Learning Outcomes

After reading this article, you will be able to explain when borrowing costs must be capitalised under IAS 23, identify which assets qualify for capitalisation, describe the criteria that trigger the start and cessation of capitalisation, and calculate the amount of borrowing costs to include in the cost of an asset. You will also distinguish between direct and general borrowings for eligible assets—key for your ACCA FR exam.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand how borrowing costs are treated under IAS 23. In particular, your revision should address:

- When and how borrowing costs must be capitalised as part of the cost of an asset

- The definition and identification of qualifying assets

- The criteria for commencement and cessation of capitalisation

- Calculation of borrowing costs to be capitalised, including treatment of general and specific borrowings

- Recognising when borrowing costs should be expensed

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following assets typically qualifies for the capitalisation of borrowing costs under IAS 23?

- a) Inventory that is produced routinely within a month

- b) An office building under construction for the company's own use

- c) Trade receivables

- d) A delivery vehicle purchased outright

-

What are the three conditions required for the commencement of capitalisation of borrowing costs?

-

When an entity uses general borrowings for a qualifying asset, how is the amount of borrowing cost to be capitalised determined?

-

True or false? Borrowing costs continue to be capitalised during periods when construction of the asset is intentionally suspended.

Introduction

Borrowing costs are common for companies financing the construction or acquisition of substantial assets. The treatment of these costs in financial statements is regulated under IAS 23 Borrowing Costs. A correct approach is essential for both accurate reporting and ACCA FR exam success.

IAS 23 sets out when borrowing costs must be added to the cost of certain assets—so-called qualifying assets—and when such costs must be expensed instead. This article guides you through the capitalisation criteria, the types of eligible assets, relevant timing rules, and calculation methods.

Key Term: borrowing costs

Interest and other costs incurred by an entity in connection with the borrowing of funds. This includes interest expense calculated using the effective interest method and certain exchange differences arising from foreign currency borrowings. Key Term: qualifying asset

An asset that necessarily takes a substantial period of time to get ready for its intended use or sale.Test Tip: When revising Capitalisation criteria and eligible assets, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Capitalisation of Borrowing Costs

Overview

IAS 23 requires that borrowing costs directly attributable to the acquisition, construction, or production of a qualifying asset be capitalised as part of the asset's cost. Other borrowing costs must be recognised as an expense in the period incurred.

Criteria for Capitalisation

Borrowing costs are capitalised only when all of the following conditions are met:

- Expenditure for the asset is being incurred

- Borrowing costs are being incurred

- Activities necessary to prepare the asset for its intended use or sale are in progress

When any one of these conditions is not met, capitalisation is suspended or not permitted.

Key Term: capitalisation

The process of adding costs to the cost of an asset rather than expensing them immediately.

Qualifying Assets

Not all assets are eligible for borrowing cost capitalisation. Qualifying assets include assets that take a substantial period (normally >12 months) to get ready for intended use or sale. Examples:

- Self-constructed property, plant, and equipment

- Investment properties under construction

- Inventories produced over a long period (e.g. wine aging or large items manufactured to order)

Non-qualifying assets include assets that are ready for use or sale when acquired, or inventories manufactured or produced routinely over a short period.

Commencement and Cessation of Capitalisation

Start of Capitalisation

Begin capitalising borrowing costs when:

- Expenditure is being incurred on the asset

- Borrowing costs are being incurred

- Activities to prepare the asset for its intended use or sale have commenced

All three conditions must be satisfied.

Suspension of Capitalisation

If development of the asset is suspended for extended periods (other than brief, necessary delays), capitalisation of borrowing costs must be suspended during that period.

Cessation of Capitalisation

Stop capitalising borrowing costs when substantially all activities necessary to prepare the asset for use or sale are complete. Any additional borrowing costs incurred after this point are expensed.

Calculation of Borrowing Costs to Capitalise

Specific Borrowings

If funds are borrowed specifically for the acquisition, construction, or production of a qualifying asset:

- Capitalise borrowing costs actually incurred on that loan during the period, less any investment income on temporary investment of those borrowings.

General Borrowings

If a qualifying asset is financed from general borrowings:

- Calculate a capitalisation rate (weighted average rate of general borrowings)

- Capitalise an amount equal to the capitalisation rate multiplied by the asset's expenditure during the period.

Key Term: capitalisation rate

The weighted average interest rate applicable to the entity’s general borrowings during the period.

Treatment of Interest Income on Unused Funds

Any investment income earned from temporarily investing funds borrowed specifically for the asset is deducted from the borrowing costs eligible for capitalisation.

