Learning Outcomes

After reading this article, you will be able to explain the main dividend theories relevant to the ACCA FM exam. You will understand the impact of clientele and signaling on dividend policy, describe common constraints such as legal restrictions and liquidity, and evaluate how practical factors shape real-world dividend decisions and share prices.

ACCA Financial Management (FM) Syllabus

For ACCA Financial Management (FM), you are required to understand the theoretical and practical influences on dividend policy. In particular, you should be comfortable with:

- The key theories of dividend policy, including the impact of signaling and clienteles on share prices

- How taxation, investor preferences, and market imperfections shape dividend decisions

- Legal, liquidity, and contractual constraints on the payment of dividends

- The practical implications of dividend policy for shareholder wealth and company strategy

- The relevance of alternative forms of distributions, such as share repurchases and scrip dividends

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which statement best describes the clientele effect in dividend policy?

- a) Companies target dividends solely based on directors' preferences.

- b) Investors group around companies whose dividend policy matches their tax preferences.

- c) All firms must pay the same dividend to attract investors.

- d) Dividend decisions are always irrelevant to share price.

-

Why might a cut in dividend send a "bad news" signal to shareholders?

- a) It always indicates a fall in profits.

- b) It may lead investors to believe management expects weaker future cash flows.

- c) It usually means a bonus share issue is planned.

- d) It makes the share more attractive to institutional investors.

-

List two main practical constraints that can limit a company’s ability to pay dividends.

-

If a firm chooses not to pay a cash dividend but instead offers a scrip dividend, what is the main difference?

Introduction

Dividend policy—the choice of how much profit to return to shareholders versus retaining for reinvestment—affects not just cash flows but also investor perceptions and share price. While dividend irrelevance theory suggests that payout policy should have no impact in the absence of market imperfections, in practice, real-world factors such as investor clienteles, signaling effects, and constraints like liquidity or legal rules play a critical role. Understanding these factors is essential for success in the ACCA FM exam.

Key Term: dividend policy

The strategy a company uses to determine the size, timing, and form of distributions made to shareholders, typically as cash dividends or share alternatives.Test Tip: When revising Clientele, signaling, and constraints, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Dividend Theories and Their Practical Implications

Dividend decisions are influenced by both theoretical viewpoints and practical factors. The sections below examine key theories and the practical constraints impacting real-world dividend policy.

Investor tax positions and income requirements shape dividend clienteles, with payout policy changes affecting shareholder turnover and share price.

The Clientele Effect

Dividend policy can influence the type of investors attracted to a company—a phenomenon known as the clientele effect.

Key Term: clientele effect

The tendency for investors to be attracted to firms whose dividend policies align with their income needs and tax positions, resulting in distinct groups (clienteles) of shareholders across different companies.

Retired individuals, for example, may prefer steady cash dividends to meet regular expenses. In contrast, higher-rate taxpayers may prefer capital gains (in the form of reinvested earnings or share price growth), as these may benefit from more favourable tax treatment compared to dividends.

Because companies tend to attract shareholders with similar preferences, changes in dividend policy may risk losing part of their existing shareholder base. However, this also means that abrupt shifts in dividend policy can be destabilising.

