Learning Outcomes

After reading this article, you will be able to apply IAS 2 rules on inventory net realisable value (NRV), including when and how to adjust inventories below cost. You will understand the procedures for writing down inventories, recognise the conditions under which reversals of write-downs are allowed, and be able to compute and disclose the effects in financial statements.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand how to measure, recognise, and account for inventories in compliance with IAS 2. You should revise the following syllabus areas for this topic:

- Explain and apply the principle that inventories are measured at the lower of cost and net realisable value under IAS 2

- Recognise circumstances that require inventories to be written down below cost and how to calculate the required write-down

- Account for and disclose write-downs of inventories and the reversal of previous write-downs when NRV increases

- Distinguish between inventory cost, NRV, and replacement cost for financial reporting

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the correct measurement basis for inventories under IAS 2?

- a) Cost

- b) Net realisable value

- c) Replacement cost

- d) Lower of cost and net realisable value

-

Which of the following is included in the calculation of net realisable value?

- a) Purchase price of the inventory

- b) Estimated selling price less estimated costs of completion and costs to make the sale

- c) Replacement cost

- d) Inventory carrying value per last year’s financial statements

-

True or false? If a previous write-down of inventory is no longer necessary due to a rise in NRV, IAS 2 allows reversal of the write-down up to the original cost of inventory.

-

Briefly state two circumstances when inventory must be written down below cost.

Introduction

Inventories are a key current asset and must be valued properly under IFRS to present a true and fair view. IAS 2 requires inventory to be measured at the lower of cost and net realisable value. This ensures assets are not overstated in financial statements if inventories cannot be sold for at least cost. Businesses may face events—damage, obsolescence, or market declines—making NRV less than cost. In such cases, inventories must be written down. If circumstances later improve and NRV increases, IAS 2 specifies how and when write-downs may be reversed.

Key Term: net realisable value (NRV)

The estimated selling price in the ordinary course of business, less the estimated costs of completion and the estimated costs necessary to make the sale.

Accounting for Inventories at Lower of Cost and NRV

IAS 2 requires each type of inventory to be measured at the lower of cost and net realisable value at each reporting date.

