Learning Outcomes

After reading this article, you will be able to explain the purpose of credit policies, perform basic creditworthiness assessments, and discuss credit scoring methods relevant to the ACCA Foundations in Financial Management exam. You will understand the factors used to evaluate customers before granting credit and the importance of scoring systems for managing credit risk.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand how to identify, assess, and control risks associated with offering credit to customers. Focus your studies on:

- The objectives and components of an effective credit policy

- Methods and factors used to assess customer creditworthiness

- The use and interpretation of credit scoring techniques

- The role of credit limits and controls in minimizing bad debts and sustaining liquidity

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is a common quantitative factor assessed in creditworthiness evaluation?

- a) Customer’s industry reputation

- b) Current ratio

- c) Employee satisfaction

- d) Marketing strategy

-

What does a credit score help a business decide?

- a) The maximum amount of inventory to purchase

- b) The selling price of its products

- c) The amount of credit to extend to a customer

- d) The annual rate of depreciation

-

True or false? A customer’s creditworthiness assessment should consider both historical payment behavior and projected future trading.

-

Briefly explain why setting credit limits is important for a business.

Introduction

Many businesses choose to sell goods or services on credit, allowing customers to pay after receipt. This supports higher sales but increases the risk of non-payment. To manage this risk, robust credit policies and systematic assessment of customer creditworthiness are essential. Credit scoring models further enable organizations to quantify credit risk and control exposure. These tools help minimize bad debts and protect cash flow.

Key Term: Credit policy

The set of rules and procedures a business uses to determine how much credit to extend to customers and under what terms.

CREDIT POLICY AND ITS OBJECTIVES

A credit policy sets clear guidelines on extending credit to customers. Its objectives are:

- To maximize sales revenue by making credit available to reliable customers

- To minimize the risk of late or non-payment (bad debts)

- To control the company’s exposure to financial losses from credit sales

- To balance sales growth with healthy cash flows

A well-structured credit policy should define the criteria for granting credit, acceptable risk levels, processes for reviewing credit applications, and the procedures for collection.

CREDITWORTHINESS ASSESSMENT

Assessing a potential or existing customer's creditworthiness is a key part of the credit policy. The aim is to determine the likelihood that the customer will pay on time and in full.

