Learning Outcomes

After reading this article, you will be able to explain the difference between asset and expense items, outline the stages and issues in preparing an asset expenditure budget, and describe the capital investment appraisal process. You will learn to distinguish cash flows from profit, identify relevant and irrelevant cash flows in evaluating capital projects, and understand the approval and control of large asset spending within organisations. This knowledge is essential for ACCA exam success.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand how capital asset decisions are planned, evaluated, and controlled. This includes the identification of relevant cash flows and the approval process for major investments. This article covers:

- The importance of investment planning and control for capital projects

- The distinction between asset and expense items in budgeting

- Stages and issues in preparing an asset expenditure budget

- Identification and evaluation of relevant cash flows for capital projects

- The approval process for significant asset investments

- The role of capital project cash flows in investment appraisal

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is a relevant cash flow for investment appraisal?

- a) Historic feasibility study cost

- b) Estimated maintenance cost incurred each year as a result of a new machine purchase

- c) Previously incurred marketing expenses

- d) Book value of an existing asset

-

What is the first stage in the asset expenditure budgeting process?

- a) Approve the investment

- b) Identify suitable projects

- c) Forecast asset expenditure requirements

- d) Appraise actual project benefits against the plan

-

Asset expenditure is most likely to result in:

- a) Immediate charge to profit or loss

- b) Creation of a non-current asset on the statement of financial position

- c) Reduction in equity

- d) Increase in inventory

-

True or false? Depreciation is included as an outflow when identifying project cash flows for investment appraisal.

Introduction

Large-scale investments in non-current assets—such as machinery, buildings, or IT systems—require careful planning and control. Asset budgeting is the structured process organisations use to plan, authorise, and monitor major capital expenditures. Investment appraisal ensures that only projects offering suitable returns on investment are approved and undertaken.

Unlike routine expense items charged straight to profit or loss, capital asset purchases are recorded as non-current assets and affect both the cash position and future profitability. Identifying the correct cash flows and following clear approval procedures are essential steps for good corporate governance and effective management.

Key Term: asset expenditure budget

A detailed plan outlining proposed spending on long-term assets over a period, including committed projects and potential new investments.

Asset and Expense Items

Organisations must separate routine expenditures from capital outlays. Expense items relate to day-to-day running costs (such as repairs or administration) and are charged directly to profit or loss when incurred. Asset items are capital investments, such as the purchase of machinery, equipment upgrades, or improvements that increase earning capacity. These are shown on the statement of financial position as non-current assets, then depreciated over their useful lives.

Key Term: capital project

A significant investment in long-term assets expected to generate benefits over multiple periods, typically subject to a formal approval and appraisal process. Key Term: relevant cash flow

A future, incremental cash inflow or outflow arising only if an investment or decision is undertaken, and excluded if it is already committed or represents a non-cash item.

Purposes and Stages of Asset Budgeting

Budgeting for asset expenditure helps organisations:

Capital project cash flow selection follows sequential tests for futurity, incrementality, cash basis, and project dependence, with examples of included items.

