty cash balance is restored to its original float by making up the difference between cash remaining and the initial amount. For example, with a float of $100, if $76 worth of vouchers and supporting receipts have been collected, there should be $24 in coins and notes remaining.

The petty cash cashier prepares a reimbursement request summarising the expenses incurred. The main bank account is used to withdraw $76, which is added to the cash in the box, restoring the float to $100. The replenishment is recorded as a payment from the bank and an equivalent increase in petty cash.

Key Term: replenishment

The process of restoring the petty cash float to its original amount at set intervals by transferring cash from the bank.

Accounting Entries for Petty Cash Transactions

Each petty cash payment is initially classified under the relevant expense type (e.g., travel, stationery) in the petty cash record. These totals are posted periodically to the main ledger.

The replenishment is recorded as follows:

- Debit: Individual expense accounts (totaled from petty cash vouchers for the period)

- Credit: Bank account (for the reimbursement amount)

This ensures both the reduction in the bank balance and the increase in recorded business expenses are reflected.

Key Term: petty cash book

An analysed record summarising petty cash payments by type, supporting the periodic posting to ledger accounts.

Petty Cash Vouchers and Documentation

Petty cash vouchers are central to the imprest system's control. To be valid, a voucher must:

- Be sequentially numbered

- Show the date, recipient, amount, description, and authorisation

- Attach supporting receipts wherever possible

All vouchers should be reviewed before replenishment to confirm they represent legitimate expenses and are appropriately approved.

Worked Example 1.1

A business maintains a petty cash imprest of $50. After two weeks, it has $12.80 in cash remaining, with numbered vouchers totaling $37.20 for approved expenses.

Question: How much should the cashier request from the bank to restore the imprest? Which ledger entries are needed?

Answer:

The cashier should request $37.20 from the bank ($50 float - $12.80 cash = $37.20 spent). The entry is: Debit relevant expense accounts (e.g., Sundries $10, Stationery $15, Postage $12.20) Credit Bank $37.20

Worked Example 1.2

During a monthly review, management finds the petty cash box contains $22 in cash and vouchers for $78, but the imprest should be $100. What does this indicate, and what step should be taken?

Answer:

The cash plus vouchers add to the imprest of $100, so the amount is correct. No cash is missing. If the numbers did not match, the discrepancy would require immediate investigation.Exam Warning: In your exam, questions may ask for the exact double-entry to record petty cash replenishment. Always credit the bank and debit the expense accounts with the total value of petty cash vouchers.

Revision Tip: Regular audits of petty cash help detect errors or misuse promptly. Always check that all vouchers are signed, numbered, and matched with receipts.

Summary

The petty cash imprest system is a structured method for controlling minor cash payments. By holding a fixed float, collecting vouchers for every payment, and regularly restoring the imprest from the bank, businesses ensure all small outlays are authorised, accurately recorded, and properly classified in the accounts. Strong documentation and periodic checks maintain accountability and reduce the chance of errors or fraud.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the purpose and operation of the petty cash imprest system

- Set up and maintain a petty cash float, restoring it as needed

- Record petty cash payments using numbered vouchers and collect receipts

- Account for petty cash replenishments in the general ledger

- Recognise the role of documentation and regular checking for internal control

Key Terms and Concepts

- imprest system

- petty cash voucher

- petty cash float

- replenishment

- petty cash book