Learning Outcomes

After reading this article, you will be able to explain the importance of monitoring accounts receivable, interpret and prepare an aged receivables analysis, apply key performance indicators (KPIs) for collection effectiveness, and calculate and account for provisions such as bad debts and allowance for receivables. You will also recognise how effective credit management impacts the financial statements.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand how receivables are monitored, measured, and controlled, and the related accounting processes. Specifically, revision for this topic should focus on:

- The definition and purpose of aged receivables analysis in monitoring credit control

- Key performance indicators (KPIs) relevant to receivable collection (e.g., receivables days, ageing breakdown)

- The nature, calculation, and accounting treatment of irrecoverable debts and allowances for receivables

- The effect on profit and assets of creating and adjusting provisions (allowances) for doubtful debts

- The relevance of effective monitoring and provisioning to financial reporting and decision-making

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the purpose of preparing an aged receivables analysis?

- If a business’s average receivables collection period is increasing, what could this indicate about its credit control?

- How is an allowance for receivables different from writing off an irrecoverable debt?

- True or false? All debts that remain unpaid for over 90 days should be written off immediately as irrecoverable.

- Which KPI compares year-end receivables to sales to show average collection duration?

Introduction

The prompt and reliable collection of money owed by customers is essential for a business’s liquidity and profitability. Poor management of receivables can lead to cash flow problems, increased credit risk, and eventually irrecoverable bad debts. To prevent this, businesses use tools such as aged receivables analysis and performance indicators to monitor the effectiveness of their credit policies. They also estimate and account for the possibility of non-payment using provisions, following the principle of prudence in accounting.

This article covers the main methods used to review outstanding debts, measure collection efficiency, and set prudent allowances for doubtful debts, all in line with ACCA exam requirements.

Key Term: aged receivables analysis

A report showing how long amounts owed by customers have been outstanding, grouped by overdue periods (e.g., current, 30 days, 60 days, etc.), to identify potential collection issues.

ANALYSING RECEIVABLES: AGED RECEIVABLES ANALYSIS

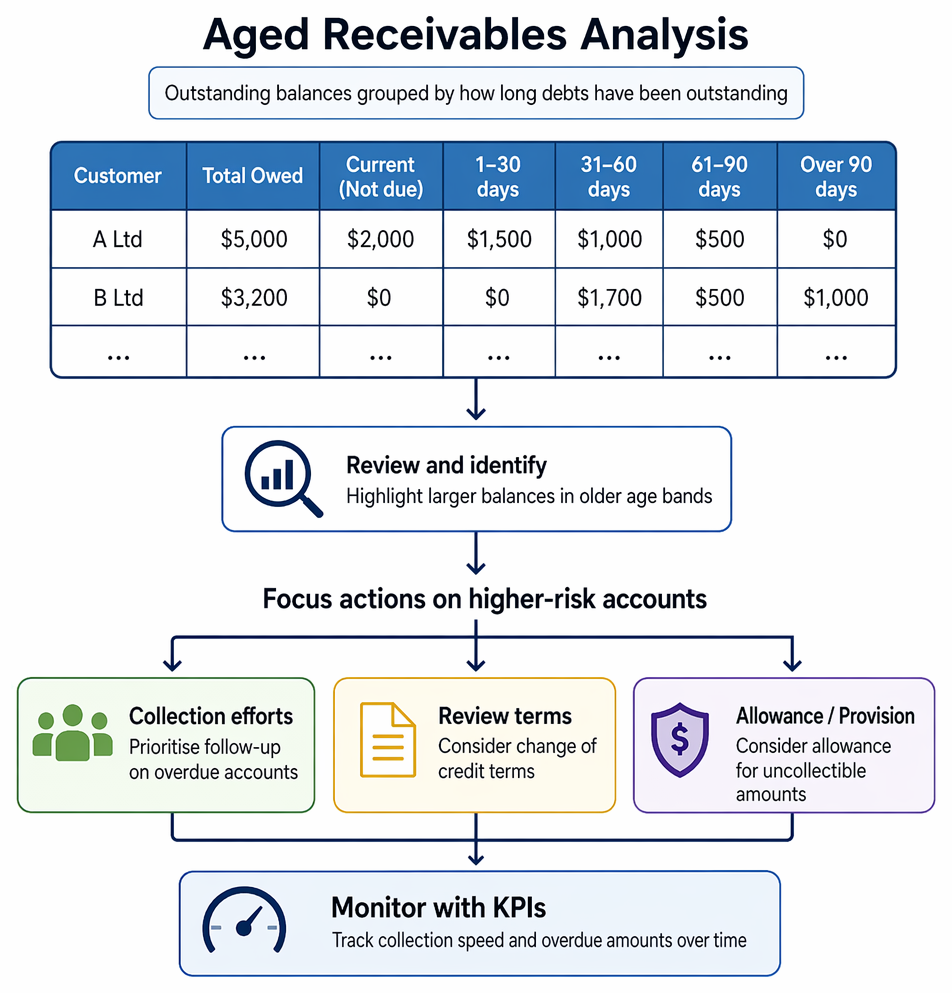

An aged receivables analysis is a practical report listing each customer’s outstanding balance, categorised by how long the debt has been outstanding (e.g., Not due, 1–30 days overdue, 31–60 days, etc.). This report helps businesses:

Customer balance assessment routes confirmed losses to write-off and uncertain exposures to specific or general allowances, with profit and balance-sheet effects.