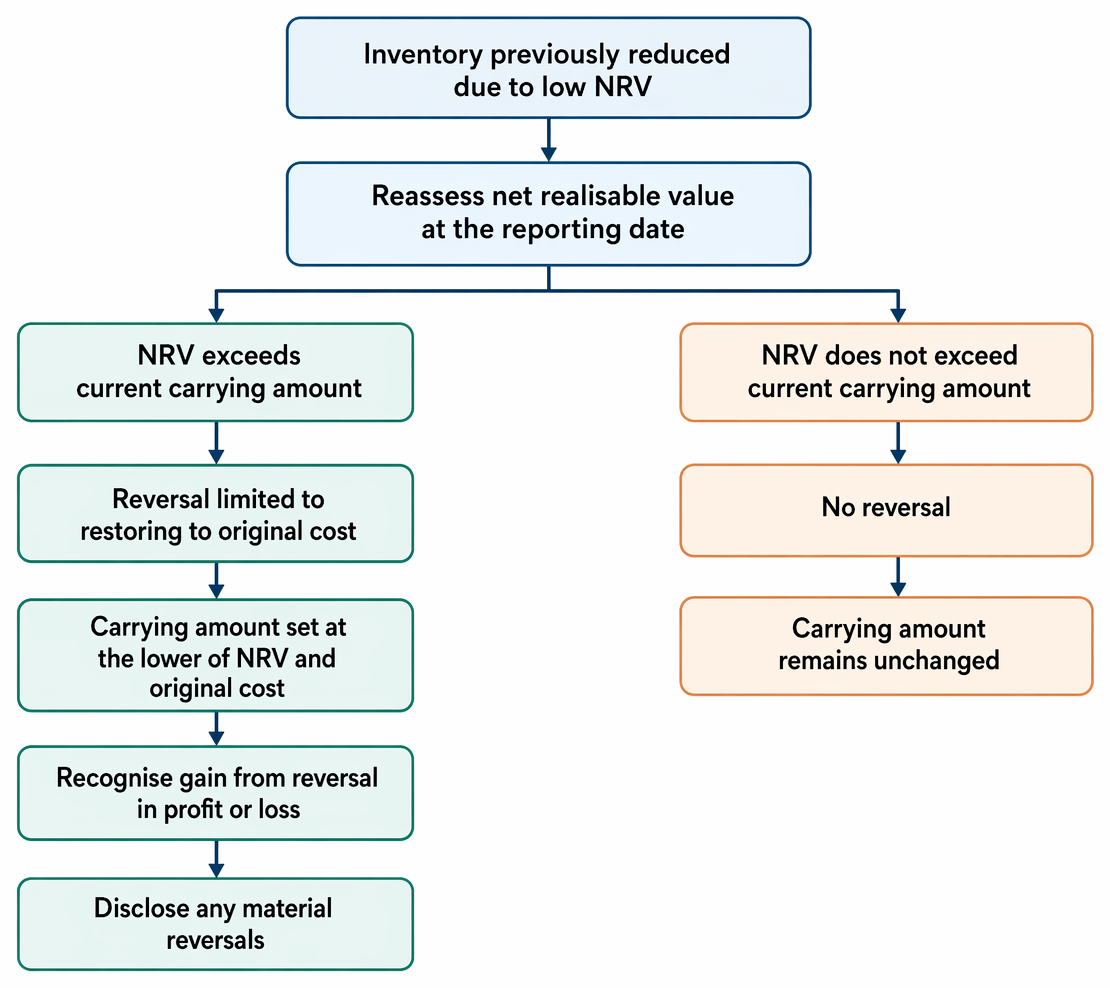

Inventory write-down reversals follow reporting-date NRV reassessment, are capped at original cost, and are credited to profit or loss.

Inventories may need to be written down below cost in cases such as:

- Physical damage or deterioration

- Obsolescence due to technological change

- Declines in selling prices

- Excess supply or low market demand

Key Term: write-down (of inventory)

The reduction in the carrying amount of inventory to its net realisable value when NRV falls below cost.

When to Write Down Inventories

Inventories should be reviewed item by item or, if appropriate, by group or category. Write-downs must be made immediately in profit or loss if NRV is below cost at the reporting date. Replacement cost is not used for this assessment, and write-downs cannot be selective to increase or smooth profits.

Worked Example 1.1

Scenario: Dulcet Ltd has 1,000 units of a product in inventory at a cost of $30 each. The estimated selling price is $32 per unit. Selling costs to complete and deliver each unit are $6. Recent market data shows similar items selling for $34.

- Calculate NRV per unit.

- At what value should the inventory be stated in the statement of financial position?

Answer:

- Estimated NRV per unit = $32 (selling price) − $6 (costs to sell) = $26.

- Inventory must be measured at the lower of cost ($30) and NRV ($26), so value = $26,000.

Recognition and Disclosure of Write-Downs

The amount of any write-down should be recognised as an expense in profit or loss, usually within cost of sales. The carrying amount of inventory should reflect the adjustment. The financial statements should disclose amounts written down to NRV, and material reversals must also be disclosed.

Reversal of Write-Downs to NRV

If circumstances that caused a previous write-down no longer exist, and NRV has increased, IAS 2 allows the reversal of the write-down up to the amount that would have been recognised if the write-down had not occurred. The reversal is credited to profit or loss.

Write-down reversals may be required if:

- Inventory previously written down is now expected to sell at a higher price

- Costs of completion or costs necessary to make the sale decrease

- Market demand recovers

Key Term: reversal of write-down

The process of increasing the carrying amount of inventory when a previous impairment loss is no longer required, but only up to the original cost.

Worked Example 1.2

Scenario: Soraya Co wrote down a product line from cost of $100,000 to NRV of $82,000 in the last period. In the current year, increased demand raises the estimated NRV to $105,000. What value should be recognised for the inventory in this year's accounts? How is the reversal accounted for?

Answer:

- The reversal can only increase the carrying amount to the original cost. Inventory recognised = $100,000.

- The reversal benefit of $18,000 ($100,000 − $82,000) is credited to profit or loss in the period.

Exam Warning: A common error is to reverse more than the original write-down or to carry inventory above original cost if NRV recovers further. IAS 2 only allows reversal up to the original cost—not above.

Revision Tip: Always judge NRV based on conditions at the reporting date. Replacement cost is not relevant unless it affects the estimated selling price or costs to complete.

Summary

- Inventories must be valued at the lower of cost and NRV at each reporting date.

- Write-downs are recognised as expenses when NRV falls below cost.

- Reversal of a write-down is required if the reasons for impairment have reversed, but only up to the original cost.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain when inventories should be written down to NRV under IAS 2

- Calculate and account for write-downs to NRV

- Describe how and when previous write-downs can be reversed

- Recognise disclosure requirements for inventory measurement and adjustments

Key Terms and Concepts

- net realisable value (NRV)

- write-down (of inventory)

- reversal of write-down