Learning Outcomes

After reading this article, you will be able to distinguish investment property from owner-occupied property under IAS 40. You will identify when to classify assets as investment property versus owner-occupied, explain the permitted measurement models, and apply recognition, measurement, and reclassification rules. You will confidently handle exam scenarios involving transfers, accounting entries, and key disclosure requirements.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the accounting treatment and classification of investment property versus owner-occupied property in accordance with IAS 40. Specifically, you should focus your revision on:

- The definition and criteria for investment property under IAS 40

- The distinction between investment property and owner-occupied property (IAS 16)

- Recognition, measurement, and reclassification rules for investment property

- The differences between the cost model and fair value model

- Treatment of transfers between investment property and other asset categories

- Required financial statement disclosures for investment property

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is NOT investment property under IAS 40?

- a) Land held for capital appreciation

- b) Building leased out under an operating lease

- c) Property occupied by the entity’s marketing department

- d) Unused land held for long-term appreciation

-

Which TWO models may an entity elect to use for subsequent measurement of investment property?

- a) Revaluation model

- b) Cost model

- c) Fair value model

- d) Income model

-

What is the correct accounting for a building held for own use that is subsequently leased to a third party under an operating lease?

-

True or false? Changes in the fair value of investment property measured under the fair value model are recognised in other comprehensive income.

Introduction

Property can play multiple roles in a business, such as generating rental income, undergoing appreciation in value, or serving as a base for the entity’s operations. IAS 40 Investment Property prescribes the specific rules for recognising, measuring, and disclosing properties held for rental income and/or capital appreciation—distinct from owner-occupied properties covered by IAS 16. Clear classification is essential, as it dictates both the measurement basis and where gains or losses appear in the financial statements.

Key Term: investment property

Property (land or building—or part of a building, or both) held to earn rentals or for capital appreciation, or both, rather than for use in the entity’s production or supply of goods or services, for administrative purposes, or for sale in the ordinary course of business.Test Tip: When revising Classification vs owner-occupied, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Classification of Property: Investment vs Owner-Occupied

Correctly classifying property under IAS 40 or IAS 16 affects both initial and subsequent accounting.

- Investment property: Land or buildings held to earn rental income or for capital appreciation, or both. The entity does NOT use the property in its own business.

- Owner-occupied property: Property held for use in production, supply, administration, or the entity’s own operations. The property is used by the entity or its employees.

Key Term: owner-occupied property

Property held by the owner (or by the lessee under a finance lease) for use in the production or supply of goods or services, or for administrative purposes.

Mixed-use Properties

Some properties serve both purposes. If the portions can be sold or leased separately, account for each portion individually. If they cannot be divided, and the owner-occupied portion is insignificant, treat the whole as investment property; otherwise, classify as owner-occupied.

Examples of Investment Property

- Office building entirely rented to third parties

- Land held for future price increases, not used in the business

- Property under construction as investment property for future letting

Not Investment Property

- Properties used for administrative, selling, or production functions

- Property intended for sale in the ordinary course of business (inventory)

- Property leased to group companies (in group accounts; in single-entity accounts, may still be investment property)

Worked Example 1.1

An entity owns a building, using 90% for its own offices and 10% rented to an unrelated party. Can any part of the building be classified as investment property?

Answer:

If only a minor portion is rented, the entire building is treated as owner-occupied property under IAS 16. Only where a significant portion is rented out—and can be sold or leased separately—can that portion be classified as investment property.

Measurement of Investment Property

Upon initial recognition, investment property is measured at cost, including directly attributable transaction costs.

IAS 40 permits two models for subsequent measurement:

- Cost model: Measure at cost less accumulated depreciation and any accumulated impairment losses (as under IAS 16). Changes in value are not recognised unless the property is impaired.

- Fair value model: Revalue to fair value at each reporting date, recognising all changes in fair value in profit or loss. No depreciation charge is made.

Once chosen, the model must be applied consistently to all investment properties held by the entity.

Key Term: fair value model

A measurement model under which investment property is revalued to its fair value at each year-end, with changes taken directly to profit or loss.

Worked Example 1.2

Alpha Ltd purchases an office building for $2 million to rent out to third parties. At its first year-end, the fair value is estimated at $2.15 million. Under the cost model, how is this accounted for? Under the fair value model?

Answer:

Cost model: The property is shown at cost less depreciation and any impairment. The fair value increase is ignored. Fair value model: The property is revalued to $2.15 million, and a gain of $150,000 is recognised in profit or loss. No depreciation is charged.

Transfers Between Categories

If an entity changes the use of a property (e.g., starts using it for its own business), transfer between investment property and other categories is required.

- From investment property (fair value model) to owner-occupied: Fair value at transfer date becomes deemed cost under IAS 16.

- From owner-occupied to investment property (fair value model): Revalue to fair value; recognise gain in other comprehensive income if required by IAS 16, then carry at fair value.

Transfers are only made when there is a change in use, e.g., from letting property to owner occupation or vice versa.

