Learning Outcomes

After studying this article, you will be able to explain the objectives of credit policies, identify how terms, limits, and discounts are set for customers, and assess the risks and benefits associated with offering credit. You will also be able to calculate the financial effects of various discount policies and recommend procedures for effective credit control in accordance with ACCA exam requirements.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand the management of accounts receivable and the risks and controls associated with credit. Specifically, this article addresses:

- The purpose of credit policies within the overall credit control process

- How to determine and implement appropriate credit terms for customers

- The procedure for assessing customer creditworthiness and setting credit limits

- The use and accounting for trade and settlement (early payment) discounts

- The effect of credit and discount policy decisions on company liquidity and profitability

- The role of credit control in managing bad debts and minimising credit risks

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following best describes the purpose of a credit policy?

- a) To maximise sales revenue at any cost

- b) To provide a framework for managing customer credit and limiting bad debts

- c) To eliminate all credit sales

- d) To determine the company discount rate with suppliers

-

When offering a settlement discount, what is the primary objective?

- a) To encourage customers to pay later

- b) To increase the list price

- c) To obtain earlier payment and improve cash flow

- d) To increase the accounting workload

-

True or false? Customer credit limits should be the same for all customers to ensure fairness.

-

Briefly explain one risk associated with extending credit without proper assessment.

-

Outline the main difference between a trade discount and a settlement discount.

Introduction

Extending credit to customers can increase sales but also introduces the risk of late payment or non-payment. To manage this, businesses implement a credit policy, establish credit terms for each customer, set credit limits to manage exposure, and apply discount strategies to encourage prompt settlement. Setting and monitoring these elements are key components of effective credit control and essential for financial health.

Key Term: credit policy

A set of principles and procedures established by a company to manage the provision of credit to customers and control the related risks.

SETTING CREDIT TERMS

Offering credit is standard in many industries, but must be managed carefully. The credit terms specify when payment is due and trigger the timing of cash flows.

