Learning Outcomes

After reading this article, you will be able to explain the purpose and content of IFRS 13 Fair Value Measurement disclosure requirements. You will be able to identify the key disclosure items in financial statements for fair value measurements, apply the three-level fair value hierarchy, and describe what information must be disclosed for recurring and non-recurring fair value measurements.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the disclosure requirements of IFRS 13 and how fair value measurements are presented in published accounts. This article will help you revise:

- The required fair value measurement disclosures under IFRS 13

- The structure and explanation of the fair value hierarchy (Levels 1–3)

- Disclosures for recurring and non-recurring fair value measurements

- Disclosure of valuation techniques and significant inputs

- Presentation in the notes to the financial statements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is NOT a required disclosure for assets measured at fair value under IFRS 13?

- a) The level of the fair value hierarchy

- b) The fair value at the reporting date

- c) The cost of acquiring the asset

- d) The valuation techniques used

-

Define what is meant by a ‘Level 2’ input in the context of the fair value hierarchy.

-

True or false? A description of the significant unobservable inputs used in a Level 3 valuation must be disclosed.

-

What additional disclosures are required for recurring fair value measurements using significant unobservable (Level 3) inputs?

Introduction

When financial statements include items measured at fair value, transparency and understanding of those measurements are essential for users. IFRS 13 Fair Value Measurement requires not only that fair value is measured correctly, but also that clear disclosures explain how those figures were determined. These disclosures ensure comparability and help users assess the reliability of fair value measurements, especially where estimates or subjectivity are involved.

Key Term: fair value measurement

The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.Test Tip: When revising Disclosure requirements, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Fair Value Hierarchy and Disclosure

IFRS 13 categorises inputs to valuation techniques into three levels, forming the fair value hierarchy:

