Learning Outcomes

After studying this article, you will be able to explain dividend theories—including the residual policy and life-cycle view—and apply these to real business scenarios. You will distinguish between theoretical and practical influences on dividend decisions and assess how dividend choices affect shareholder wealth and the financing of investment projects.

ACCA Financial Management (FM) Syllabus

For ACCA Financial Management (FM), you are required to understand how dividend policy fits within financial strategy. In particular, this article addresses:

- The theoretical approaches to, and the practical influences on, the dividend decision

- The concept and application of the residual dividend policy

- The life-cycle theory of dividends and its implications

- The relationship between dividend decisions, shareholder wealth, and retained earnings

- How dividend policies interact with investment and financing decisions

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main idea behind the residual dividend policy?

- How does the life-cycle theory explain differences in dividend payout across firms?

- True or false? Under the residual policy, dividends are paid only after funding all positive NPV projects.

- Why might a mature firm pay higher dividends compared to a new growing firm?

- What impact can a change in dividend policy have on shareholder expectations?

Introduction

Dividend policy concerns how much profit a company distributes as dividends versus how much it retains for reinvestment. Two key theoretical approaches for the ACCA FM exam are the residual dividend policy and the life-cycle theory of dividends. Understanding these helps explain real-world dividend behaviour and its link to business strategy, shareholder wealth, and funding decisions.

Key Term: dividend policy

The set of rules or guidelines a company uses to decide the portion of earnings distributed to shareholders versus retained in the business. Key Term: residual dividend policy

An approach where dividends are paid out of earnings only after all acceptable investment opportunities (usually positive NPV projects) have been funded. Key Term: life-cycle theory (of dividends)

A theory proposing that a company's dividend payout is linked to its stage of development—high-growth firms retain profits, while mature firms pay more in dividends.

Dividend Policy in Theory

Dividend policy decisions are significant because they affect the wealth of shareholders and the overall financial strategy of the company. Two theoretical approaches are especially relevant for exam purposes.

Residual Dividend Policy

The residual approach argues that the main purpose of the firm is to maximize shareholder wealth by investing in all positive net present value (NPV) projects. Only after funding these investments does the company consider paying dividends. If profits exceed the funding needed for investment, the surplus is available for dividends. If the required investment uses up all profits, there may be no dividend.

This policy assumes shareholders are indifferent to receiving returns through dividends or capital gains, provided their wealth is maximized. In theory, this approach minimizes the need for raising new external equity and thus reduces issue costs.

Key Term: net present value (NPV)

The difference between the present value of a project's cash inflows and the initial investment cost, used to assess project viability.

Worked Example 1.1

Question: A company has earnings of $10 million available this year. It has investment opportunities requiring $7 million that all yield positive NPVs. What dividend will be paid under the residual policy?

Answer:

The company will retain $7 million to fund the projects. The remaining $3 million ($10m - $7m) is paid out as dividends.

Advantages and Limitations of Residual Policy

- Advantages: Ensures all valuable investment opportunities are funded first; reduces the need for costly external finance.

- Limitations: Leads to unpredictable and potentially fluctuating dividends, which may not align with shareholder preferences for stable income.

Exam Warning: If asked about the residual theory in the exam, do not suggest that it means dividends are never paid—rather, they are paid only from profits not needed for investment.

Dividend Policy and the Corporate Life-Cycle

While the residual approach assumes all firms apply the same reasoning, in practice, dividend policy often follows a pattern based on the company's stage of development—a concept known as the life-cycle theory.

Corporate life-cycle theory links growth firms with earnings retention, mature firms with stable dividends, and declining firms with returning excess cash.

