Learning Outcomes

After reading this article, you will be able to explain why businesses must manage cash surpluses, distinguish between liquidity and yield objectives, and identify common low-risk investment options. You will understand the importance of matching investment periods to cash flow needs and assess how yield and risk interact in short-term financial decisions. You'll also be able to articulate these principles in the context of ACCA exam requirements.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand the principles and practical considerations of managing excess cash. In particular, you must be able to:

- Outline the reasons for and risks associated with holding cash surpluses.

- Distinguish between liquidity and yield as objectives for surplus cash management.

- List and explain characteristics of common short-term investment vehicles.

- Recognise the need to match cash investments' maturity with future cash outflows.

- Describe the trade-off between liquidity, yield, and risk in short-term fund management.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which priority usually takes precedence when managing a short-term cash surplus?

- a) Maximising yield

- b) Guaranteeing liquidity

- c) Taking higher investment risk for greater return

- d) Investing for the long term

-

A business considers locking surplus cash into a six-month fixed deposit, but expects it may need the funds in three months. What is the main risk in doing this?

-

Name two low-risk, high-liquidity investment instruments commonly used for surplus cash.

-

True or false? Funds placed in shares are usually considered an appropriate option for short-term cash surplus management.

Introduction

Most organisations experience periods when cash receipts temporarily exceed payments. Unless invested wisely, these surpluses provide no return and can quickly erode through inflation or missed opportunities. Effective management of cash surpluses means deciding where and how to place excess cash so that the business has funds available when needed, but also earns the best possible return without taking inappropriate risks.

Managing short-term cash is a balancing act involving three main factors: how quickly the funds can be accessed (liquidity), how much return they generate (yield), and the probability that the invested funds might be lost (risk). Getting this balance right is critical in financial management and frequently tested in the ACCA FFM exam.

Key Term: cash surplus

Cash held by a business that exceeds the amount needed for day-to-day operations, which may be temporarily available for short-term investment.Test Tip: When revising Liquidity, yield, and risk trade-offs, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

WHY MANAGE CASH SURPLUSES?

Holding surplus cash in a non-interest-bearing account or as cash-in-hand means the business forgoes potential earnings. However, tying up those funds in high-yield but risky or illiquid investments could mean they are not available when required, or worse, the funds could be lost if the investment fails.

The goal, therefore, is to earn a suitable return on idle cash while ensuring funds are available when needed. The best option often depends on the cash flow forecast, risk appetite, and short-term market conditions.

Key Term: liquidity

The ease and speed with which an asset can be converted into cash without significant loss of value. Key Term: yield

The income return—usually expressed as an annual percentage—earned from an investment, such as interest or dividends. Key Term: risk

The likelihood that an investment will lose value or will not be repaid when due.

