Learning Outcomes

After reading this article, you will be able to explain what interest rate swaps are and why organisations use them. You will understand how swaps work, distinguish them from other derivatives like futures or options, and identify their main benefits and risks. You will also be able to describe core exam-relevant scenarios when a swap can be used to manage interest rate exposure in line with ACCA Financial Management (FM) exam requirements.

ACCA Financial Management (FM) Syllabus

For ACCA Financial Management (FM), you are required to understand the risk management techniques available for interest rate risk. In particular, ensure your revision covers:

- The causes and types of interest rate risk faced by organisations

- The available methods for managing interest rate risk, including asset and liability management, matching, smoothing, and forward rate agreements (FRAs)

- The main types of interest rate derivatives (including swaps) used to hedge interest rate risk, and how they are applied in practice

- The advantages, disadvantages, and limitations of swaps compared to other risk management tools

- The difference between fixed interest rate and floating interest rate exposures and how swaps can alter these

- The distinction between swaps and other derivatives such as futures and options

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main reason why a company would enter into an interest rate swap?

- Which exposures can an interest rate swap directly hedge?

- a) Credit risk

- b) Interest rate risk

- c) Liquidity risk

- d) Exchange rate risk

- Outline one key difference between an interest rate swap and a forward rate agreement (FRA).

- A company has floating-rate debt but expects rising interest rates. Would it usually pay fixed or floating in a swap to hedge its risk?

- True or false? In a plain vanilla interest rate swap, principal amounts are exchanged at the start and end dates.

Introduction

Interest rate changes can create significant costs for organisations with debt or investment positions. If rates rise, the cost of floating-rate loans increases; if rates fall, floating-rate assets yield less. Managing this risk is essential for effective financial management and is a clear focus in the ACCA FM syllabus.

One tool for managing this risk is the interest rate swap. Swaps are derivative contracts that allow two parties to exchange interest payments (typically fixed for floating) based on a notional amount, helping to align a company’s interest rate profile with its risk appetite.

Key Term: interest rate swap

A contractual agreement in which two parties exchange a series of interest payments on a specified notional amount, with one party usually paying a fixed rate and the other a floating rate over the same period.

The Purpose and Mechanics of Interest Rate Swaps

Interest rate swaps are primarily used to manage exposure to interest rate movements. They allow an entity to convert its floating-rate borrowing to a fixed rate or vice versa, without altering the original terms or counterparties of the existing loan.

In a standard (plain vanilla) interest rate swap:

- One party agrees to pay a fixed interest rate to the counterparty,

- The other party pays a floating rate (often linked to a benchmark such as LIBOR or SONIA),

- Both sets of payments are calculated on an agreed notional principal, which is not exchanged.

Key Term: notional principal

The hypothetical amount used to calculate interest payments in a swap. The notional is not actually transferred between swap parties. Key Term: plain vanilla swap

The most basic form of interest rate swap, involving the periodic exchange of fixed-rate payments for floating-rate payments between two parties.

Why Use a Swap? Suppose a company has borrowed at a floating interest rate but believes that rates are about to rise, increasing future interest payments. By entering into a swap to pay fixed and receive floating, it can effectively lock in interest costs, achieving certainty.

Conversely, a company with fixed-rate debt may anticipate falling rates. By swapping to receive fixed and pay floating, it can benefit if future floating rates fall below its current fixed rate.