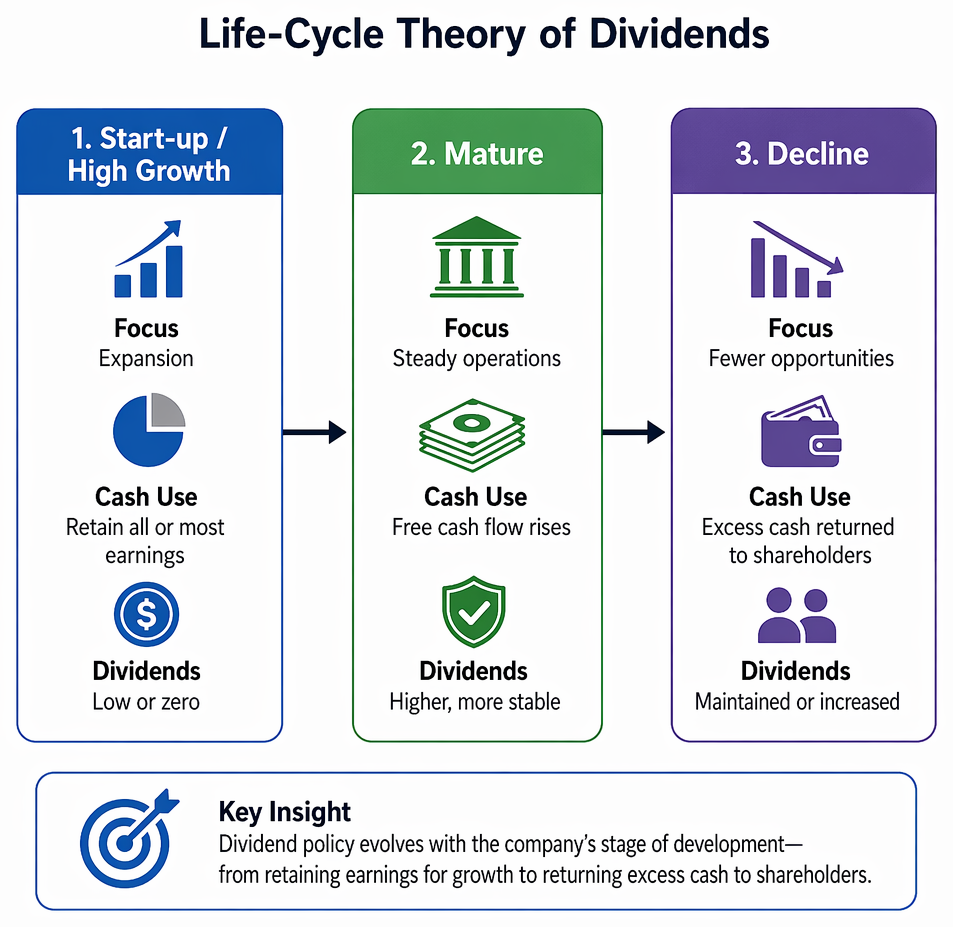

Life-Cycle Theory of Dividends

The life-cycle theory suggests that a firm's dividend policy evolves as it matures:

- Start-up/High Growth: Firms retain all or most earnings to fund expansion. Dividends are low or zero.

- Mature: Fewer new investments mean free cash flow rises. Firms can afford higher, more stable dividends.

- Decline: With fewer profitable opportunities, earnings may shrink, but payouts may be maintained or even increased to return excess cash to shareholders.

This model explains why new technology companies often pay no or low dividends, while established utilities or manufacturers pay high dividends.

Worked Example 1.2

Which type of company is most likely to have a high dividend payout ratio: a new software start-up or a large, established food retailer? Explain why.

Answer:

The food retailer is more likely to pay higher dividends. As a mature firm, it has stable earnings and fewer high-return investment opportunities, so excess profits are returned to shareholders. The start-up retains profits to finance growth.

Practical Considerations in Dividend Policy

Although theories provide a guide, several real-world factors influence the actual dividend paid:

- Shareholder expectations for regular income

- The impact of dividend policy on share price and investor confidence (e.g., dividend cuts may signal financial trouble)

- Tax considerations; some shareholders may prefer dividends over capital gains, or vice versa

- Legal and liquidity constraints restricting dividend payments

Companies tend to favour steady dividends to avoid creating uncertainty for investors, even if profits and investment needs fluctuate.

Revision Tip: Remember: In exam scenarios, connect dividend policy to the firm's growth phase and cash needs as well as shareholder preferences.

Summary

- The residual dividend policy prioritises investment: dividends are only paid from surplus earnings after funding all positive NPV projects.

- The life-cycle theory explains why young, rapidly expanding firms retain earnings, while more mature firms pay higher dividends.

- Real-world dividend policy balances theoretical logic with practical needs for stability, shareholder expectations, and legal limits.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and explain dividend policy, residual policy, and life-cycle theory

- Describe how residual policy links investment and dividends

- Distinguish company life-cycle stages and their typical dividend practices

- Recognise real-world influences on dividend decisions beyond theory

- Apply these theories to exam-style problems and business scenarios

Key Terms and Concepts

- dividend policy

- residual dividend policy

- life-cycle theory (of dividends)

- net present value (NPV)