Learning Outcomes

After reading this article, you will be able to explain the concept of the time value of money and apply present value and annuity calculations to typical ACCA FFM exam questions. You will know how to calculate and interpret present values for single cash flows and annuities, use discounting and compounding in decision-making, and identify when to use different formulas or tables.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand the core techniques for evaluating the value of money over time and applying these to financial decisions. Specifically, you should be able to:

- Define and apply the concept of the time value of money

- Calculate the present value and future value of single amounts and regular cash flows (annuities)

- Use discounting and compounding techniques to evaluate cash flows

- Recognise and apply the correct formulas or tables for exam questions on present value and annuity calculations

- Distinguish between different types of cash flow streams and select the correct calculation method

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What does the time value of money principle state about $1 received today compared to $1 received in a year’s time?

- a) No difference

- b) $1 today is worth less

- c) $1 today is worth more

- d) Depends on inflation only

-

You are offered $10,000 today or $10,800 in one year. If the discount rate is 12%, which option is worth more in present value terms?

-

Calculate the present value of $1,500 received at the end of each year for 5 years if the discount rate is 8% per year.

-

True or false? An ordinary annuity assumes payments are made at the beginning of each period.

Introduction

Most financial decisions involve comparing cash flows that occur at different times. The time value of money reflects the fact that money received today can be invested to earn interest, making it worth more than the same nominal amount received in the future. This article explains the key concepts and calculations needed to assess present values, future values, and annuities, as required for ACCA FFM exam questions.

Key Term: time value of money

The principle that a sum of money has greater value now than the same sum at a future date, owing to its potential to earn interest.

PRESENT VALUE AND DISCOUNTING

Present Value of a Single Future Amount

To compare cash flows at different dates, all must be expressed at a single point in time. Present value (PV) is the value today of a sum to be received in the future, discounted at an appropriate rate.

Key Term: present value

The current value of a future sum of money discounted at a specified rate.

The formula for calculating the present value of a single cash flow receivable after n years at discount rate r:

where:

- PV = present value

- FV = future value (lump sum)

- r = discount rate (expressed as a decimal)

- n = number of periods

Key Term: discounting

The process of calculating the present value of a future sum by applying a discount rate.

Discounting and Compounding

Discounting brings a future value back to its present value. The opposite process is compounding, which projects a present sum forward to its value at a future date.

Key Term: compounding

The process of determining a future value by adding interest to a present sum over time.

ANNUITY CALCULATIONS

Single-sum discounting is presented as steps to determine amount, rate and periods, select a factor, derive present value, and compare options.