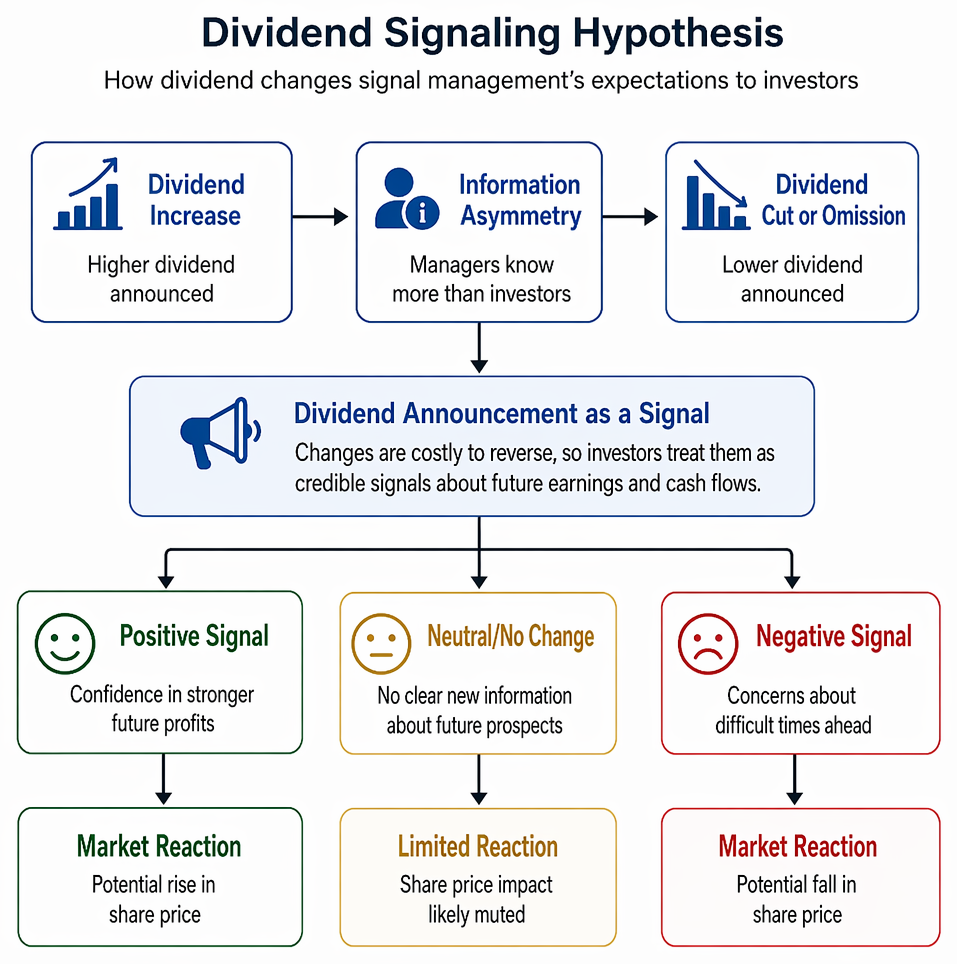

Dividend Signaling Hypothesis

Dividend changes often convey information beyond the amount paid. This is the basis of the signaling hypothesis.

Key Term: signaling hypothesis

The theory that changes in dividend payments are interpreted by investors as signals about management’s expectations of future earnings and cash flows.

When a company increases its dividend, investors may see this as a signal of management’s confidence in future profits. Conversely, a cut or omission can be interpreted as a warning of difficult times ahead, potentially leading to a fall in share price—even if short-term profits remain healthy.

Key Term: information asymmetry

A situation where company managers possess better information about the firm’s prospects than outside investors.

The signaling effect arises from information asymmetry. Since managers usually know more than shareholders, the dividend announcement provides a credible (costly to reverse) signal about the company’s expected performance.

Practical Constraints on Dividend Policy

Company law and financial realities can restrict the ability to pay dividends, often regardless of investor preferences.

Legal and Regulatory Constraints

A business can only pay dividends from distributable profits as defined by law. This means:

- Dividends cannot be paid from unrealised or revaluation reserves.

- Creditor protection rules may limit payout levels.

Lenders may also impose covenants restricting dividends until certain financial conditions are met.

Liquidity Constraints

Even when sufficient accounting profits exist, a lack of available cash may prevent real dividend payments.

Companies also need to ensure they maintain enough working capital to fund ongoing operations. Distributing too much as dividends risks cash shortfalls.

Contractual Limitations

Loan agreements or bond covenants can restrict dividend payments to protect lenders’ interests. Such restrictions help prevent the company from distributing funds that may threaten its ability to meet debt obligations.

Alternative Dividend Forms: Scrip, Bonus Issues, and Share Repurchases

Companies sometimes offer shareholders dividends in the form of new shares (scrip dividends) rather than cash. Alternatively, they may make bonus issues (capitalising reserves), which increase the number of shares held but do not provide cash. Share buybacks can also be used to return value, often offering more tax-efficient alternatives in some jurisdictions.

Worked Example 1.1

A company has a stable, older shareholder base that relies on regular cash dividends. Management decides to suspend the dividend to finance investment in new projects. What are the likely consequences for shareholder reaction and share price?

Answer:

Investors attracted to the regular dividend may sell their shares if the payout is suspended, causing a shift in clientele. Additionally, such an abrupt change could signal management’s concerns, regardless of public statements, potentially leading to a fall in share price due to both clientele effect and negative signaling.

Worked Example 1.2

XYZ Ltd announces a 30% increase in its annual dividend despite flat profits. How might investors interpret this, and what risks could arise for the company?

Answer:

Investors may interpret the increase as a positive signal about future earnings growth. If management cannot deliver such growth, future dividend reductions may then trigger a sharp negative market response—a risk of damaging credibility and investor confidence.Exam Warning: Dividend irrelevancy theory assumes perfect markets without taxes, transaction costs, or information asymmetry. In real-world ACCA FM exam scenarios, expect to discuss how practical factors like signaling and clientele override the basic theory.

Summary

Dividend policy decisions are shaped by more than abstract theory. The clientele effect explains the existence of shareholder groups with differing preferences, while the signaling hypothesis highlights that dividend changes transmit information about management’s confidence in future performance. Practical constraints—legal rules, liquidity, and loan covenants—often limit payout choices. For exam questions, you must assess both theory and the effects of these real-world influences.

Key Point Checklist

This article has covered the following key knowledge points:

- The clientele effect and its influence on shareholder composition

- The signaling hypothesis and the impact of dividend changes on investor perceptions

- Legal, liquidity, and contractual constraints affecting dividend policy

- Practical implications for how dividend decisions shape share price and shareholder value

- Alternative dividend forms, such as scrip and share buybacks

Key Terms and Concepts

- dividend policy

- clientele effect

- signaling hypothesis

- information asymmetry