Learning Outcomes

After reading this article, you will be able to explain the criteria for recognising property, plant and equipment (PPE) under IAS 16, determine which costs are included in initial measurement, and understand how assets with separately significant parts—componentisation—are treated for depreciation. These principles are core for ACCA FR and regularly tested.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the key provisions of IAS 16 Property, Plant and Equipment. In particular, you should be able to:

- Define and apply the recognition criteria for PPE, including when to recognise an asset.

- Identify and calculate which costs are to be included in the initial measurement of PPE.

- Explain the treatment of subsequent expenditure, including capital and revenue items.

- Apply the concept of componentisation—identifying major parts of an asset with different useful lives and accounting for each component separately.

- Demonstrate the impact of these rules in the preparation of financial statements.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which two conditions must be met before an item of property, plant and equipment can be recognised as an asset under IAS 16?

- List at least four costs that can be included in the initial measurement of PPE.

- A company spends £50,000 on replacing a truck’s engine. Should this expenditure be capitalised or expensed? Briefly explain.

- How should an aircraft with engines and body that have different useful lives be depreciated under IAS 16?

Introduction

Property, plant and equipment (PPE) are significant assets for most entities. Correct application of IAS 16 is essential to ensure the financial statements present a fair view of an entity’s resources and results. This article focuses on the rules for when to recognise assets, which costs are included at initial measurement, and how to deal with assets made up of significant parts—known as componentisation.

IAS 16 requires entities to only include items as PPE if certain conditions are met, and to measure them at cost on initial recognition. Correct identification of costs avoids misstatements of profit. Componentisation, a common exam topic, ensures more accurate allocation of depreciation and better reflects the asset's economic reality.

Key Term: property, plant and equipment (PPE)

Tangible assets held for use in the production or supply of goods or services, for rental to others, or for administrative purposes, and expected to be used during more than one period. Key Term: componentisation

The treatment of parts of a PPE asset as separate components, each depreciated over its own useful life if those parts are significant in value compared to the whole asset.

RECOGNITION OF PROPERTY, PLANT AND EQUIPMENT

An item of property, plant and equipment should be recognised if both:

- It is probable that future economic benefits associated with the item will flow to the entity; and

- The cost of the item can be measured reliably.

This means that routine maintenance and repairs are not recognised as assets, as they do not provide future benefits—only maintain the asset's current condition.

Key Term: recognition criteria

The conditions that must be met under IFRS for an item to be included as an asset or liability in the financial statements.

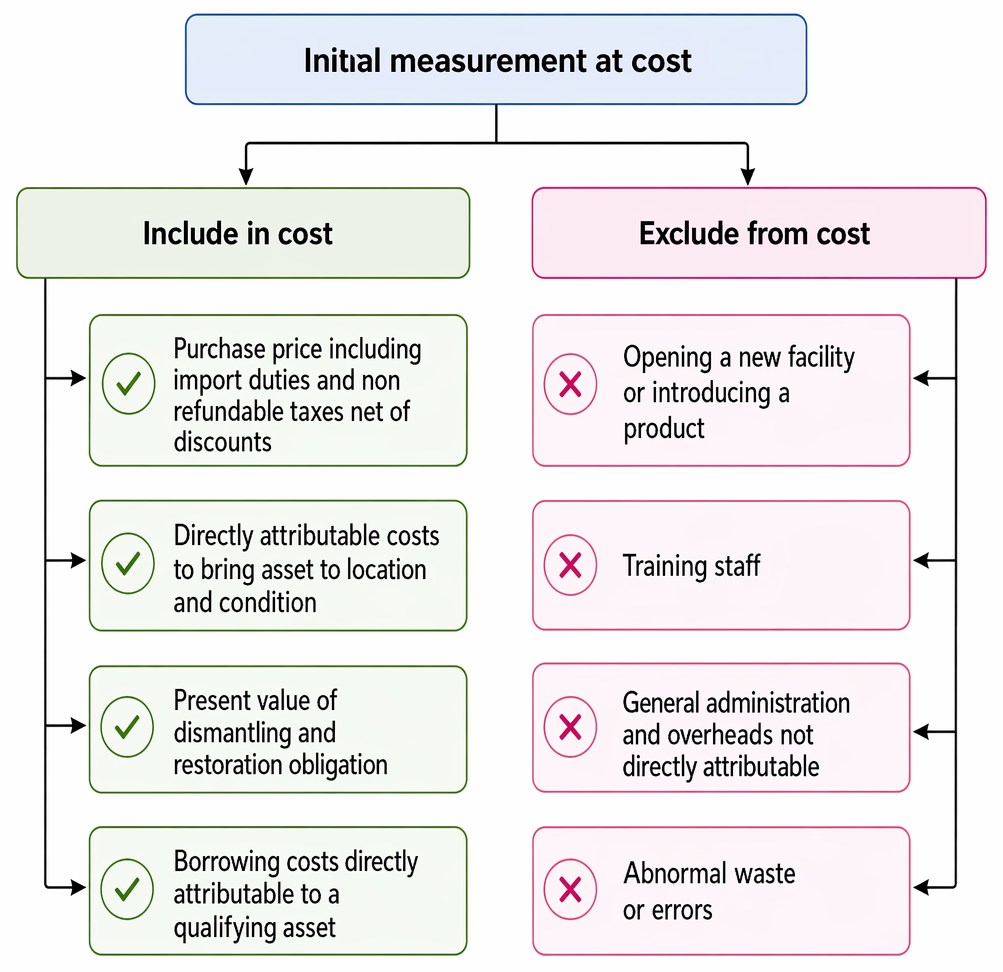

INITIAL MEASUREMENT—WHAT COSTS ARE INCLUDED?

