Learning Outcomes

After reading this article, you will be able to explain the criteria for classifying non-current assets as held for sale under IFRS 5, understand the measurement and presentation requirements for these assets, and describe how discontinued operations are identified and reported in financial statements. You will recognize the impact these concepts have on both the statement of financial position and the statement of profit or loss.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the treatment and disclosure of non-current assets held for sale and discontinued operations under IFRS 5. In particular, this article covers:

- The conditions for classifying non-current assets and disposal groups as held for sale under IFRS 5

- The measurement basis for assets held for sale

- How to present and disclose assets held for sale on the statement of financial position

- The definition and identification of discontinued operations

- The required disclosures and presentation of results from discontinued operations in the statement of profit or loss and notes

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What conditions must be met for a non-current asset to be classified as held for sale under IFRS 5?

- How are non-current assets held for sale measured on the statement of financial position?

- True or false? Assets classified as held for sale continue to be depreciated until sold.

- How is a discontinued operation defined, and how must its results be presented in the financial statements?

Introduction

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations introduces specific requirements for classifying, measuring, and presenting assets that a company plans to sell, rather than continue to use. This also affects how major disposals, called discontinued operations, are reported in the profit or loss. Understanding these rules ensures that users are presented with relevant information about both ongoing and ceasing business activities, critical for transparency and comparability.

Key Term: non-current asset held for sale

A non-current asset that is expected to be recovered primarily through a sale transaction rather than through continuing use, provided certain IFRS 5 criteria are met.

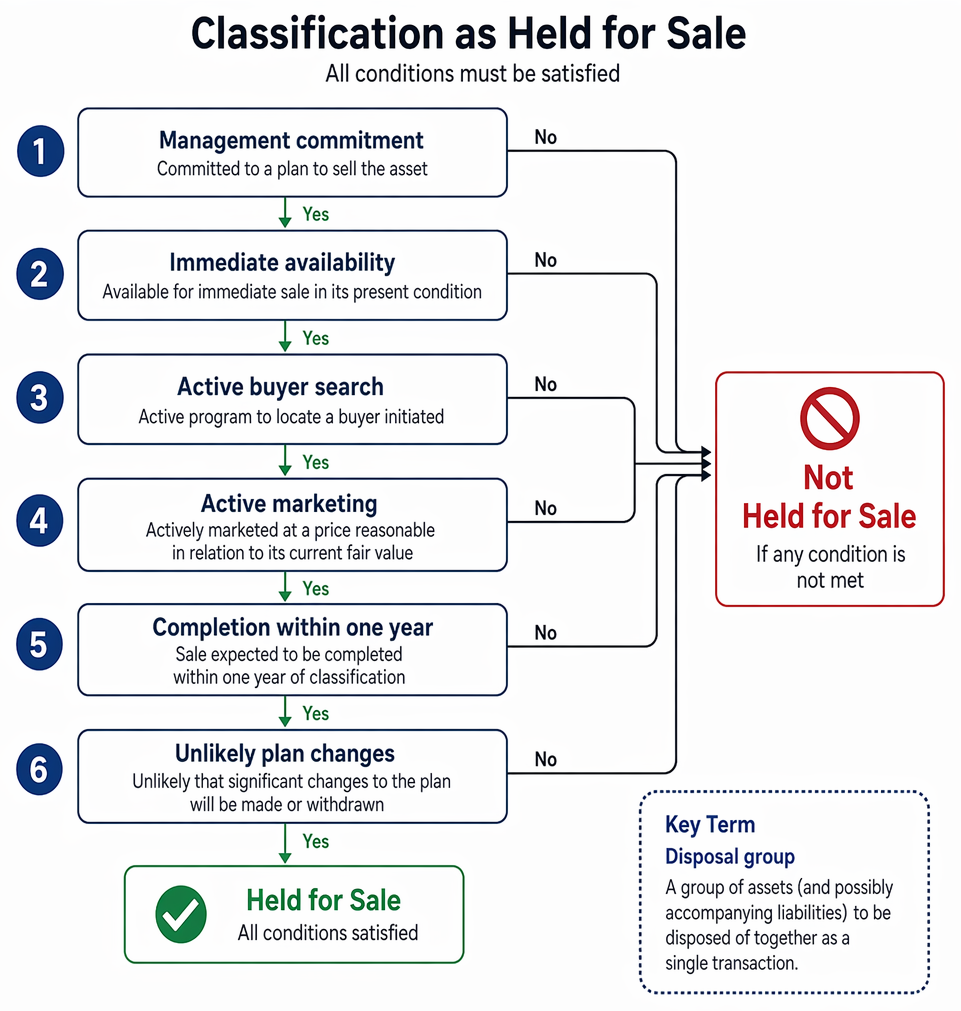

Classification as Held for Sale

To classify a non-current asset or disposal group as 'held for sale', all of the following conditions must be satisfied:

Held-for-sale assets use the lower measurement basis, with any impairment recognised, depreciation discontinued, and subsequent reversal capped at pre-classification carrying amount.

- Management is committed to a plan to sell the asset.

- The asset is available for immediate sale in its present condition.

- An active program to locate a buyer has been initiated.

- The asset is being actively marketed at a price reasonable in relation to its current fair value.

- The sale is expected to be completed within one year of classification.

- It is unlikely that significant changes to the plan will be made or that the plan will be withdrawn.

