Learning Outcomes

After studying this article, you will be able to explain how inventories are measured under IAS 2, including when and how to use the FIFO and weighted average cost formulas. You will be able to distinguish between these cost formulas, apply them in inventory valuation scenarios, and ensure compliance with the consistency and disclosure requirements of IAS 2.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the correct measurement and reporting of inventories under IAS 2. Focus your revision on the following areas:

- The definition and scope of inventories under IAS 2

- What costs are included in inventory valuation

- The purposes and application of the FIFO and weighted average (AVCO) cost formulas

- Selection and consistent application of cost formulas for interchangeable goods

- Calculating inventory value at the lower of cost and net realisable value (NRV)

- Disclosure requirements for inventory policies and carrying amounts

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which two cost formulas does IAS 2 permit for inventories that are interchangeable?

- A company buys 400 units at $5, then 200 units at $8. If it sells 500 units, what is the closing inventory value using FIFO? What about using weighted average cost?

- Is an entity allowed to change its inventory cost formula for similar items from FIFO to weighted average in different periods? Explain briefly.

- Define briefly what is meant by “net realisable value” under IAS 2.

Introduction

Inventory measurement directly affects an entity’s reported profits and asset values. Under IAS 2, it is critical to select an appropriate cost formula for inventories—especially when goods are interchangeable. IAS 2 specifies that for such inventories, only the first-in, first-out (FIFO) and weighted average cost formulas are permitted. Understanding how these cost formulas work, their impact on financial statements, and the associated disclosure requirements is essential for ACCA Financial Reporting exam success.

Key Term: inventories

Assets held for sale in the ordinary course of business, in the process of production for such sale, or as materials or supplies to be consumed in production.

Cost of Inventories: What Is Included

Inventory cost includes all costs to bring inventories to their present location and condition, such as:

- Cost of purchase: purchase price, import duties, transport and handling (after deducting trade discounts and rebates)

- Costs of conversion: direct labour, production overheads allocated on a normal capacity basis

- Other costs: only if necessary to bring inventories to present condition

Abnormal waste, storage (not required in production), administrative, and selling costs are excluded from inventory.

Key Term: cost formula

The method used to assign costs to inventories—such as FIFO or weighted average—when items are interchangeable.

Cost Formulas Permitted by IAS 2

When inventories are interchangeable, they cannot be traced to a specific identity. In these cases, IAS 2 permits:

- FIFO (First-in, First-out)

- Weighted Average Cost (AVCO)

Specific identification of cost may be used only for inventory items that are not interchangeable or are for specific projects.

Key Term: FIFO (first-in, first-out)

A cost formula assuming that the earliest (first) goods purchased or produced are sold or used first. Key Term: weighted average cost (AVCO)

A cost formula in which each unit of inventory is valued at the average cost of all similar units available for sale during the period.

FIFO (First-In, First-Out)

Under FIFO, the first goods purchased or manufactured are assumed to be sold first. Thus, ending inventory is valued at the cost of the most recent purchases.

Weighted Average Cost

Under the weighted average formula, inventory is valued at the average cost of all inventory available for sale during the period, recalculated with each purchase (if using a perpetual system) or at period end (if using a periodic system).

Worked Example 1.1

A company has the following purchases and sales during a month:

- 100 units at $6

- 150 units at $8

- Sold 180 units

Calculate closing inventory using (a) FIFO, (b) weighted average cost.

Answer:

(a)FIFO: 100 units at $6 issued first, then 80 units at $8. Closing inventory: 70 units at $8 = $560. (b) Weighted average cost: Total cost = $600 + $1,200 = $1,800. Total units = 250. Average cost per unit = $7.20. Closing inventory: 70 units x $7.20 = $504.Exam Warning: IAS 2 does not permit the use of the LIFO (last-in, first-out) cost formula. Using LIFO will result in zero marks in the ACCA exam.

Consistency and Selection of Cost Formulas

For inventories with similar nature and use, the chosen cost formula must be applied consistently within the entity. It is permitted to use different cost formulas for inventories of a different nature or use (e.g., raw materials vs. finished goods) where justified.

Worked Example 1.2

A retailer buys:

- 500 units at $10

- 300 units at $13

- Sells 600 units during the period

Calculate inventory value at the period end using weighted average.

Answer:

Total units available: 800. Total cost: $5,000 + $3,900 = $8,900. Weighted average cost: $8,900 / 800 = $11.125 per unit. Closing inventory: 200 units x $11.125 = $2,225.Revision Tip: When answering exam questions, label your cost formula clearly (e.g., FIFO or AVCO). Do not mix methods for similar inventory classes. Justify any change of cost formula clearly as required by the standard.

Impact of Cost Formula on Profits and Inventory Values

- When prices are rising, FIFO results in lower cost of goods sold and higher closing inventory than AVCO, therefore higher reported profit.

- When prices fall, the reverse applies—FIFO results in higher cost of goods sold and lower closing inventory.