- Identify customers who are slow to pay

- Focus collection efforts on higher-risk accounts

- Monitor adherence to credit terms

- Calculate provisions for doubtful debts more effectively

Key Term: key performance indicator (KPI)

A quantifiable measure used to assess progress towards a business objective, such as collection speed or overdue amounts in receivables management. Key Term: allowance for receivables

A provision raised in the accounts to reflect the estimated amount of receivables that may prove uncollectible, based on historical experience and current circumstances.

The analysis may be generated monthly and is often presented as below:

| Customer | Total Owed | Current | 1–30 days | 31–60 days | 61–90 days | Over 90 days |

|---|---|---|---|---|---|---|

| A Ltd | $5,000 | $2,000 | $1,500 | $1,000 | $500 | $0 |

| B Ltd | $3,200 | $0 | $0 | $1,700 | $500 | $1,000 |

| ... | ... | ... | ... | ... | ... | ... |

Aged analysis highlights problem debts that may need further action—collection efforts, change of terms, or consideration for allowance/provision.

MONITORING EFFECTIVENESS: COLLECTION KPIs

Businesses use several KPIs to monitor collection performance and the efficiency of credit control:

- Receivables collection period (or ‘days sales outstanding’): Indicates the average number of days it takes to collect receivables.

- Overdue receivables ratio: Proportion of receivables overdue (per aged analysis) to total receivables.

- Bad debts ratio: Total irrecoverable debts written off as a % of credit sales.

These KPIs help management:

- Identify trends in payment delays

- Benchmark collection efficiency

- Detect weakening controls or deteriorating customer quality

Worked Example 1.1

A company has closing trade receivables of $36,500 and total credit sales for the year of $292,000. Receivables of $5,000 are over 60 days overdue and $2,000 are over 90 days overdue.

Calculate: (a) the receivables collection period, and (b) the percentage of overdue receivables (over 60 days).

Answer:

(a) Receivables collection period = ($36,500 / $292,000) × 365 = 45.6 days. (b) Overdue >60 days = ($5,000 + $2,000)/$36,500 = $7,000 / $36,500 = 19.2%.Revision Tip: Be familiar with both the calculation and interpretation of collection period and overdue receivables ratios for ACCA exam questions.

PROVISIONING: IRRECOVERABLE DEBTS AND ALLOWANCES

As not all customers will pay, businesses apply prudence by making provisions for potential losses:

- Irrecoverable debts (‘bad debts’): Debts that are specifically known to be uncollectible are written off directly as an expense.

- Allowance for receivables (provision): An estimate of debts that may become irrecoverable, based on experience, current customer conditions, or age analysis.

Key Term: irrecoverable debt

An amount owed by a customer that is considered certain not to be collected and is therefore written off as an expense.

An allowance can be general (e.g., 2% of total receivables) or specific (e.g., based on the ages and risks per the aged analysis).

Worked Example 1.2

At 31 December, TRH Ltd had trade receivables of $40,000. It decides to write off $1,500 as irrecoverable and to create an allowance for receivables of 5% of the remaining balance.

What is the allowance to be set up, and how are these adjustments recorded?

Answer:

Adjusted receivables after write-off = $40,000 – $1,500 = $38,500. Allowance = 5% × $38,500 = $1,925. Journal entries:

- Dr Irrecoverable debts expense $1,500 Cr Receivables $1,500 (write off bad debt)

- Dr Irrecoverable debts expense $1,925 Cr Allowance for receivables $1,925 (set up allowance)

Worked Example 1.3

A business increased its allowance for receivables from $2,000 to $3,400 during the year. What is the impact on the statement of profit or loss and financial position?

Answer:

The increase in allowance ($1,400) is charged to profit as an expense. The closing balance of allowance ($3,400) is shown as a deduction from receivables in current assets in the statement of financial position.Exam Warning: Do not confuse writing off a debt (removing a specific amount from receivables and recording an expense) with increasing an allowance (setting aside an estimated amount for potential losses).

IMPACT OF MONITORING AND PROVISIONING ON FINANCIAL STATEMENTS

Effective receivables monitoring and provisioning:

- Prudent reporting: Ensures assets are not overstated and losses are not ignored

- Affects profit: Higher provisions decrease reported profit

- Affects the balance sheet: Allowance is deducted from trade receivables, showing the net expected to be collected

- Supports management action: KPIs and aged analysis highlight collection weaknesses and may prompt tighter credit terms

Worked Example 1.4

A retailer’s aged analysis shows 30% of its receivables are over 90 days. Management has not made any allowance in the accounts. What accounting issue does this pose?

Answer:

Not recognising an allowance may result in trade receivables being overstated and profit being exaggerated, breaching the prudence principle.

Summary

Monitoring receivables using aged analysis and KPIs helps highlight credit risks early and supports better cash flow management. Sound provisioning using a suitable allowance reflects the realisable value of receivables and promotes fair reporting in line with accounting standards.

Key Point Checklist

This article has covered the following key knowledge points:

- The use and interpretation of aged receivables analysis to monitor credit risk

- Calculation and significance of key receivables KPIs (e.g., collection period, overdue ratios)

- Distinction between irrecoverable debt write-off and an allowance for receivables

- The accounting entries and financial statement effect of provisioning for doubtful debts

- Why prudent receivables management supports accurate profit and asset reporting

Key Terms and Concepts

- aged receivables analysis

- key performance indicator (KPI)

- allowance for receivables

- irrecoverable debt