If any of these conditions is not met, the asset should not be classified as held for sale.

Key Term: disposal group

A group of assets (and possibly accompanying liabilities) to be disposed of together as a single transaction.

Measurement of Non-current Assets Held for Sale

Once an asset (or disposal group) meets the held for sale criteria, it must be measured at the lower of:

- its carrying amount, and

- fair value less costs to sell.

Upon classification as held for sale:

- Depreciation ceases.

- The asset or group is presented separately from other assets on the face of the statement of financial position, usually within current assets.

If the fair value less costs to sell falls below the carrying amount, an impairment loss is recognized in profit or loss. If fair value less costs to sell increases later, a reversal of (some) prior impairment may be recognized, but not to an amount exceeding the original carrying value before the asset was classified as held for sale.

Worked Example 1.1

A company owns equipment with a carrying amount of $25,000. Management decides on 1 October 20X7 to sell the asset and expects sale completion within six months. At 31 December 20X7, the fair value less costs to sell is $22,000.

How should this asset be presented and measured at 31 December 20X7?

Answer:

The asset will be classified as held for sale because the criteria are met. It should be measured at the lower of carrying amount ($25,000) and fair value less costs to sell ($22,000), which is $22,000. An impairment loss of $3,000 ($25,000 – $22,000) is recognized in profit or loss. No further depreciation is charged from 1 October 20X7.Exam Warning: A common error is to continue depreciating assets after classifying them as held for sale. Remember, under IFRS 5, depreciation must stop once an asset is classified as held for sale.

Presentation of Held for Sale Assets and Liabilities

Non-current assets (or disposal groups) classified as held for sale must be presented separately from other assets and liabilities in the statement of financial position, clearly distinguishable from ordinary current or non-current categories.

If the disposal group contains both assets and liabilities to be transferred, each component must be presented separately as 'assets held for sale' and 'liabilities held for sale'.

Key Term: fair value less costs to sell

The estimated selling price in the ordinary course of business, less costs directly attributable to the disposal.

Discontinued Operations

A discontinued operation is a sold (or held-for-sale) business component that:

- Represents a separate major line of business or geographical area of operations, or

- Is part of a single coordinated plan to dispose of such a line or area, or

- Is a subsidiary acquired exclusively with a view to resale.

Key Term: discontinued operation

A component of an entity that has been disposed of or is classified as held for sale and either represents a separate major line of business or geographic area, is part of a single coordinated plan to dispose, or is a subsidiary acquired solely for resale.

The results of a discontinued operation, including any gain or loss on disposal, must be reported as a single amount on the face of the statement of profit or loss, with further detail presented in the notes or on the face if relevant.

Worked Example 1.2

On 1 May 20X6, a company decides to sell its clothing division (a major business line), with completion expected before year-end. The division makes a $45,000 loss before disposal, and the company incurs a $20,000 loss on sale.

How should these be presented in the statement of profit or loss?

Answer:

Both the $45,000 pre-disposal loss and $20,000 disposal loss are included within 'profit/loss from discontinued operations', presented as a single line item on the face of the profit or loss statement, with breakdown details in a note.

Financial Statement Impact

Statement of Financial Position

- Held for sale assets are presented as a separate line (within current assets).

- Related liabilities are shown as 'liabilities associated with assets held for sale'.

Statement of Profit or Loss

- The post-tax result of discontinued operations is shown as one line below continuing operations.

- Gains or losses on disposal, plus any impairment, are included in this line.

Worked Example 1.3

On 30 September 20X8, a company classifies its food processing plant as held for sale. Its carrying value is $150,000, fair value is $160,000, and costs to sell are $12,000.

What is the value of the asset on the statement of financial position?

Answer:

Fair value less costs to sell is $148,000 ($160,000 – $12,000), which is less than $150,000 carrying amount. The asset is measured at $148,000, and an impairment loss of $2,000 is recognized in profit or loss.

Key Presentation and Disclosure Rules

- Classification applies only when all held for sale criteria are met.

- Depreciation ceases once classified as held for sale.

- Prior period figures are not restated unless the operation is discontinued; prior year comparative profit or loss figures should be restated to distinguish between continuing and discontinued operations.

- Disclosures must enable users to assess the financial effect of discontinued operations and assets held for sale on the company’s financial position and performance.

Revision Tip: If asked to prepare profit or loss extracts or explain a disposal, clearly separate results from continuing and discontinued operations using the proper heading. Use the breakdown in the notes for further detail.

Summary

IFRS 5 prescribes strict rules for classifying and measuring non-current assets held for sale and discontinued operations. Classification as held for sale requires specified criteria, and once met, assets are measured at the lower of carrying amount and fair value less costs to sell, and depreciation stops. Discontinued operations—major business lines or geographies sold or held for sale—must have their results and any disposal gain/loss separately presented. This gives users a clear view of ongoing versus ceasing activities.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish when a non-current asset or disposal group is classified as held for sale under IFRS 5

- Explain the measurement basis (lower of carrying amount and fair value less costs to sell) for assets held for sale

- Identify the presentation of these assets and liabilities in the statement of financial position

- Define a discontinued operation and recognize the required single-line profit or loss disclosure

- State that depreciation ceases for assets classified as held for sale

- Recall key required disclosures for held for sale assets and discontinued operations

Key Terms and Concepts

- non-current asset held for sale

- disposal group

- fair value less costs to sell

- discontinued operation