Changes to a cost formula are permitted only where they result in more relevant and reliable information—a policy must not be changed arbitrarily. If a change occurs, it must be applied retrospectively and prior periods restated for comparability.

Key Term: net realisable value (NRV)

The estimated selling price in the ordinary course of business less the estimated costs of completion and costs necessary to make the sale.

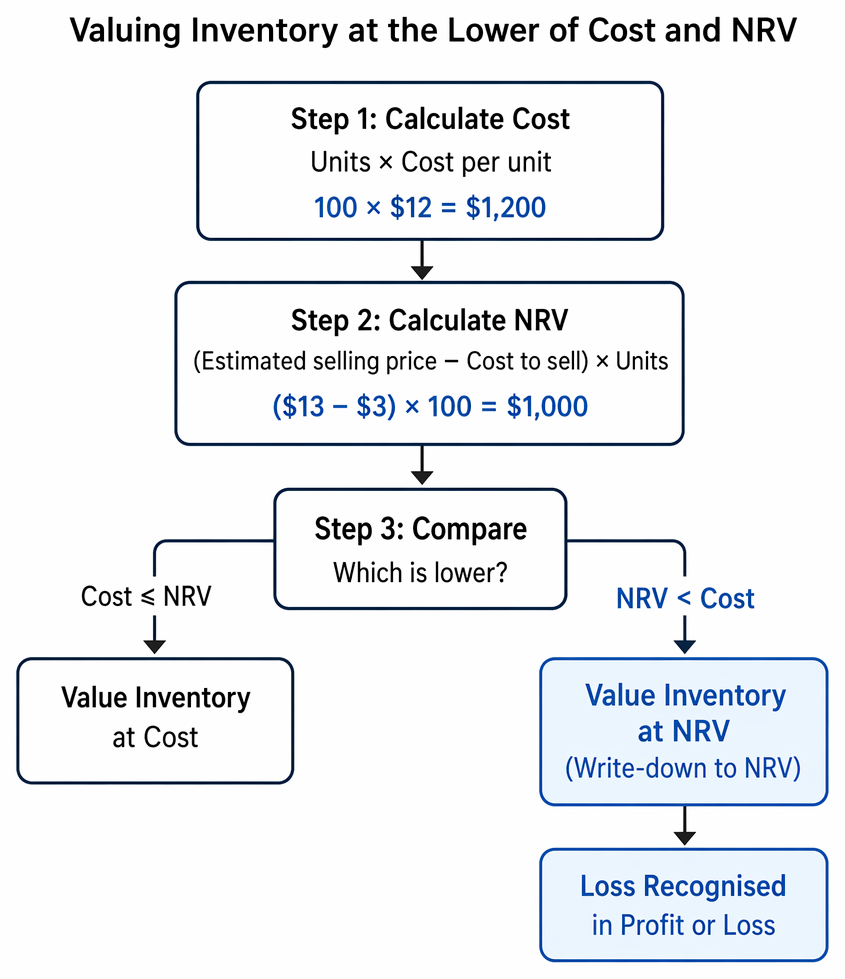

Valuing Inventory at the Lower of Cost and NRV

IAS 2 requires all inventories to be stated at the lower of cost and NRV. If NRV falls below cost, inventory is written down to NRV, with the loss recognised in profit or loss.

Inventory valuation under IAS 2 identifies permissible cost components, defines net realisable value, and records losses when NRV is below cost.### Worked Example 1.3

A company has 100 units of a product costing $12 each. Due to market changes, the estimated selling price is $13 but it will cost $3 per unit to sell.

What value should inventory be stated at?

Answer:

Cost: $1,200. NRV: ($13 - $3) x 100 = $1,000. Value inventory at $1,000 (the lower of cost and NRV).

Disclosure Requirements

IAS 2 requires disclosure in the financial statements of:

- Accounting policy adopted for measuring inventories, including the cost formula used

- Total carrying amount of inventories, appropriately classified

- Carrying amount of inventories carried at fair value less costs to sell, and amount of inventory written down to NRV

This enables users to assess the effect of inventory methods on reported performance.

Exam Warning

Changing from one permitted cost formula to another for similar items requires justification that it results in more relevant/reliable financial information. Arbitrary changes are not allowed.

Summary

IAS 2 mandates that inventories are carried at the lower of cost and net realisable value. For interchangeable inventory, the cost can be determined using FIFO or weighted average, applied consistently to similar items. The chosen method can materially impact reported profit and inventory values, so clarity and consistency are essential.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain what costs are included in inventory valuation per IAS 2

- State when and how FIFO or weighted average (AVCO) cost formulas should be used

- Apply FIFO and AVCO to inventory calculation scenarios

- Recognise the importance of applying a cost formula consistently to similar items

- Outline required IAS 2 inventory disclosures

Key Terms and Concepts

- inventories

- cost formula

- FIFO (first-in, first-out)

- weighted average cost (AVCO)

- net realisable value (NRV)