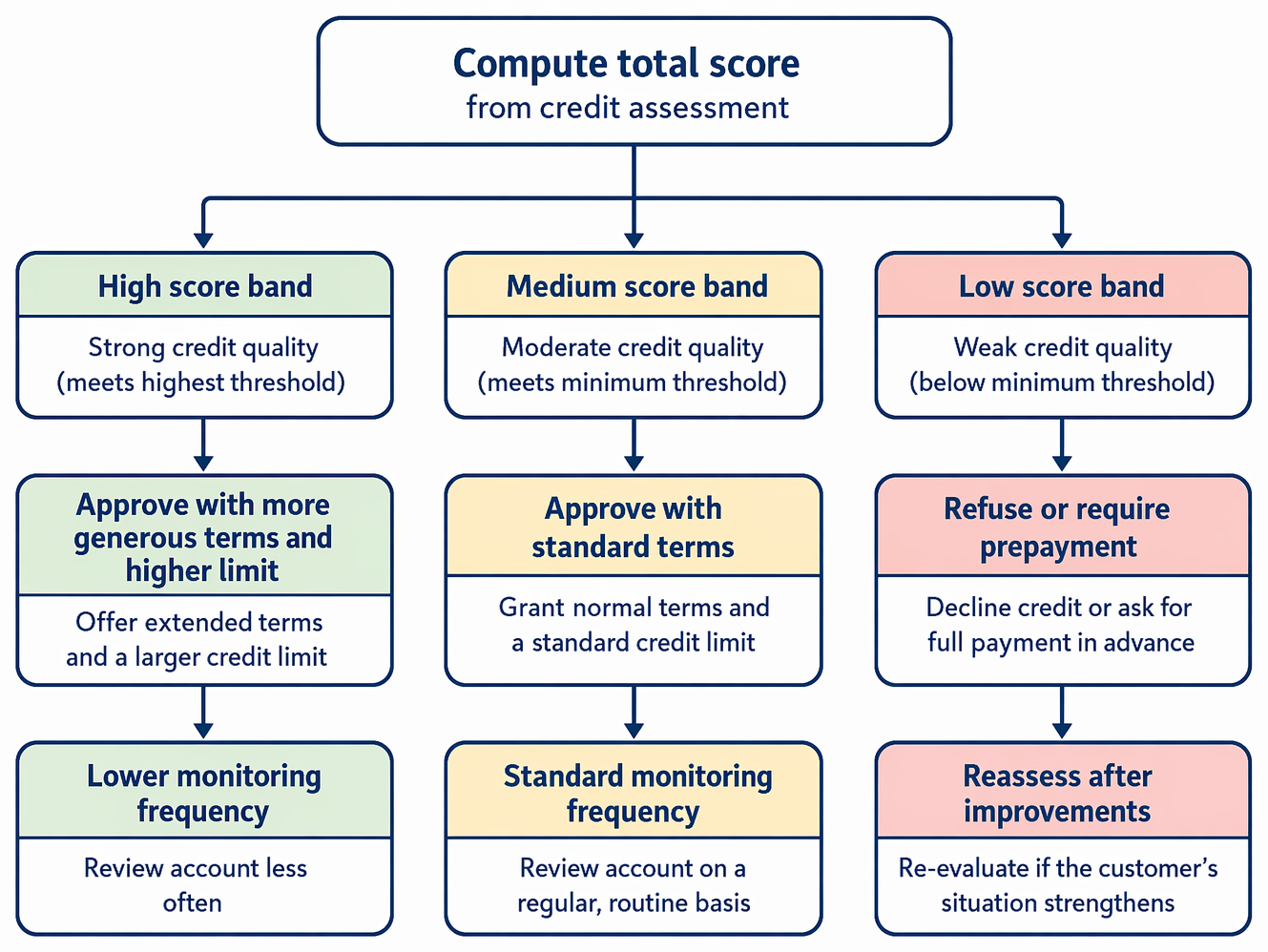

Customer risk bands derived from aggregate scores determine generous credit, standard terms, or refusal with subsequent review.

Key Steps in Credit Assessment

- Collect information about the customer (financial statements, payment history, credit references)

- Analyze qualitative and quantitative factors affecting their risk

- Allocate a credit rating or score

- Decide on appropriate credit terms and limits

Key Term: Creditworthiness

The assessment of a customer's ability and willingness to pay debts as they fall due.

Main Factors in Credit Assessment

Quantitative Factors

- Liquidity ratios (e.g., current ratio, quick ratio)

- Gearing (debt to equity ratio)

- History of payment and outstanding balances

- Level of existing credit with other suppliers

Qualitative Factors

- Length of time trading and business reputation

- Management experience and stability

- Industry and economic conditions

- Legal disputes or credit defaults

Where possible, these factors are considered together for a balanced view.

Worked Example 1.1

A business receives a credit application from Delta Co, which requests a $20,000 credit limit. Delta Co's financial statements show a current ratio of 2.1, a consistent record of on-time payments with other suppliers, but recent media reports signal possible cash flow pressures due to new project delays.

Question: Should Delta Co be granted the requested limit automatically?

Answer:

The business should not approve the full request without further checks. While the current ratio and payment history are positive, the reports of project delays may increase cash flow risk. It may be prudent to grant a lower initial credit limit and monitor payment performance.

CREDIT SCORING SYSTEMS

Credit scoring quantifies credit risk through weighted points assigned to various assessment factors. A total score helps businesses consistently and objectively evaluate applications.

Key Term: Credit scoring

A technique that assigns numerical values to factors affecting credit risk, producing a score used to guide lending decisions.

Scores are typically based on:

- Financial ratios (liquidity, profitability)

- Past payment record

- Length of relationship

- External credit ratings

- Outstanding debt levels

A company's credit policy will specify minimum scores for acceptance or different levels of credit terms.

Worked Example 1.2

A credit scoring model has the following weights:

- Payment history: 50 points

- Liquidity ratio: 30 points

- External credit agency rating: 20 points

Customer X scores 45 for payment history, 25 for liquidity, and 10 for agency rating, totaling 80 points. The minimum passing score is 75.

Question: Would Customer X be accepted or refused credit?

Answer:

Customer X achieves a score above the acceptance threshold, so credit may be granted, subject to final manager review. However, the relatively low agency rating suggests extra caution or closer monitoring.

SETTING CREDIT LIMITS AND ONGOING MONITORING

Once a credit assessment is complete and the score meets requirements, a credit limit is set. Credit limits reflect the maximum exposure deemed safe given the customer's risk rating.

Regular review is required, especially if a customer's circumstances change or late payments are observed. This helps control risk and limit business losses.

Exam Warning: Do not rely only on historical payment behavior. Exam questions often require you to consider qualitative and forward-looking information when assessing credit risk.

Revision Tip: Practice calculating basic credit scores and interpreting risk indicators. Focus on both the numeric assessment and the reasoning behind setting limits.

Summary

Careful evaluation of credit risk is essential for every business that sells on credit. Credit policies, systematic creditworthiness assessment, and credit scoring models help businesses extend credit safely, limit bad debts, and maintain strong liquidity.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify the main objectives and elements of a credit policy

- Explain how to perform a creditworthiness assessment and why it matters

- List common quantitative and qualitative risk factors in credit decisions

- Describe credit scoring systems and their application in granting credit

- Recognize the importance of setting credit limits and reviewing credit accounts

Key Terms and Concepts

- Credit policy

- Creditworthiness

- Credit scoring