Learning Outcomes

After completing this article, you will be able to describe and apply techniques used by auditors to understand, document, and evaluate accounting systems. You will learn how to use narrative notes, flowcharts, and control questionnaires, as well as how to evaluate controls and identify deficiencies. By the end, you will be able to state the steps needed to highlight and report significant weaknesses within a system—skills essential for the ACCA Foundations in Audit (FAU) exam.

ACCA Foundations in Audit (FAU) Syllabus

For ACCA Foundations in Audit (FAU), you are required to understand the approaches auditors use to examine and assess the adequacy of an entity’s accounting systems. This article focuses on:

- The use of narrative notes and flowcharts to document systems

- Internal control questionnaires (ICQs) and internal control evaluation questionnaires (ICEQs)

- Evaluating the effectiveness of internal controls

- Identifying and defining deficiencies in controls

- Communicating significant control deficiencies to management

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which method would best illustrate the sequence and checks in a complex transaction cycle?

- a) Narrative notes

- b) Organisation charts

- c) Flowcharts

- d) Internal audit reports

-

What is the main purpose of an Internal Control Evaluation Questionnaire (ICEQ)?

- a) To narrate all system steps in detail

- b) To identify the absence of key controls in a system

- c) To document payroll figures

- d) To test inventory valuation

-

State two reasons why standardised ICQs might become ineffective for identifying system deficiencies.

-

Briefly explain what should be communicated to management when a significant control deficiency is identified.

Introduction

Accurate and reliable accounting systems are essential for trustworthy financial reporting and effective internal control. Auditors must not only understand how these systems operate but also assess their strengths and weaknesses. Evaluating systems involves documenting processes and controls, then identifying any gaps that may lead to error or fraud. If deficiencies are discovered, auditors have a responsibility to communicate them clearly to management.

Test Tip: When revising Evaluating system and identifying deficiencies, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Understanding and Recording Accounting Systems

To evaluate any accounting system, auditors first need to understand and record how it operates in practice. Several techniques are available for this purpose, each with their unique strengths.

Narrative Notes

Narrative notes describe the system’s procedures and controls in plain language. They are useful for simple systems or small entities where the number of transactions is low and processes are straightforward. However, for more complex systems, narrative notes can become lengthy and make it harder to spot gaps or inefficiencies.

Key Term: Narrative Notes

Narrative notes are written descriptions detailing the procedures and controls of an accounting system, suitable for simple, low-volume processes.

Flowcharts

Flowcharts offer a diagrammatic representation, showing the flow of documents, operations, and checks within the system. They help auditors visualize how transactions and controls move through different departments, making it easier to pinpoint missing steps or weaknesses.

Key Term: Flowchart

A flowchart is a visual diagram illustrating the movement and checks of transactions and documents through an accounting system.

Flowcharts are especially useful in larger organizations where transaction cycles involve many steps and multiple staff. They standardize system depiction and make reviewing or updating system documentation more efficient.

Organisation Charts

Organisation charts show the structure of an entity, indicating lines of reporting and responsibility. While helpful for understanding staff roles, they do not specify process details or controls within transaction cycles.

Evaluating Accounting Systems

Once the system is fully documented, auditors must evaluate whether internal controls are robust enough to prevent or detect material misstatements. This is achieved by structured evaluation tools.

Internal Control Questionnaires (ICQs)

An Internal Control Questionnaire is a standardized list of questions about the existence of controls in a particular system (for example, purchasing or payroll). Auditors complete the ICQ by asking client personnel yes/no questions targeted at key control objectives.

Key Term: Internal Control Questionnaire (ICQ)

A document comprising a formal list of questions to determine whether expected internal controls are present within a specific transaction cycle.

ICQs help auditors ensure that all important controls have been considered, and deficient answers (usually ‘No’) indicate where further testing or attention is required.

Internal Control Evaluation Questionnaires (ICEQs)

Whereas ICQs focus on the presence of controls, ICEQs aim to uncover specific weaknesses by asking questions about potential errors or omissions in the system.

Key Term: Internal Control Evaluation Questionnaire (ICEQ)

An evaluation tool with direct questions designed to detect the absence or ineffectiveness of key controls, highlighting possible errors or fraud.

ICEQs are shorter than ICQs and require auditor judgement—they work best when combined with system documentation such as flowcharts.

Checklists

Checklists, much like ICQs, provide a standardized way to ensure all areas of the system have been reviewed, especially in high-volume or standardized transaction cycles.

Identifying System Deficiencies

Evaluating an accounting system often reveals deficiencies—weaknesses that increase the risk of error or fraud. Recognizing and reporting these is a key auditor responsibility.

Key Term: Deficiency

A deficiency is a weakness in the design or operation of a control that could allow errors or fraud to go undetected or uncorrected.

Common examples include lack of segregation of duties, missing authorizations, or absence of regular reconciliations.

When deficiencies are found, auditors assess the severity. Significant deficiencies—those likely to lead to material misstatements—must be formally communicated to management or those charged with governance.

Worked Example 1.1

Question: You are evaluating the purchases system at Pioneer Ltd and complete an ICQ. Several questions related to segregation of duties, invoice approvals, and supplier statement reconciliations are answered ‘No’. What do you do with these findings?

Answer:

- Highlight the areas where controls are absent or ineffective.

