Learning Outcomes

After reading this article, you will be able to explain and apply the main equity valuation models required for ACCA FM. You will understand the dividend discount model, the Gordon growth model, how to calculate share values using expected dividends and growth, and appreciate the key assumptions, advantages, and limitations of these models.

ACCA Financial Management (FM) Syllabus

For ACCA Financial Management (FM), you are required to understand the valuation of equity investments using dividend-based models. You should focus your revision on:

- The dividend discount model (DDM) and its application to share valuation

- The Gordon growth model as a version of DDM with constant growth

- Calculating the value of shares using expected dividends and growth rates

- The fundamental assumptions and limitations of these models

- How to estimate dividend growth rates from historic data and retained earnings

- The relevance of these models for minority and majority shareholders in both quoted and unquoted companies

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Under what core assumption does the Gordon growth model become invalid for valuing equity?

- A company has just paid a dividend of 16c. Dividends are expected to grow by 4% annually, and the current share price is $2.00. What is the cost of equity, according to the DDM?

- What information is needed to value a share using the dividend discount model?

- True or false? The dividend discount model can be used for shares with no expected future dividend growth.

Introduction

Equity valuation is central to both investment appraisal and financial reporting. For ACCA FM, you need to be able to value company shares using established theoretical models. The primary approach is the dividend discount model (DDM), with the Gordon growth model being its most frequently applied form. These models estimate the value of an ordinary share by discounting expected future dividends at the shareholder's required rate of return.

Key Term: dividend discount model (DDM)

A method for valuing shares by estimating the present value of all expected future dividends discounted at the required rate of return.

The focus of these models is the relationship between dividend payments and share value, reflecting the principle that shareholders invest for returns through dividends or capital gains. Accurate application of these models in the exam depends on recognising their assumptions and using the correct formulas for both constant and growing dividends.

THE DIVIDEND DISCOUNT MODEL

The dividend discount model (DDM) applies the concept that the value of a share is the present value of all future dividends expected by the investor.

General Formula:

where current share price dividend expected at time required rate of return (cost of equity)

In practice, future dividends must often be forecasted using a perpetual pattern (for example, with no growth or constant annual growth).

Shares with Constant Dividends

If dividends are expected to be constant in perpetuity, the formula simplifies to:

where is the constant dividend per period.

Key Term: required rate of return (cost of equity)

The minimum return that investors expect for providing capital to a company, reflecting the risk of that investment.

Shares with Constant Growth (Gordon Growth Model)

The Gordon growth model is the standard approach where dividends are assumed to grow at a constant rate forever.

Gordon Growth Formula:

or

where dividend just paid expected constant growth rate in dividends dividend expected next period

Key Term: Gordon growth model

A version of the dividend discount model assuming dividends grow at a constant rate forever; used especially for mature, stable companies. Key Term: ex-div share price

The share price excluding the value of the next dividend about to be paid; used when applying valuation models like the DDM.

Worked Example 1.1

A company has just paid a dividend of 12c per share. Dividends are expected to grow at 5% per year. The current ex-div share price is $1.50. What is the cost of equity?

Answer:

Use the Gordon growth model, rearranged for :

Hence, .