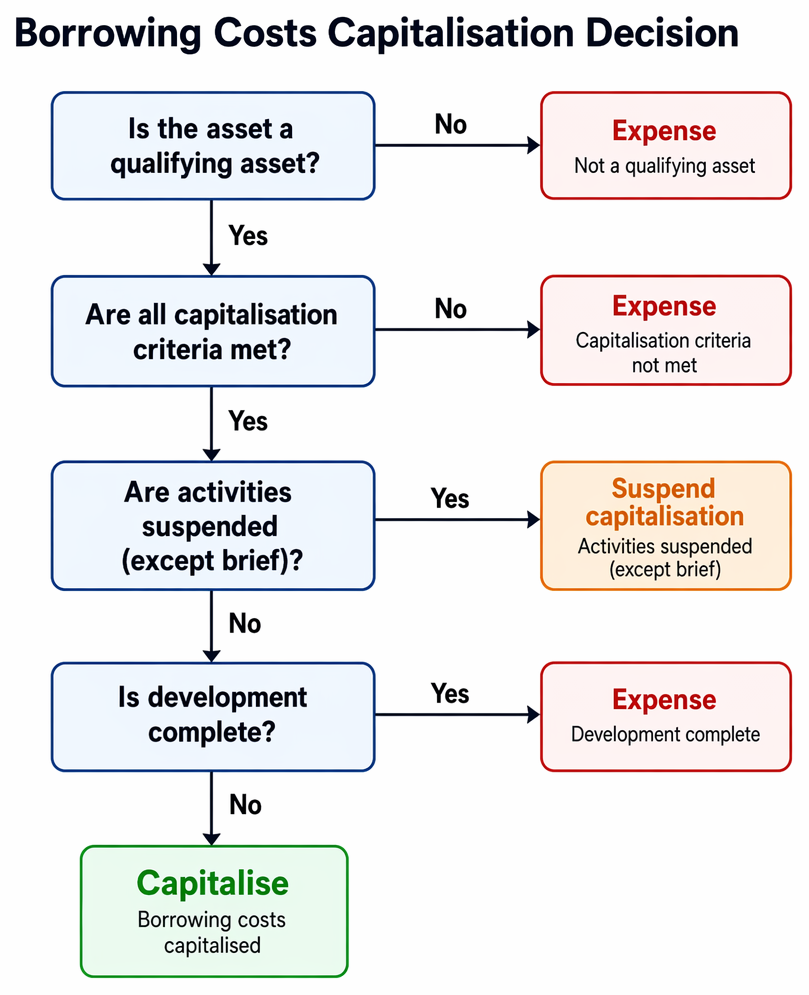

Summary Table: Borrowing Costs Capitalisation Decision

Commencement of capitalisation requires a qualifying asset and concurrent expenditure, incurred borrowing costs, and activities necessary for intended use or sale.

| Condition | Answer |

|---|---|

| Is the asset a qualifying asset? | Capitalise |

| Not a qualifying asset? | Expense |

| Are all capitalisation criteria met? | Capitalise |

| Activities suspended (except brief)? | Suspend capitalisation |

| Development complete? | Expense |

Worked Example 1.1

A company begins building a factory on 1 February 20X9. It obtains a specific loan of $10 million at 5% interest on 1 January 20X9. Construction expenditure occurs evenly from 1 February to 31 August, and the project is completed on 31 August 20X9. From 1 January to 31 January, the $10 million was temporarily invested to earn $4,000 interest.

How much borrowing cost should be capitalised?

Answer:

Borrowing costs should be capitalised from 1 February to 31 August only (the construction period). Annual interest: $10m × 5% = $500,000. For 7 months: $500,000 × 7/12 = $291,667. Less investment income: $4,000 (as earned on borrowed funds in January). Total capitalised: $291,667 – $4,000 = $287,667.

Worked Example 1.2

An entity takes out the following general borrowings throughout the year: $8m at 7% and $12m at 10%. It spends $5m on a self-constructed asset steadily throughout the year.

What borrowing cost is capitalised?

Answer:

Total interest: ($8m × 7%) + ($12m × 10%) = $560,000 + $1,200,000 = $1,760,000. Total borrowings: $20m. Capitalisation rate: $1,760,000 / $20,000,000 = 8.8%. Interest capitalised: $5m × 8.8% = $440,000 (assuming even expenditure; otherwise, apply a time-weighted approach).Exam Warning: In exams, many students forget to deduct investment income earned on surplus funds from the amount capitalised, or they continue capitalising after asset completion. Marks will be lost if you fail to apply these timing and calculation rules accurately.

Summary

The core principle of IAS 23 is to capitalise borrowing costs that are directly attributable to a qualifying asset—but only while preparatory activities are underway. Know how to identify qualifying assets, apply timing rules, and calculate capitalisation amounts for both specific and general borrowings. All other borrowing costs must be expensed.

Key Point Checklist

This article has covered the following key knowledge points:

- Define ‘borrowing costs’ and ‘qualifying asset’ for IAS 23 purposes

- Identify assets that require capitalisation of borrowing costs

- Explain when to commence, suspend, and cease capitalisation

- Calculate borrowing costs to capitalise for both specific and general borrowings

- Deduct investment income on unused borrowed funds for specific borrowings

- Recognise that all other borrowing costs are expensed

Key Terms and Concepts

- borrowing costs

- qualifying asset

- capitalisation

- capitalisation rate