Learning Outcomes

After reading this article, you will be able to explain the principles of cash pooling and cash sweeping in group cash management. You will identify how different pooling structures operate, distinguish between physical and notional methods, and evaluate their benefits, risks, and the controls required. You will also be able to apply this knowledge in exam scenarios assessing group cash resource management.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand how organisations manage surplus cash across business units and accounts. You should revise the following areas:

- The operation and objectives of cash pooling and sweeping arrangements in group structures

- The distinction between physical cash concentration (cash sweeping) and notional pooling

- The main advantages and risks associated with group pooling arrangements

- Legal, tax, and regulatory considerations in the movement of funds within a group

- Controls required to safely implement and monitor cash pooling and sweeping practices

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the main purpose of establishing cash pooling arrangements in a group of companies?

- a) Reducing surplus inventory

- b) Centralising available cash to minimise group borrowing and interest costs

- c) Recording revenue faster

- d) Managing payroll

-

Which method of pooling combines account balances without physically transferring funds?

- a) Cash sweeping

- b) Physical concentration

- c) Notional pooling

- d) Invoice discounting

-

List two potential risks associated with a group cash pooling arrangement.

-

Briefly explain what is meant by “zero balancing” in the context of group cash accounts.

Introduction

Efficient use of cash is essential for businesses, especially those operating as part of a group with multiple entities and bank accounts. When cash is spread across many accounts, some companies may have idle balances while others rely on overdrafts or external loans. Cash pooling arrangements provide a structured approach to consolidate surplus funds, improving returns and reducing financing costs for the whole group. For the ACCA FFM exam, understanding the methods, benefits, risks, and control requirements of cash pooling and sweeping is fundamental.

Key Term: cash pooling

Bringing together cash balances from different accounts or legal entities to optimise group liquidity and reduce the need for external borrowing.Test Tip: When revising Cash pooling and sweeping basics, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

CASH POOLING AND SWEEPING ARRANGEMENTS

Cash pooling enables groups of companies to aggregate and use available funds more efficiently. Two primary structures are used: physical cash concentration (cash sweeping) and notional pooling.

Notional pooling presents separate subsidiary balances being combined only for interest purposes, reducing group financing costs without changing legal entitlements.

Physical Cash Concentration (Cash Sweeping)

Physical concentration, often known as cash sweeping, involves the actual transfer of funds from participant accounts to a designated primary account, usually run by the group treasury. This is typically automated and set at a daily frequency. The main effect is that surplus cash from various subsidiaries or business units is centralised, and any overdrafts within the group can be cleared using internal cash rather than incurring external loan costs.

Key Term: cash sweeping

The process of automatically moving surplus balances from individual operating accounts to a central account, usually on a daily basis, to maximise the use of group liquidity. Key Term: zero balancing

A form of cash sweeping where participant accounts are reduced to a zero balance at a fixed interval (e.g. daily) by transferring all surplus cash to a central account.

Notional Pooling

Notional pooling does not require the physical transfer of funds between accounts. Instead, the bank calculates interest for the group by notionally combining the balances of all participant accounts each day. Debit and credit balances are offset, so the group benefits from decreased net interest charges, even though individual subsidiaries’ accounts and entitlements remain unchanged.

Key Term: notional pooling

A cash management system where the balances of multiple group accounts are combined only for interest calculation, without moving actual funds between accounts.

