Learning Outcomes

After studying this article, you will be able to record and explain the disposal and part-exchange of property, plant, and equipment (PPE), calculate gains or losses on disposal, and understand the impact of these transactions on both the ledger accounts and the financial statements for ACCA Maintaining Financial Records (FA2).

ACCA Maintaining Financial Records (FA2) Syllabus

For ACCA Maintaining Financial Records (FA2), you are required to understand how to record, account for, and present disposals and part-exchanges of property, plant, and equipment. Focus your revision on:

- Recording the disposal and part-exchange of tangible non-current assets in line with IAS 16 Property, Plant and Equipment

- Preparing journal and ledger entries for asset disposals, including transfers of cost and accumulated depreciation

- Calculating and recording gains or losses on disposal and reflecting these in the statement of profit or loss

- Recognising the accounting treatment of part-exchange transactions when acquiring new assets

- Presenting the impact of disposals and part-exchanges in financial statements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which account is credited with the original cost of an asset when it is disposed of?

-

A delivery van was bought for $10,000. Accumulated depreciation totals $7,000 at disposal. If the van is sold for $4,000, what is the gain or loss on disposal?

-

True or false? When an old asset is given in part-exchange for a new one, the part-exchange value represents the proceeds from the disposal of the old asset.

-

Briefly outline the double-entry required to record a gain on disposal of PPE.

Introduction

Tangible non-current assets, such as property, plant, and equipment, are used over several periods but are often disposed of before the end of their useful lives. Disposals can be through sale, scrapping, or part-exchange for new assets. You must accurately record the removal of the asset’s cost and accumulated depreciation, recognise any cash proceeds or part-exchange value, and calculate the resulting gain or loss for financial reporting and assessment purposes.

Key Term: disposal account

A temporary ledger account used to collect all entries related to the disposal of a non-current asset, including the asset’s cost, accumulated depreciation, and proceeds.Test Tip: When revising Disposals, part-exchanges, and gains/losses, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Accounting for Disposals of Property, Plant, and Equipment

Property, plant and equipment disposal calculations compare disposal proceeds, including part-exchange allowances, with carrying amount to determine gain or loss.

The Disposal Process

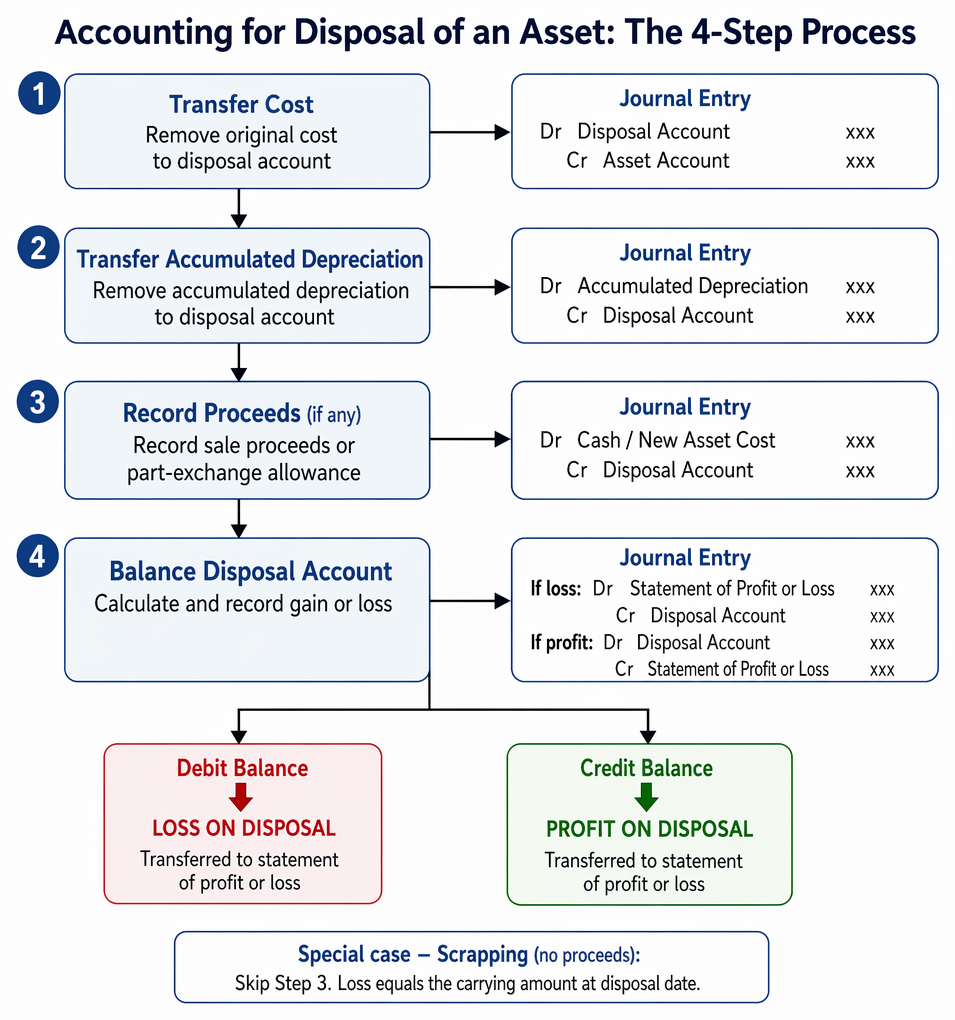

Disposing of a non-current asset involves removing its cost and accumulated depreciation from the records and bringing together the relevant amounts in the disposal account to calculate any gain or loss. The steps are as follows:

- Transfer the cost of the asset to the disposal account (credit the asset account, debit the disposal account).