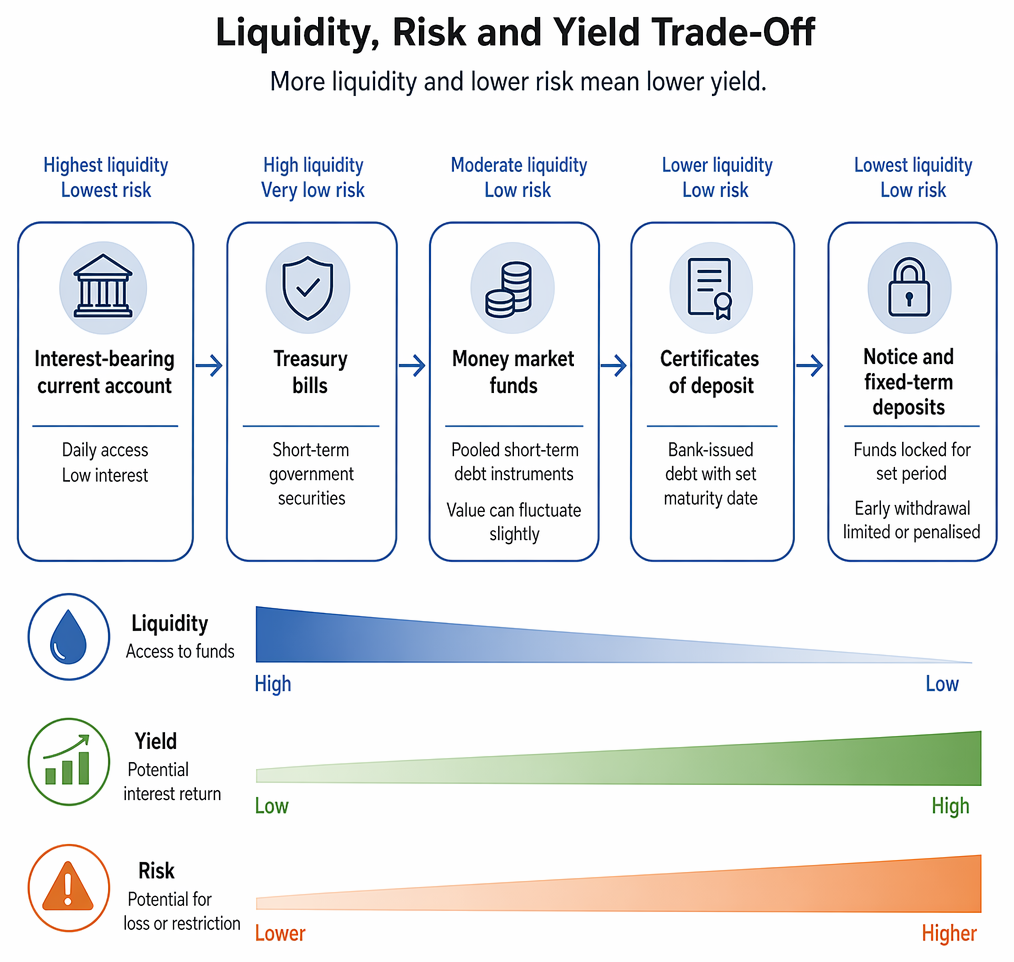

LIQUIDITY, YIELD, AND RISK: THE TRADE-OFF

A business managing surplus funds faces a fundamental trade-off:

Surplus cash placement follows maturity matching to forecast outflows, then assessment of yield and provider credit quality.

- High liquidity assets (such as a current account) are always available but may offer little or no return.

- Assets with higher yield (such as fixed-term deposits or commercial paper) generally lock money away for a fixed period or may involve extra risk.

- Riskier assets may offer the best returns but could be unsuitable if short-term access to funds is needed.

The central principle: the more accessible (liquid) and lower-risk an investment is, the lower the yield tends to be.

SHORT-TERM INVESTMENT VEHICLES

Short-term opportunities for investing surplus cash include:

- Interest-bearing current accounts: Provide daily access to funds, minimal risk, but often low interest.

- Notice and fixed-term deposits: Offer higher interest in exchange for committing funds for a set period (e.g., 7, 30, or 90 days). Withdrawing early may incur penalties or be restricted.

- Treasury bills: Short-term government securities (usually one to twelve months) regarded as very low risk and highly liquid.

- Money market funds: Pooled investments mainly in low-risk, short-term debt instruments. Offer better returns than a current account, but value can fluctuate slightly.

- Certificates of deposit (CDs): Bank-issued debt securities with a set maturity date, usually offering a fixed interest rate.

Key Term: money market instrument

Tradable financial instrument (such as a treasury bill, commercial paper, or certificate of deposit) with short maturity and usually low risk, used for short-term investing.

Worked Example 1.1

A business has a cash surplus of £40,000 that it will not need for 30 days. It considers the following:

- Leave funds in its current account (0.1% annual interest), or

- Place the cash in a 30-day term deposit paying 2% annual interest, with no early access.

If unexpected bills must be paid in 20 days, what is the trade-off?

Answer:

By choosing the term deposit, the business earns more interest (£66 compared to £3 for 30 days). However, the money cannot be accessed if needed early, which introduces liquidity risk. If the funds are needed before 30 days, the business may have to borrow or miss payments.

MATCHING MATURITY TO CASH NEEDS

A sound cash management policy requires matching the investment period (maturity) with the expected timing of cash outflows. Investing in instruments that mature just before the funds are required reduces liquidity risk without unduly sacrificing yield.

Keeping too much cash uninvested sacrifices return, but tying funds up for too long or in risky investments exposes the business to unnecessary risk or liquidity shortages.

Worked Example 1.2

Zara Ltd forecasts it will need £100,000 for tax payments in exactly two months. The options are:

- Invest in a 60-day treasury bill at 1.7% interest (reaches maturity the day before the tax is due),

- Or, invest in a 90-day deposit at 2.2% interest.

Should Zara Ltd consider the higher-yield 90-day deposit?

Answer:

The 90-day deposit matures after the tax payment is needed, so funds will not be available on time—this introduces liquidity risk, even though the yield is slightly higher. The 60-day treasury bill matches Zara's timing and is the safer option, even at slightly lower yield.

RISK MANAGEMENT AND SECURITY

Preserving capital is often the top priority for short-term surplus. Sound policy means avoiding speculative or high-volatility assets (like shares or cryptocurrencies) for short-term funds, as their value may drop suddenly, making them unsuitable for cash required soon.

Businesses should also consider the credit rating of investment providers. A high interest rate offered by a financially weak bank or corporation could signal elevated risk of loss.

Exam Warning: Do not confuse the objectives of short-term cash surplus management with those of long-term investment. For ACCA exams, remember that liquidity and safety usually come before maximizing yield when surplus funds are only available for a short time.

Summary

To manage surplus cash effectively, businesses should:

- Prioritise liquidity for short-term funds.

- Seek reasonable yield only if risk and liquidity requirements are met.

- Match maturity of investments closely to anticipated cash needs.

- Avoid high-risk or illiquid investments when funds may be needed soon.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain why managing cash surpluses is needed in a business.

- Define and distinguish liquidity, yield, and risk.

- List and describe the main short-term investment options for surplus cash.

- Explain the trade-off between liquidity, yield, and risk.

- Recognise the importance of matching investment maturity with cash flow timing.

- Understand why safety typically outweighs yield for short-term surpluses.

Key Terms and Concepts

- cash surplus

- liquidity

- yield

- risk

- money market instrument