Learning Outcomes

After studying this article, you will be able to identify and describe key sources of finance available to businesses, distinguishing between debt finance, leasing, and hybrid instruments. You will learn the features, advantages, and disadvantages of debt, leases, and hybrid finance, and understand related accounting principles and implications for businesses, as required by the ACCA Foundations in Financial Management (FFM) syllabus.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand the nature and selection of various sources of business finance. In particular, you should be confident with:

- The features and practical uses of debt instruments, including bank loans, overdrafts, and bonds

- Accounting and business implications of finance and operating leases

- The concept and application of hybrid instruments such as convertible debt and preference shares

- The benefits, risks, and suitability of these finance sources for different types of business needs

- The impact of finance choice on the financial statements and ratios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is a key feature that distinguishes a lease from a loan?

- a) Ownership remains with the lessee from the outset

- b) Usage of an asset is separated from legal ownership

- c) All payments must be made at the start of the agreement

- d) Repayments always include a variable interest rate

-

A company issues convertible bonds. These are best described as:

- a) Ordinary shares with guaranteed dividends

- b) Overdrafts secured on inventory

- c) Debt that may be exchanged for shares at a future date

- d) Preference shares with no voting rights

-

State two advantages and two potential disadvantages for a business using finance leases compared to purchasing assets outright.

-

True or false: Interest on borrowings is always reported as an expense in the statement of profit or loss for limited companies.

Introduction

Businesses commonly require external finance to fund expansion, asset purchases, or ongoing working capital needs. Selecting the appropriate type of finance is critical, as each source has different features, costs, and effects on the company’s accounts. This article examines three main categories of external finance: debt finance, leasing arrangements, and hybrid instruments, highlighting their characteristics, implications, and related accounting treatments.

Test Tip: When revising Debt finance, leases, and hybrid instruments, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

DEBT FINANCE

Debt finance refers to funds borrowed with an agreement to repay both principal and interest, without granting ownership rights to the lender.

Main Types of Debt Finance

Bank loans: Offered for fixed periods and amounts, with interest payable at a fixed or variable rate. Usually secured against company assets.

Bank overdrafts: Flexible borrowing up to an agreed limit, typically at a higher interest rate and repayable on demand. Often used for short-term cash flow fluctuations.

Bonds or loan notes: Longer-term, fixed-sum borrowings issued to a range of investors, with regular interest payments (known as coupons).

Key Term: Debt finance

Borrowed funds that must be repaid with interest, without affecting the company's equity ownership.

Features, Advantages, and Disadvantages

- Repayable over a defined period

- Interest payments are usually tax-deductible

- Lender has no ownership or control over business operations

Benefits include predictability and retention of ownership, while drawbacks comprise mandatory repayments, interest costs, and potential obligations to provide collateral.

Worked Example 1.1

Question: A limited company obtains a $100,000 bank loan at 6% interest for five years. How will this be recognised in its accounts, and what financial statement impacts occur?

Answer:

The company will recognise a non-current liability for the principal outstanding. Each year, the interest expense (6% of the outstanding balance) is reported in profit or loss. Loan repayments reduce the liability and cash balance.Exam Warning: Confuse neither the cost of debt finance (interest on borrowings) with dividends paid to shareholders, nor interest-bearing debt with equity. Ensure you can distinguish debt from equity in both finance source and financial statement presentation.