- Translate the failed controls into identified deficiencies, explaining how each could lead to errors or fraud (e.g., lack of supplier statement reconciliation could mean missing payables or undetected duplicate payments).

- Determine whether any are significant and must be reported promptly to management, supported by recommendations to improve controls.

Communication of Deficiencies

Auditors must communicate significant deficiencies to management, explaining their nature, possible effects, and suggesting corrective actions.

Exam Warning: A common exam pitfall is failing to link an identified system weakness to its potential consequences. Always state why a deficiency matters—for example, how the absence of authorisation controls could result in unauthorised or fraudulent transactions.

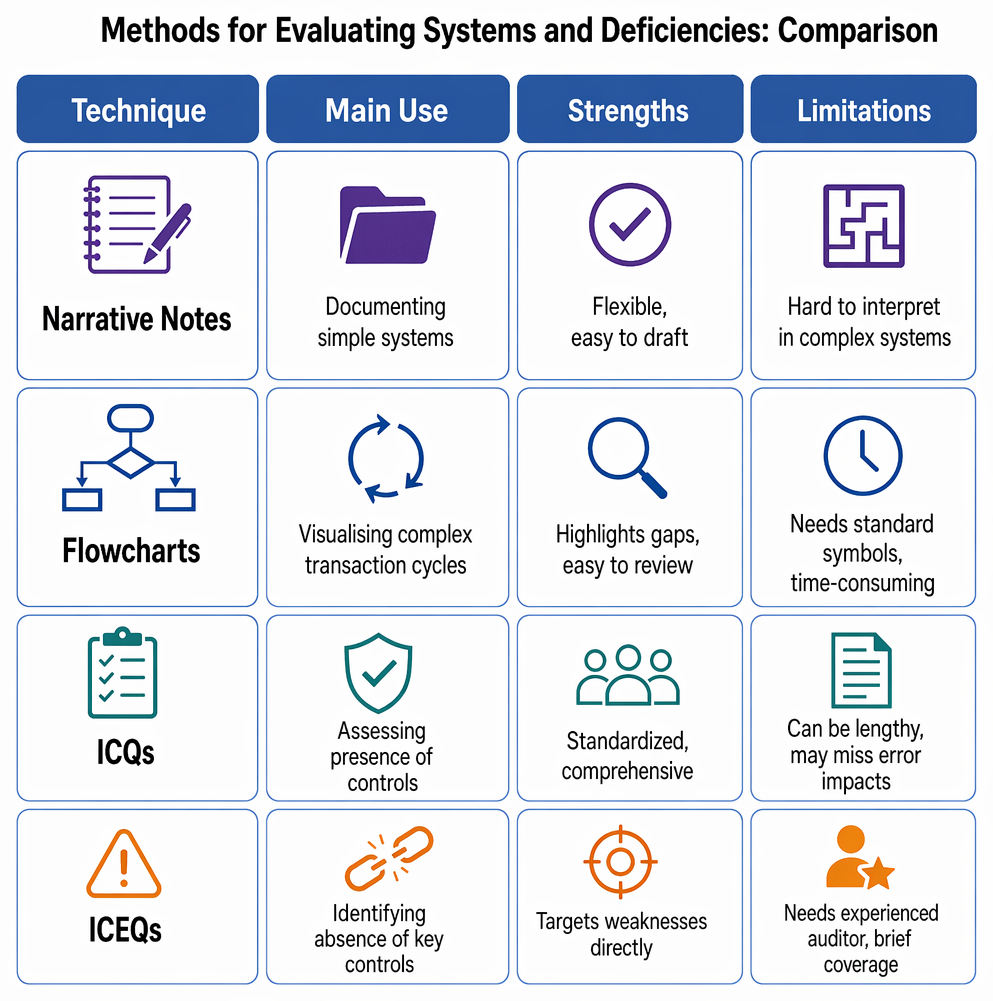

Methods for Evaluating Systems and Deficiencies: Comparison

Accounting system documentation is matched to purpose: narrative notes for simple systems, flowcharts for complex processes, and organisation charts for reporting lines.

| Technique | Main Use | Strengths | Limitations |

|---|---|---|---|

| Narrative Notes | Documenting simple systems | Flexible, easy to draft | Hard to interpret in complex systems |

| Flowcharts | Visualising complex transaction cycles | Highlights gaps, easy to review | Needs standard symbols, time-consuming |

| ICQs | Assessing presence of controls | Standardized, comprehensive | Can be lengthy, may miss error impacts |

| ICEQs | Identifying absence of key controls | Targets weaknesses directly | Needs experienced auditor, brief coverage |

Key Point Checklist

This article has covered the following key knowledge points:

- Techniques to document and understand accounting systems: narrative notes, flowcharts, organisation charts

- Use and formatting of Internal Control Questionnaires (ICQs) and Internal Control Evaluation Questionnaires (ICEQs)

- How to evaluate systems and identify deficiencies using structured tools and checklists

- Reporting significant system deficiencies to management and suggesting improvements

- The need to relate deficiencies to risks of error or fraud in exam and practice scenarios

Key Terms and Concepts

- Narrative Notes

- Flowchart

- Internal Control Questionnaire (ICQ)

- Internal Control Evaluation Questionnaire (ICEQ)

- Deficiency