- Transfer accumulated depreciation to the disposal account (debit accumulated depreciation, credit the disposal account).

- Record sale proceeds or part-exchange allowance (debit cash or new asset cost account, credit the disposal account).

- Calculate and record the gain or loss by balancing the disposal account:

- Debit balance = Loss (transferred to the statement of profit or loss)

- Credit balance = Profit (transferred to the statement of profit or loss)

Key Term: accumulated depreciation

The total amount of depreciation charged on an asset since its purchase up to the date of disposal. Key Term: gain on disposal

The amount by which the net disposal proceeds exceed the carrying amount of the asset at disposal date. Key Term: loss on disposal

The amount by which the carrying amount of the asset exceeds the disposal proceeds.

Worked Example 1.1

A business sells a piece of equipment originally purchased for $12,000. At the date of disposal, accumulated depreciation is $8,000. The equipment is sold for $3,500 cash. What is the gain or loss on disposal, and how should the entries be recorded?

Answer:

- Transfer cost: Debit disposal account $12,000, credit equipment account $12,000.

- Transfer accumulated depreciation: Debit accumulated depreciation $8,000, credit disposal account $8,000.

- Record proceeds: Debit cash $3,500, credit disposal account $3,500.

- Disposal account balance: $12,000 (debit) less $8,000 + $3,500 (credit) = $500 loss.

- Entry for loss: Debit statement of profit or loss (loss on disposal) $500, credit disposal account $500.

- The loss is reported as an expense in the statement of profit or loss.

Cash Sale vs. Scrapping

If the asset is scrapped (no proceeds received), the loss equals the carrying amount at disposal date. The accounting process remains the same except that there are no proceeds to credit to the disposal account.

Part-Exchange of Non-Current Assets

Part-exchange (or trade-in) is common when replacing assets, such as vehicles. The old asset is exchanged for an agreed allowance against the cost of a new asset.

- The part-exchange allowance acts as the "sale proceeds" of the old asset.

- The cost of the new asset equals its full list price; the part-exchange allowance is credited against this, with the balance payable in cash or by other method.

Entries:

- Record the disposal of the old asset in the usual way, using the part-exchange value as the proceeds.

- Recognise the new asset at full cost:

- Debit new asset account with full cost.

- Credit disposal account with part-exchange allowance and credit cash/bank with any balance paid.

Worked Example 1.2

A company buys a new van for $15,000. The dealer accepts the old van as part-exchange, giving a $4,000 allowance. The old van originally cost $10,000 with accumulated depreciation of $8,000 at the disposal date. The company pays the $11,000 difference in cash.

Answer:

- Transfer old van cost: Debit disposal account $10,000, credit vans account $10,000.

- Transfer old van accumulated depreciation: Debit accumulated depreciation $8,000, credit disposal account $8,000.

- Record part-exchange: Debit new van account $4,000, credit disposal account $4,000.

- Cash paid for new van: Debit new van account $11,000, credit cash $11,000.

- Total new van cost: $4,000 (part-exchange) + $11,000 (cash) = $15,000.

- Disposal account calculation: $10,000 (debit) less $8,000 + $4,000 (credit) = $2,000 credit (profit), credited to statement of profit or loss as gain on disposal.

Exam Warning: Be careful: Only the part-exchange allowance is treated as proceeds from the old asset’s disposal. Always record the new asset at its full cost, not just the cash paid.

Presentation in the Financial Statements

Gains or losses on disposal appear in the statement of profit or loss as other income or expense. After disposal, the asset and its accumulated depreciation are both removed from the statement of financial position. The new asset is presented at cost, with depreciation commencing as usual.

Summary

Disposals and part-exchanges require clearing the cost and accumulated depreciation from the records, correctly recording any proceeds, and identifying the gain or loss on disposal for the financial statements. In part-exchange transactions, the old asset is treated as disposed of at the agreed allowance, with the new asset recorded at full list price. Careful preparation of the disposal account is critical to accurate reporting.

Key Point Checklist

This article has covered the following key knowledge points:

- Record disposals and part-exchanges of property, plant, and equipment using the disposal account

- Transfer asset cost and accumulated depreciation to the disposal account on disposal

- Calculate and record gain or loss on disposal in the financial statements

- Account for part-exchange by treating the allowance as disposal proceeds and new asset at full list price

- Present the disposal's effect in both the ledger accounts and financial statements

Key Terms and Concepts

- disposal account

- accumulated depreciation

- gain on disposal

- loss on disposal