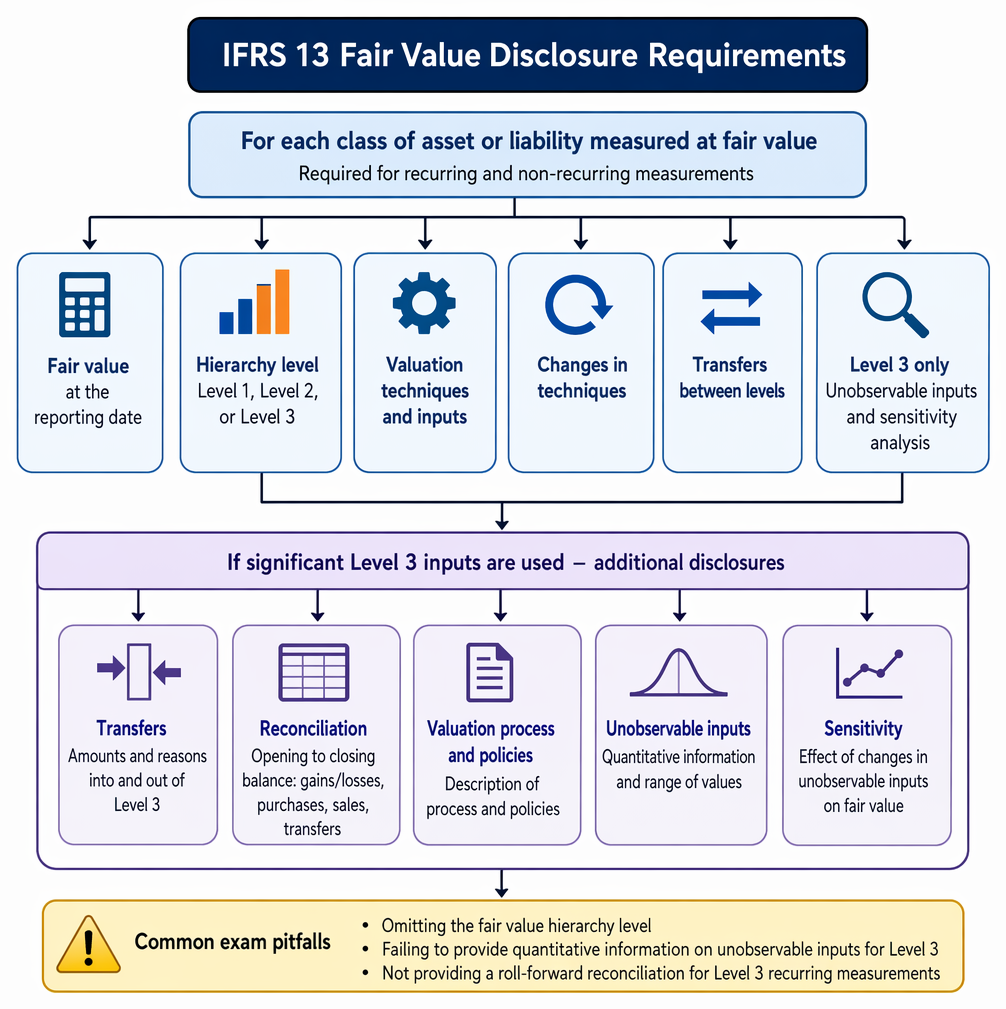

IFRS 13 disclosure requirements extend from fair value and hierarchy level to valuation inputs, transfers, and Level 3 reconciliation disclosures.

- Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities

- Level 2: Observable inputs other than quoted prices in Level 1 (e.g. quoted prices for similar items)

- Level 3: Unobservable inputs based on the entity’s own assumptions

Key Term: fair value hierarchy

A classification of inputs to valuation techniques into three levels, with Level 1 being the most reliable and Level 3 the least. Key Term: recurring vs non-recurring fair value measurement

Recurring measurements arise when an item is measured at fair value at each reporting date. Non-recurring measurements occur in particular circumstances (e.g. impairment, business combinations).

Required Disclosures

For each class of asset or liability measured at fair value, an entity must disclose:

- The fair value at the reporting date

- The level of the fair value hierarchy (Level 1, 2, or 3)

- For recurring and non-recurring fair value measurements:

- The valuation techniques and inputs used

- Any changes in valuation technique

- If there has been a transfer between levels

- For Level 3 items—information about significant unobservable inputs and sensitivity analysis

Level 3 Additional Requirements

If any fair value measurement uses significant Level 3 inputs, the following must also be disclosed:

- The amount and reasons for transfers into and out of Level 3

- A reconciliation from opening balance to closing balance, showing gains/losses, purchases, sales, and transfers

- Description of the valuation process and policies

- Quantitative information about significant unobservable inputs and their range of values

- Description of the sensitivity of the valuation to changes in unobservable inputs

Worked Example 1.1

Question: Treevie Co measures its investment property at fair value. At 31 December 20X6, the fair value was determined using a valuation model incorporating significant unobservable market data (Level 3). Treevie Co reported a $100,000 increase in fair value in 20X6. How should Treevie Co satisfy IFRS 13’s disclosure for this item?

Answer:

Treevie Co must disclose the fair value at year end, identify that the measurement is Level 3, describe the valuation technique and significant unobservable inputs, provide a reconciliation of the opening and closing balances, disclose the $100,000 gain, and explain how changes in unobservable inputs would affect the fair value.

Disclosures for Assets/ Liabilities Not Measured at Fair Value

Sometimes, fair value information is required for items not measured at fair value (e.g. financial instruments at amortised cost). In these cases, an entity must disclose:

- The fair value of the item

- The fair value hierarchy level

- The valuation techniques used

Exam Warning: Omitting the fair value hierarchy level or failing to provide quantitative information on unobservable inputs for Level 3 items are common errors and will lose marks on the exam. Always disclose the hierarchy level and provide a roll-forward reconciliation for Level 3 recurring measurements.

Summary

IFRS 13 requires extensive disclosures for fair value measurements. Entities must disclose not only the amount and methods used, but also the level of the hierarchy, key inputs, and the reliability of those figures. Level 3 measurements require additional reconciliations and sensitivity analyses to ensure full transparency.

Key Point Checklist

This article has covered the following key knowledge points:

- Describe required fair value disclosures per IFRS 13

- Explain the three-level fair value hierarchy and assign assets/liabilities accordingly

- Identify required disclosure items for recurring and non-recurring fair value measurements

- List additional requirements for Level 3 measurements (reconciliation, sensitivity, policies)

- Recognise the importance of disclosing valuation techniques and significant inputs

Key Terms and Concepts

- fair value measurement

- fair value hierarchy

- recurring vs non-recurring fair value measurement