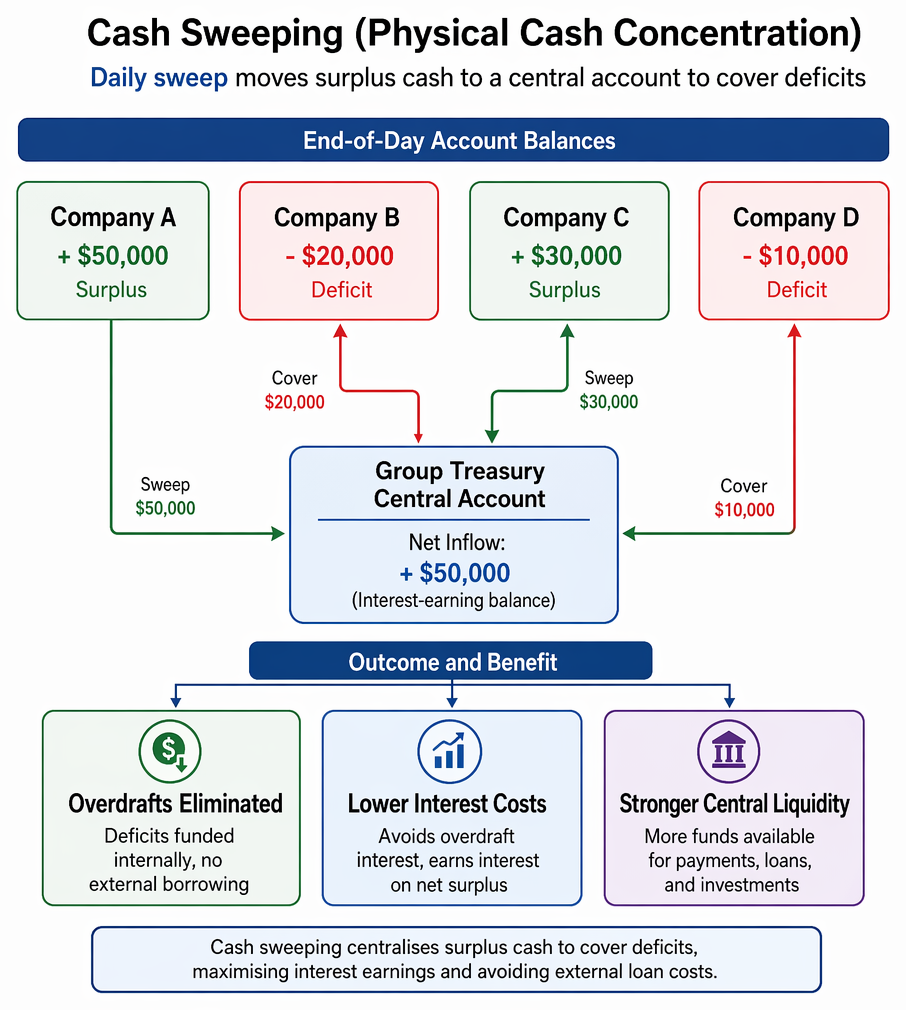

Worked Example 1.1

A group has four companies with the following account balances at the end of a business day: Company A +$50,000, Company B -$20,000, Company C +$30,000, Company D -$10,000. The group uses daily cash sweeping.

Question: What happens during the sweep and how does this benefit the group?

Answer:

At the end of the day, Companies A and C transfer their surplus funds into the group’s central account. The negative balances of Companies B and D are automatically covered by funds in the central account, eliminating overdrafts and external interest costs. The group maximises interest earnings on the consolidated positive balance and avoids unnecessary borrowing.

Advantages of Cash Pooling and Sweeping

- Lower group interest costs by reducing external overdrafts and netting off positive and negative balances

- Stronger central liquidity for paying suppliers, loans, and funding investments without needing extra borrowing

- Centralised control and visibility over group cash, improving treasury management and forecasting

Risks in Cash Pooling Arrangements

Despite the benefits, pooling and sweeping arrangements must be carefully designed, particularly for legal and operational risks.

- Legal risk: Moving funds between entities may create regulatory, tax, or creditor issues. Cross-border movements may face restrictions or special tax rules.

- Operational risk: Automated transfers can fail, or misallocation may leave parts of the group short of working capital.

- Credit risk: If one participant defaults, the pooled group funds may be at risk to the defaulting entity’s creditors.

Exam Warning: Exam questions on cash pooling often require you to explain both the advantages and specific risks (such as intra-group credit exposure, regulatory controls, and documentation of inter-company positions). Remember to mention legal and tax implications as part of a well-rounded answer.

Control Measures for Safe Operation

To ensure safe use of pooling and sweeping, controls are necessary:

- Written agreements clarifying each entity’s rights, responsibilities, and how interest is allocated

- Automated transfer and reconciliation systems with clear audit trails

- Regular compliance checks with banking, tax, and company law regulations in each country

- Monitoring to ensure no unplanned liquidity shortfalls for individual subsidiaries

Worked Example 1.2

A multinational group wants to offset balances among subsidiaries in several currencies without centralising funds, due to local capital controls. Should it use notional pooling or cash sweeping, and why?

Answer:

The group should use notional pooling if legally allowed. This enables offsetting of balances for interest calculation without actually transferring cash, which suits situations with currency or capital movement restrictions. Cash sweeping would likely breach local exchange rules if funds cannot be transferred abroad.

Selection of Structure: Factors to Consider

- Regulatory environment: Many countries limit notional pooling, especially across borders or currencies.

- Group structure: Legal autonomy or minority partners may require notional, not physical, pooling.

- Tax considerations: Inter-company interest may be subject to tax if not properly documented.

- Bank capabilities: Not all banks support all pooling structures, especially for complex, cross-border groups.

Summary

Pooling and sweeping are essential techniques for managing surplus group cash. Physical sweeping moves actual balances to a central account, while notional pooling maintains separate accounts but offsets for interest purposes. Both methods help reduce group interest costs, but each carries specific legal, tax, operational, and credit risks. Safe operation requires robust agreements, systems, and compliance monitoring.

Key Point Checklist

This article has covered the following key knowledge points:

- Define cash pooling, cash sweeping, notional pooling, and zero balancing

- Distinguish between physical cash concentration and notional pooling arrangements

- Identify the main benefits of cash pooling for group liquidity and interest costs

- List key operational, legal, and credit risks in pooling arrangements

- Recognise the core controls and legal considerations needed for secure group cash management

Key Terms and Concepts

- cash pooling

- cash sweeping

- zero balancing

- notional pooling