Worked Example 1.3

Bravo Ltd has a headquarters building it uses for its own staff. On 1 July, it vacates the property and commences letting to an unrelated company. The property’s carrying value is $1.2 million and its fair value at date of change is $1.35 million. Bravo applies the fair value model under IAS 40.

How is this transfer accounted for?

Answer:

On the date of change, revalue the property to fair value ($1.35 million). The $150,000 gain is recognised in other comprehensive income, as required for revaluations under IAS 16. After transfer, Bravo measures the property under the fair value model, with subsequent changes in fair value recorded in profit or loss.Exam Warning: A common mistake is to treat fair value gains and losses under the fair value model as 'other comprehensive income'. The correct treatment is to take all changes in fair value directly to profit or loss (unless a transfer from owner-occupied property triggers a gain under IAS 16, which first goes to other comprehensive income).

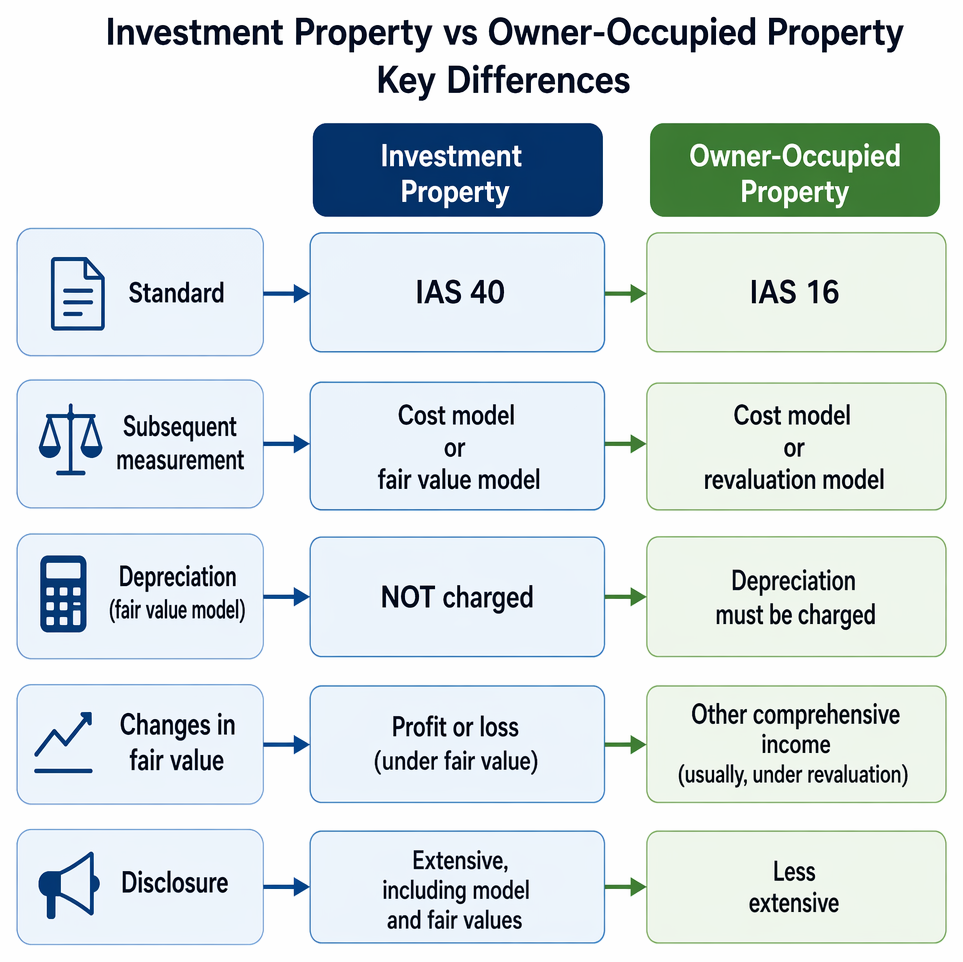

Summary Table: Key Differences

IAS 40 treatment of mixed-use property depends on whether portions are separately saleable or leaseable and whether owner occupation is significant.

| Criterion | Investment Property | Owner-Occupied Property |

|---|---|---|

| Standard | IAS 40 | IAS 16 |

| Subsequent measurement | Cost model or fair value model | Cost model or revaluation model |

| Depreciation (fair value model) | NOT charged | Depreciation must be charged |

| Changes in fair value | Profit or loss (under fair value) | Other comprehensive income (usually, under revaluation) |

| Disclosure | Extensive, including model and fair values | Less extensive |

Key Point Checklist

This article has covered the following key knowledge points:

- Define investment property and owner-occupied property under IAS 40 and IAS 16

- Identify the criteria for classifying a property as investment property

- State the measurement models available for investment property

- Apply transfer rules when a property changes use between categories

- Explain the recognition of fair value changes under each model

- Distinguish disclosures required for investment property

Key Terms and Concepts

- investment property

- owner-occupied property

- fair value model