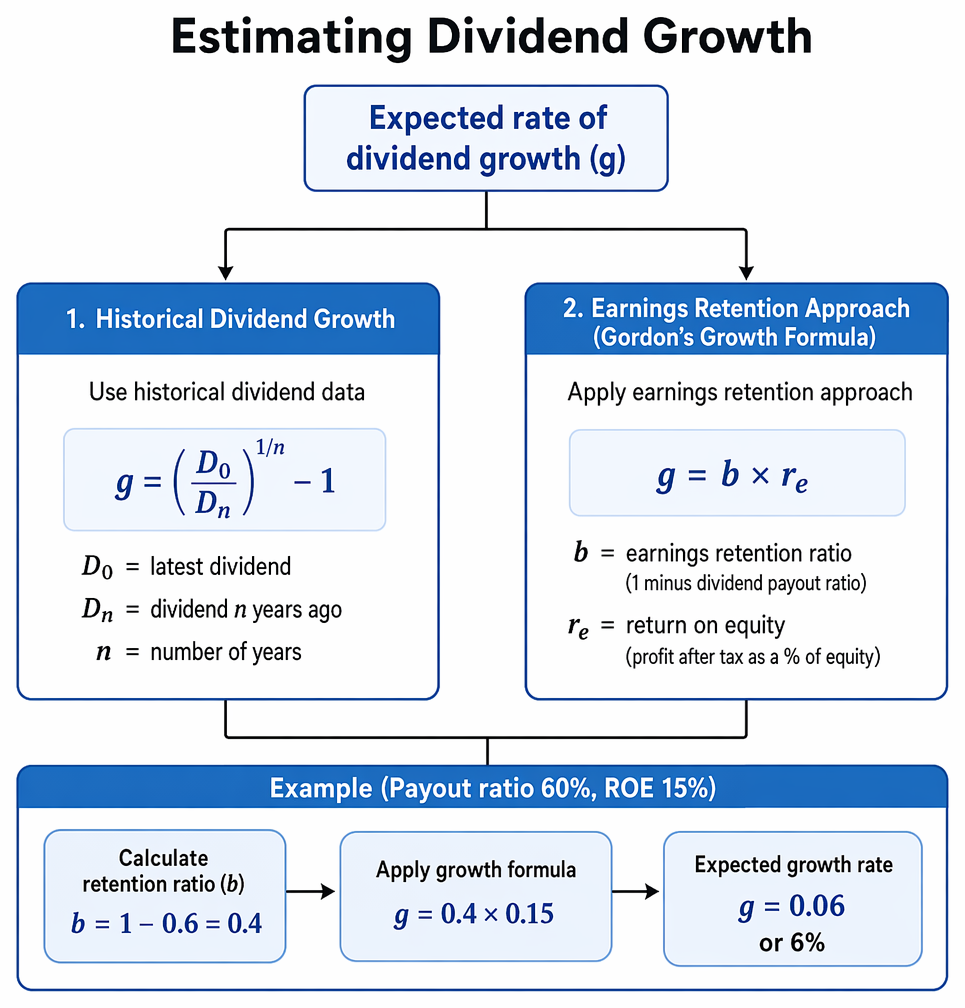

ESTIMATING DIVIDEND GROWTH

To apply the Gordon growth model, you must determine the expected rate of growth in dividends.

Share valuation model choice depends on whether dividends are predictable, whether growth is constant, and whether growth remains below required return.

1. Historical Dividend Growth

If historic dividend data is available, use the following formula:

where is the latest dividend, is the dividend years ago.

2. Earnings Retention Approach (Gordon’s Growth Formula)

Alternatively, estimate growth by applying:

where is the earnings retention ratio and is the return on equity.

Key Term: earnings retention ratio

The proportion of earnings retained in the business instead of paid out as dividends; equals 1 minus the dividend payout ratio. Key Term: return on equity

The profit after tax as a percentage of total shareholders’ equity.

Worked Example 1.2

A company has a payout ratio of 60%, an ROE of 15%. Estimate the expected rate of dividend growth.

Answer:

The retention ratio or 6%.

ASSUMPTIONS, ADVANTAGES, AND LIMITATIONS

Assumptions

- Dividends are the key source of value for shareholders.

- The required return and growth rate are constant and known.

- For the Gordon growth model, ; otherwise, the model is invalid.

Advantages

- Simple calculation from share price and dividend data.

- Provides an objective value based on cash flows.

Limitations

- Sensitive to small changes in or .

- Assumes a stable and predictable dividend policy.

- Not suitable for firms that do not pay regular dividends or where dividends are irregular.

- Applying the model to high-growth companies may overstate share value.

Worked Example 1.3

A technology firm is expected to pay a dividend of 2c next year, growing unpredictably. The company currently reinvests most profits and dividends are irregular. Is the Gordon growth model appropriate?

Answer:

No. The model assumes stable, constant dividend growth, which is not present. An alternative valuation method should be considered for this scenario.Exam Warning: Do not apply the growth model if the estimated growth rate exceeds or equals the required rate of return. The formula will not produce a valid result, and this error can result in lost marks.

Revision Tip: When using these models, always check whether the share price given is ex-div or cum-div. Subtract the forthcoming dividend from a cum-div price before using it in the formula.

Summary

Dividend-based valuation models allow you to estimate a company's share price using projected dividends and growth. The Gordon growth model is widely examined and assumes a constant rate of dividend growth. Be clear about its inputs, method, and where it should (and should not) be applied.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish between the dividend discount model and the Gordon growth model

- Calculate share values given dividend, growth, and required return

- Estimate dividend growth rates using historic data and retention model

- Recognise core assumptions, strengths, and limitations of each model

- Understand when each model is suitable for ACCA FM exam questions

Key Terms and Concepts

- dividend discount model (DDM)

- required rate of return (cost of equity)

- Gordon growth model

- ex-div share price

- earnings retention ratio

- return on equity