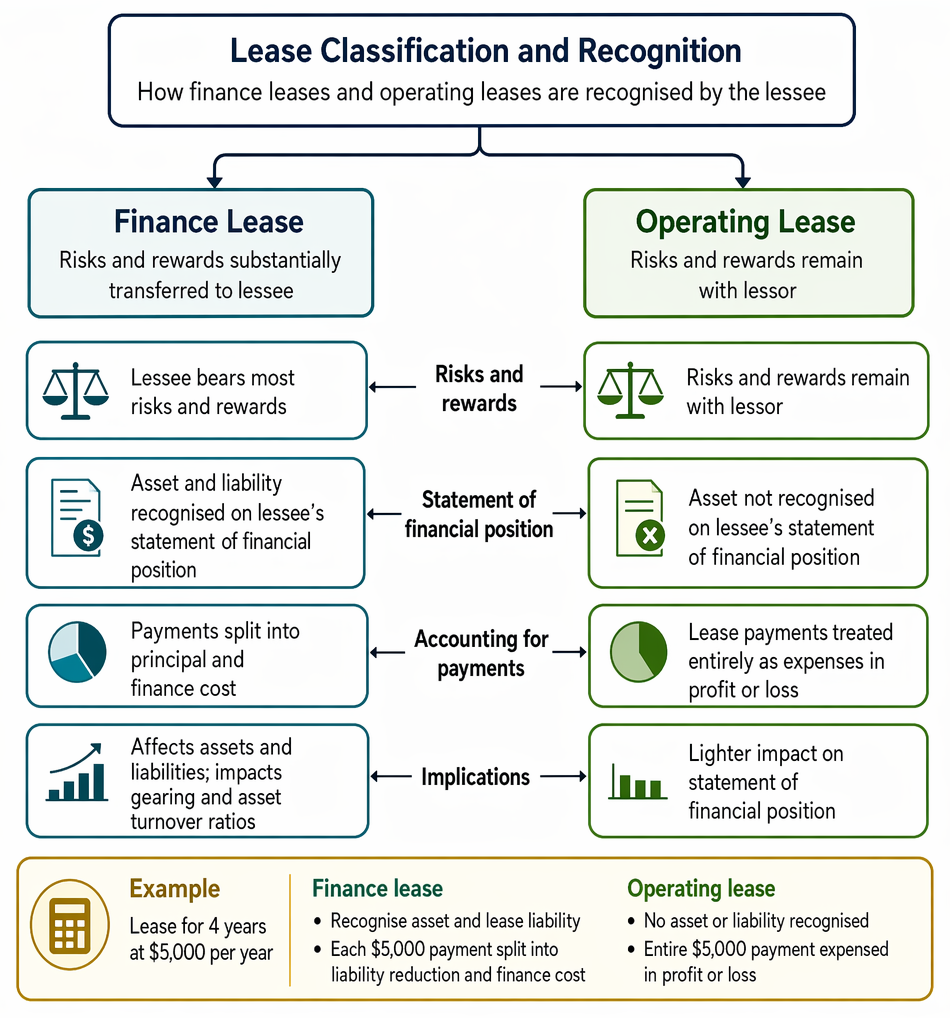

LEASES

Leasing allows a business to use assets without buying them outright. Leases fall into two categories: finance leases and operating leases.

Hybrid instruments are classified as liabilities or equity according to their terms, determining whether returns are finance costs or equity dividends.

Key Term: Lease

A contract granting the right to use an asset over an agreed period in exchange for regular payments, without immediate transfer of ownership. Key Term: Finance lease

A lease arrangement that substantially transfers risks and rewards of asset ownership to the lessee, leading to on-balance-sheet recognition. Key Term: Operating lease

A lease where the risks and rewards of asset ownership remain with the lessor, and the asset does not appear on the lessee’s statement of financial position.

Finance Lease

- Lessee (user) bears most risks and rewards

- Asset and liability both recognised on the lessee's statement of financial position

- Payments split into principal and finance cost

Operating Lease

- Ownership risks/rewards remain with the lessor (owner)

- Lease payments treated entirely as expenses in profit or loss

- Asset not recognised by the lessee

Key Differences and Implications

- Finance leases affect both assets and liabilities, impacting gearing and asset turnover ratios

- Operating leases typically have a lighter impact on the statement of financial position

Worked Example 1.2

Question: Company A leases an asset under a finance lease for four years, agreeing to pay $5,000 per year. How does the recognition differ from an operating lease?

Answer:

For a finance lease, Company A recognises the leased asset and a lease liability. Annual payments are split between reducing liability and finance cost in profit or loss. In an operating lease, only the annual lease payment is expensed; no asset or liability is recognised.

HYBRID INSTRUMENTS

Hybrid instruments possess both debt and equity characteristics and are used to raise finance while providing flexibility.

Types of Hybrid Instruments

Convertible debt: Debt instruments, such as bonds or loan notes, that can be converted into shares at the holder's option.

Preference shares: Shares granting the holder a fixed dividend, with potential for repayment (redeemable) or indefinite duration (irredeemable). Can resemble either debt or equity depending on terms.

Key Term: Hybrid instrument

A financial instrument exhibiting traits of both debt and equity; for example, convertible bonds or preference shares.

Why Use Hybrid Instruments?

- Attract investors seeking fixed income with potential equity upside

- Often cost less than pure equity or debt in terms of required investor return

- Provide companies with funding while deferring potential dilution of shareholder control

Accounting and Statement Presentation

- The classification in financial statements depends on specific terms: redeemable preference shares and convertible debt are generally treated as liabilities; irredeemable preference shares as equity.

Worked Example 1.3

Question: XYZ Ltd issues $50,000 of convertible loan notes, which may be converted to shares after three years. How is this instrument presented in the statement of financial position?

Answer:

Until conversion, the loan notes are classified as liabilities. On conversion, they are transferred to share capital and share premium as applicable. Interest paid before conversion is treated as a finance cost in profit or loss.

Summary

Selecting appropriate finance requires understanding the distinguishing features, advantages, and effects of debt, leases, and hybrid instruments. The choice affects a business's financial risk, tax position, and how results are presented in financial statements.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and explain debt finance and its distinction from equity

- Identify main types of business debt—loans, overdrafts, bonds

- Explain key features of finance leases and operating leases, and how to account for each

- Recognise the main types of hybrid instruments: convertible debt and preference shares

- Describe the benefits and drawbacks of each finance type for businesses

- Understand accounting implications for each finance source in financial statements

Key Terms and Concepts

- Debt finance

- Lease

- Finance lease

- Operating lease

- Hybrid instrument