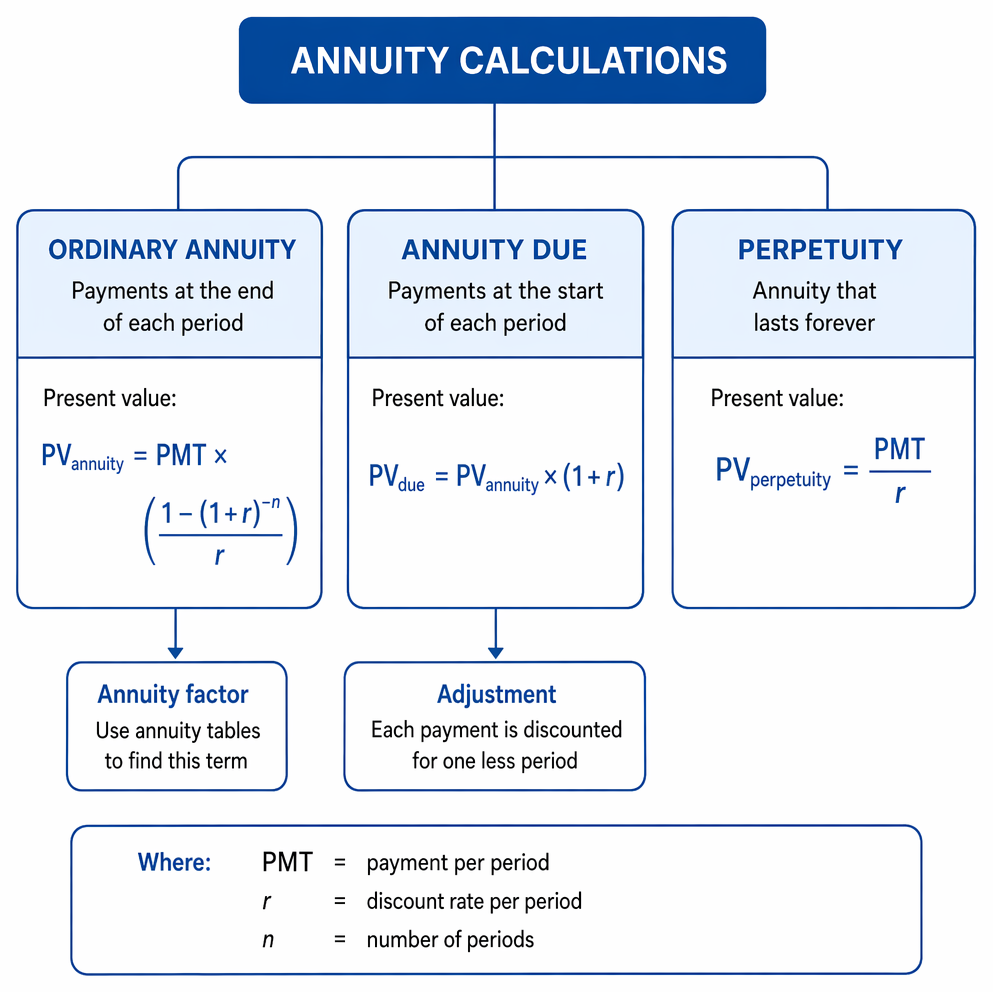

Ordinary Annuities

An annuity is a regular series of equal payments, either received or paid. An ordinary annuity means payments are made at the end of each period.

Key Term: annuity

A sequence of equal payments or receipts made at regular intervals.

The present value of an ordinary annuity is calculated as:

where:

- = payment per period

- = discount rate per period

- = number of periods

You can use annuity tables in the exam to find the bracketed term above ("annuity factor").

Annuity Due

If payments are made at the start of each period, it is called an annuity due. The present value is adjusted since each payment is discounted for one less period.

Perpetuities

A perpetuity is an annuity that lasts forever. Its present value is:

APPLICATIONS OF DISCOUNTING AND ANNUITY CALCULATIONS

Present value and annuity calculations are required in many ACCA exam contexts, including project appraisal, lease evaluation, loan repayments, and asset valuation.

Worked Example 1.1

Calculate the present value of $5,000 receivable in 3 years’ time if the discount rate is 6% per annum.

Answer:

Using the formula: PV = \frac{5,000}{(1 + 0.06)^3} = \frac{5,000}{1.191016} = \4,197 $ (rounded to the nearest dollar)

Worked Example 1.2

A business will receive $2,000 each year at the end of the next four years. The discount rate is 8%. What is the present value of these cash flows?

Answer:

Find the 4-year, 8% annuity factor from the annuity table (or calculate as above): Annuity factor ≈ 3.3121 Present value = $2,000 × 3.3121 = $6,624 (rounded to nearest dollar)

Worked Example 1.3

Calculate the present value of a perpetuity of $400 per year if the discount rate is 5%.

Answer:

Exam Warning: Routinely check whether the question refers to cash flows at the start or end of each period—ordinary annuities and annuities due have different present values.

Revision Tip: Always use the present value or annuity tables provided in your exam. Practice selecting the correct factors based on the number of periods and the stated discount rate.

Summary

The time value of money requires converting all future cash flows to present values before making decisions. Annuity and perpetuity calculations let you handle regular streams of payments effectively using standard formulas or tables. Competence with these techniques is essential for passing calculation-based ACCA FFM exam questions.

Key Point Checklist

This article has covered the following key knowledge points:

- Define the time value of money and why $1 today is worth more than $1 tomorrow

- Calculate present value for single cash flows using the discounting formula

- Distinguish between compounding (FV) and discounting (PV)

- Apply annuity formulas to regular series of payments, using PV tables where permitted

- Recognize differences between ordinary annuities, annuity due, and perpetuities

- Select the correct discount rate and period for exam calculations

Key Terms and Concepts

- time value of money

- present value

- discounting

- compounding

- annuity