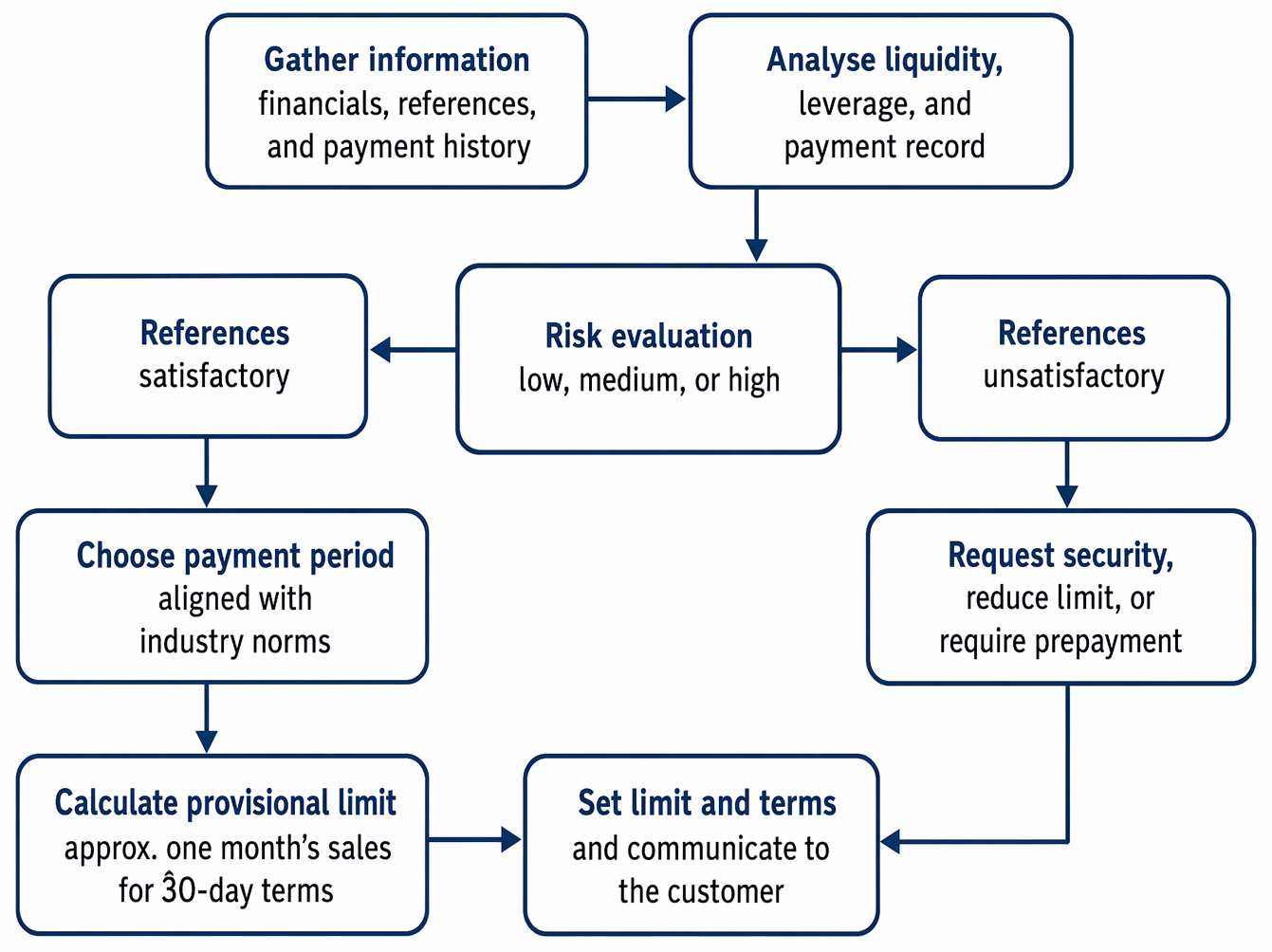

Customer creditworthiness evaluation links liquidity, leverage, and references to payment periods, provisional limits, and security requirements for higher-risk accounts.

Assessing Creditworthiness

Before agreeing to sell on credit, a business should evaluate whether the customer is likely to pay. This often involves reviewing:

- Financial statements

- Credit references

- Payment history

Key Term: credit limit

The maximum outstanding amount a business allows an individual customer to owe at any given time, set to limit potential losses.

Determining Payment Periods

Standard payment terms might be “30 days from invoice,” but can vary based on industry norms, risk appetite, and negotiation. Longer terms may attract customers, but increase the risk of bad debt and reduce available cash.

Key Term: trade discount

A reduction from the list price granted at the time of sale, often to encourage larger orders or customer loyalty. Key Term: settlement discount

A percentage reduction in the invoice price offered to customers for early payment, typically stated as “2% if paid within 10 days.”

Worked Example 1.1

A business sells goods for a list price of $5,000. It offers a trade discount of 10% and a settlement discount of 3% if the invoice is paid within 7 days. The customer buys the goods and pays within 7 days. What amount does the customer pay?

Answer:

Calculate the trade discount: $5,000 × 10% = $500. Invoice after trade discount: $5,000 – $500 = $4,500. Calculate settlement discount: $4,500 × 3% = $135. Amount paid under settlement terms: $4,500 – $135 = $4,365.

SETTING CREDIT LIMITS

Credit limits are not arbitrary. They are set using:

- Customer financial strength

- Size of previous orders

- Expected future orders

- Overall business risk

These limits should be reviewed regularly and adjusted if necessary. Effective credit limits prevent excessive risk concentration in one customer.

Worked Example 1.2

Suppose a customer’s annual sales are $60,000, and their average payment period is 30 days. What is an appropriate credit limit for this customer?

Answer:

Average monthly sales: $60,000 ÷ 12 = $5,000. With 30-day terms, maximum outstanding should equal one month’s sales: $5,000. Set the customer’s credit limit at $5,000, subject to periodic review.

DISCOUNT POLICY DECISIONS

Discount policies are designed to incentivise desired payment behaviour and to balance sales growth with credit risk. The two main types of discounts are:

- Trade discounts: Encourage purchases by offering a lower price at the point of sale.

- Settlement discounts: Encourage faster payment, thereby improving cash flow.

Both have direct impacts on revenue recognition and cash management.

Worked Example 1.3

A business issues an invoice for $2,000 with a 5% settlement discount for payment within 10 days. The customer pays on day 8.

- What amount does the customer pay?

- How should the difference be accounted for?

Answer:

Settlement discount: $2,000 × 5% = $100. Amount paid: $2,000 – $100 = $1,900. The $100 is recognised as a ‘discount allowed’ expense in the seller’s accounts.

CREDIT POLICY ADMINISTRATION AND CONTROL

Credit policies should be documented, communicated internally, and consistently applied. Elements include:

- Customer application forms

- Authorisation for exceptions

- Clear procedures for overdue accounts and debt recovery

Review processes should be in place to:

- Monitor compliance

- Identify trends in overdue debts

- Adjust limits or terms as needed

Exam Warning: Extending generous credit terms or high limits without a formal review process can result in increased bad debt and liquidity problems. ACCA exam questions may test your ability to spot weaknesses in credit control procedures.

Revision Tip: Practice calculating the effects of different discount offers and payment periods on cash flow and profit. Pay attention to the distinction between trade and settlement discounts in exam questions.

Summary

A well-designed credit policy supports profitable sales growth while keeping the risk of bad debts within acceptable levels. Setting appropriate terms, limits, and discount strategies are central to effective credit control.

Key Point Checklist

This article has covered the following key knowledge points:

- The objectives and components of a credit policy

- Methods for assessing customer creditworthiness and setting limits

- The meaning and calculation of trade and settlement discounts

- The role of credit terms and discounts in cash flow management

- The need for ongoing credit control and periodic policy review

Key Terms and Concepts

- credit policy

- credit limit

- trade discount

- settlement discount