On initial recognition, PPE are measured at cost. 'Cost' includes:

Property, plant and equipment cost under IAS 16 is classified into includable acquisition costs and expenditures recognised in profit or loss.

- Purchase price (including import duties, non-refundable taxes, less trade discounts and rebates)

- Directly attributable costs to bring the asset to the location and condition necessary for its intended use (e.g., site preparation, delivery, installation, professional fees)

- Initial estimates of dismantling and site restoration costs (discounted to present value)

- Borrowing costs directly attributable to the acquisition of qualifying assets (see IAS 23)

Costs excluded from initial measurement:

- Costs of opening a new facility, introducing a new product, or advertising

- Costs of training staff to use the asset

- Administration or general overheads not directly attributable

- Abnormal costs (e.g., wasted materials, avoidable errors)

Worked Example 1.1

Question: Calder Co builds a new warehouse. It pays £200,000 for land, £18,000 for site clearance, £350,000 for construction, £7,000 for delivery of materials, and £12,000 for architect fees. £20,000 is spent on staff training. What is the initial cost of the asset to be recognised?

Answer:

- Land: £200,000

- Site clearance: £18,000

- Construction: £350,000

- Delivery: £7,000

- Architect fees: £12,000 Training costs (£20,000) are expensed. Total cost capitalised: £587,000

Dismantling or restoration — what is required?

If an entity will be required to dismantle an item and restore its site, it must estimate these costs and capitalise the present value of this obligation as part of the asset's initial cost. The obligation is recognised as a liability.

Worked Example 1.2

Question: Summit Drilling installs machinery for oil extraction. At the end of its 10-year useful life, it must dismantle the equipment at an expected cost of £100,000. Calculate the present value included in cost if the discount rate is 5%.

Answer:

Present value = £100,000 ÷ (1.05^10) ≈ £61,391 The asset is recognised at cost plus £61,391 for dismantling. A liability of £61,391 is also recognised for the future outlay.Exam Warning: Forgetting to discount estimated restoration costs to present value is a common mistake. In the exam, always discount future costs before adding to the asset's cost.

SUBSEQUENT EXPENDITURE—ASSET OR EXPENSE?

Post-acquisition costs are only capitalised if they increase the asset's economic benefits—e.g., extend useful life, increase output, or improve efficiency. Normal repairs and routine maintenance are expensed as incurred.

Replacement of a major part (e.g., aircraft engine) is capitalised as a new asset component, and the carrying amount of the replaced part is derecognised.

Key Term: subsequent expenditure

Spending on PPE after its initial recognition; capitalised only if it increases future economic benefits above those originally assessed.

Worked Example 1.3

Question: Aquaplane Co owns a bottling machine consisting of a pump (£60,000 original cost, expected to last 6 years) and a filling unit (£40,000, expected to last 15 years). After 7 years, the pump is replaced at a cost of £75,000. What is the impact?

Answer:

The original pump has reached the end of its useful life and should be derecognised (i.e., carrying value written off). The cost of the replacement pump (£75,000) is capitalised as a new component; depreciation starts over this pump’s new expected life.Revision Tip: Exam questions often present a replacement scenario—always derecognise the old component before adding the new one.

COMPONENTISATION—DEPRECIATING SIGNIFICANT PARTS SEPARATELY

If an item of PPE comprises parts with significantly different useful lives or consumption patterns, each significant part (component) should be recognised and depreciated separately.

Common examples:

- Aircraft: body and engines have different useful lives

- Buildings: roof, lifts, HVAC systems often replaced at different intervals

- Ships: hull and engine

Each component is depreciated over its own expected life. When a component is replaced, its carrying amount is derecognised.

Key Term: depreciation

The systematic allocation of the depreciable amount of an asset over its useful life.

Worked Example 1.4

Question: Oryx Airlines buys an aircraft for $12m. The fuselage ($8m) has a useful life of 20 years; the engines ($4m) only 8 years. How are depreciation expenses determined?

Answer:

- Fuselage: $8m ÷ 20 years = $400,000 per year

- Engines: $4m ÷ 8 years = $500,000 per year Depreciate each part separately; when the engines are replaced, the carrying amount is removed, and the new engines capitalised.

Exam Warning — Componentisation

Failing to depreciate significant components separately—or to derecognise replaced components—is penalised in ACCA exams.

Summary

IAS 16 requires PPE to be recognised only if future benefits are probable and costs can be reliably measured. Initial cost includes directly attributable expenses and estimated discounted dismantling/restoration costs. Routine maintenance is expensed; major replacements can be capitalised if they increase economic benefits. Separately significant components (componentisation) must be identified, capitalised, and depreciated over their respective useful lives.

Key Point Checklist

This article has covered the following key knowledge points:

- List and explain the IAS 16 recognition criteria for PPE assets

- Identify which costs are included in initial measurement, and those excluded

- Calculate present value restoration costs for inclusion in asset cost

- Differentiate between capital and revenue expenditure for subsequent costs

- Apply componentisation: recognising and depreciating significant parts separately

- Understand how to account for major replacements and derecognition of old parts

Key Terms and Concepts

- property, plant and equipment (PPE)

- componentisation

- recognition criteria

- subsequent expenditure

- depreciation