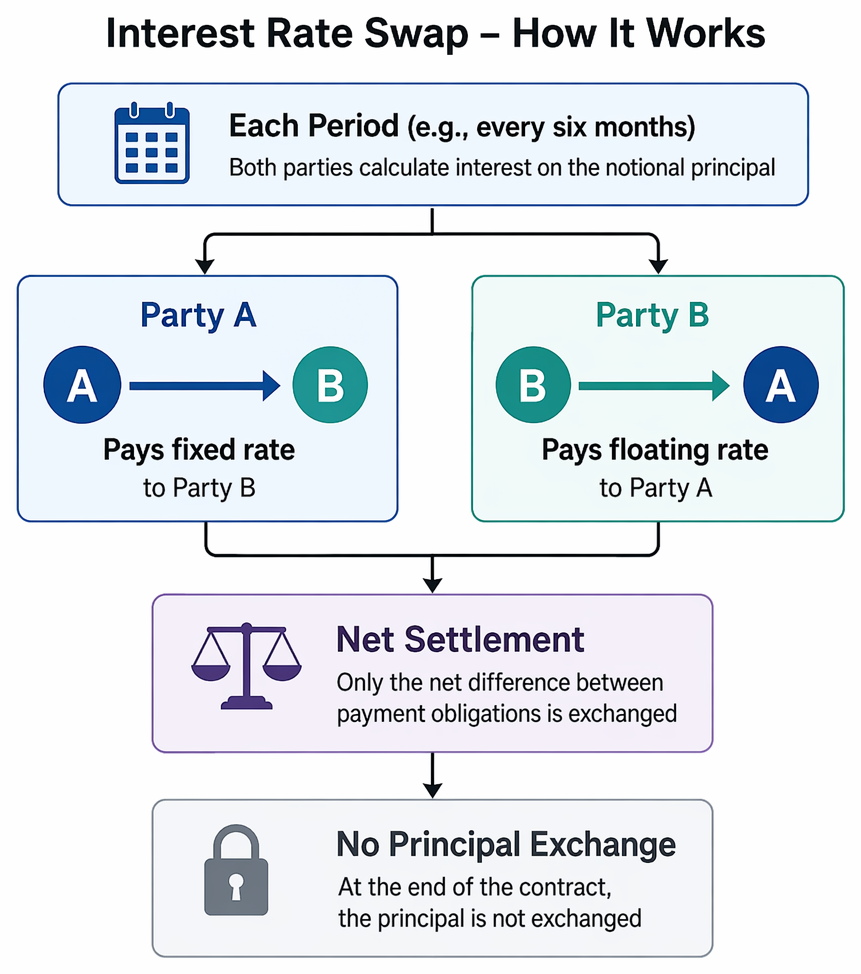

How Interest Rate Swaps Work

The swap itself is a separate contract from any existing loans. It does not affect the original loan agreement or change the lending party. Instead, it changes the effective rate paid or received by each participant.

Floating-rate debt with rising-rate expectations implies pay-fixed/receive-floating, while fixed-rate debt with falling-rate expectations implies receive-fixed/pay-floating.

-

Each period (e.g., every six months), both parties calculate interest due on the notional principal:

- Party A pays Party B at the agreed fixed rate,

- Party B pays Party A at the agreed floating rate,

- Only the net payment is usually exchanged.

-

At the end of the contract, the principal is not exchanged.

Key Term: net settlement

The process in a swap whereby only the difference between parties’ payment obligations is exchanged each period, rather than both gross amounts.

When Are Swaps Used?

Common scenarios:

- To convert floating-rate debt to a fixed-rate (or vice versa) to match an organisation’s interest rate view or risk policy.

- To access more favourable rates. For instance, a company with a strong fixed-rate borrowing profile swaps with another who has better access to floating-rate funding.

- To hedge anticipated or existing exposures without restructuring existing borrowings or investments.

Comparison to Other Risk Management Techniques

Interest rate swaps differ from other derivatives and traditional hedging methods:

| Feature | Interest Rate Swap | FRA/Futures | Options |

|---|---|---|---|

| Exchange of rates | Yes, over time | No; lock a single rate | Right, not obligation, to fix |

| Used for | Ongoing exposure | Single-period exposure | Protecting against adverse movements only |

| Principal exchanged | No | No | No |

| Upfront cost | Typically none | None | Premium payable |

Swaps are best for sustained interest rate risk, while FRAs or futures may be more suitable for short-term or one-off exposures. Options protect against adverse movements but let you benefit from favourable ones—at a cost.

Worked Example 1.1

A borrower has a $10 million loan paying 3-month LIBOR plus 1%. The company wishes to lock in a fixed rate for the next 2 years, but current loan terms cannot be altered. The treasurer arranges a 2-year interest rate swap to pay 4.5% fixed and receive 3-month LIBOR on $10 million, matching the reset dates with the loan.

Question: What is the effective interest rate paid after entering the swap, assuming LIBOR fluctuates over the period?

Answer:

The borrower continues to pay bank interest = LIBOR + 1%. Through the swap, the borrower pays a fixed 4.5% and receives LIBOR, netting off. Overall, LIBOR cancels out: (LIBOR + 1%) (to bank) + 4.5% (to swap) – LIBOR (received via swap) = 4.5% + 1% = 5.5% total effective fixed rate over 2 years.

Worked Example 1.2

A company expects interest rates to decline and wants to benefit from floating rates but has an existing fixed-rate debt. What swap arrangement can it use, and what exposure does it then face?

Answer:

The company should enter into a swap to receive fixed and pay floating, matching amounts and periods to its existing loan. This changes its effective position to paying floating rates (fixed loan + swap net payments), allowing it to benefit if rates fall. However, if rates rise, the company may end up paying more than with its original fixed-rate only.Exam Warning: Interest rate swaps do not change the original debt principal, and the notional amount is never exchanged. In ACCA FM questions, avoid stating that principal is swapped or repaid with a swap. Also, be cautious: swaps hedge ongoing exposures, not one-off interest payments.

Revision Tip: In the exam, you may be asked to recommend a hedge for a particular scenario. You should be able to state when a swap is appropriate compared to other tools such as FRAs or futures.

Summary

Interest rate swaps allow companies to effectively convert floating-rate debt to a fixed rate, or vice versa, by exchanging interest payments with another party. Swaps are most appropriate for managing sustained exposure where rates are expected to move adversely, providing flexibility without altering the existing debt arrangements. The notional principal is never exchanged, and swaps hedge interest rate risk, not other types of risk such as credit or foreign exchange.

Key Point Checklist

This article has covered the following key knowledge points:

- Define an interest rate swap and explain its structure (fixed vs floating payments)

- Describe the key reasons organisations use swaps to manage interest rate risk

- Understand the mechanics of swaps, including payment netting and notional principal

- Contrast swaps with other risk management tools (FRAs, futures, options)

- Identify practical scenarios suitable for swaps and understand typical exam pitfalls

Key Terms and Concepts

- interest rate swap

- notional principal

- plain vanilla swap

- net settlement