- Forecast long-term resource needs

- Set priorities and allocate capital sensibly

- Control, authorise, and monitor spending to avoid risk and waste

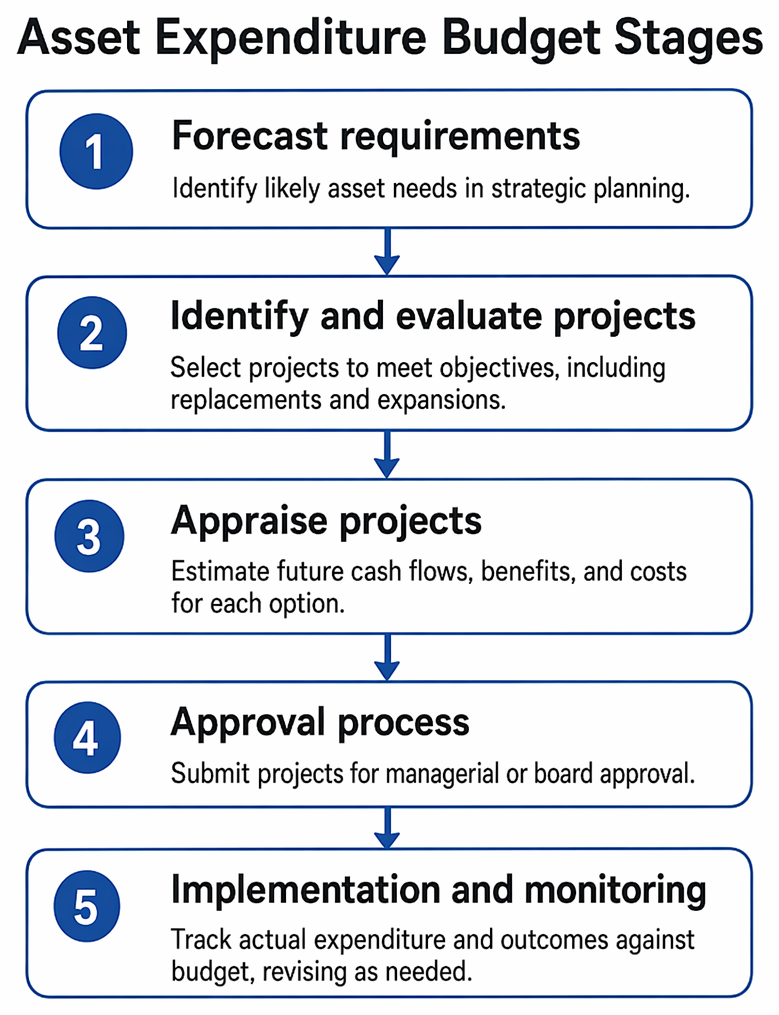

Asset Expenditure Budget Stages

- Forecast requirements: Identify likely asset needs as part of wider strategic planning.

- Identify and evaluate projects: Select capital projects to meet objectives, including replacements and expansions.

- Appraise projects: Estimate future cash flows, benefits, and costs for each option.

- Approval process: Submit projects for managerial or board approval.

- Implementation and monitoring: Track actual expenditure and outcomes against budget, revising as needed.

Issues in Asset Budgets

- Estimating initial and ongoing costs accurately

- Timing of cash flows—purchase, running, maintenance, and disposal

- Budgeting for unforeseen expenditures or delays

- Aligning projects with strategic priorities and available funds

Capital Project Cash Flows

Investment appraisal requires careful identification of all cash flows from a project.

Only cash flows that change as a direct result of the investment are relevant. Non-cash items (such as depreciation) and costs already incurred (sunk costs) are excluded.

Relevant and Irrelevant Cash Flows

Relevant cash flows:

- Additional operating income or cost savings generated by the project

- Outflows for initial investment and installation

- Proceeds from sale of old equipment (net of tax or selling costs)

- Incremental maintenance and running costs

- Disposal proceeds (scrap or resale value) at project end

- Tax effects on incremental profits and outflows

Irrelevant cash flows:

- Past (sunk) costs (e.g. prior feasibility studies)

- Depreciation charges (non-cash)

- Apportioned fixed overheads not changing due to the project

- Book values from the statement of financial position

Key Term: sunk cost

A cost that has already been incurred and cannot be recovered; not relevant to future investment decisions. Key Term: incremental cash flow

The net increase or decrease in cash receipts or payments resulting from selecting one alternative over another.

Worked Example 1.1

A manufacturer plans to replace an old machine with a new model. The new machine will cost £60,000 and require £5,000 installation. It is expected to last 5 years, saving £8,000 per year in operating costs. An old machine, with a book value of £10,000, can be sold for £6,000. A feasibility study costing £2,000 was conducted last year. Identify the relevant cash flows for investment appraisal.

Answer:

Relevant cash flows are:

- £60,000 (outflow, machine purchase)

- £5,000 (outflow, installation)

- £6,000 (inflow, sale of old machine)

- £8,000 per year (inflows, operating cost savings, years 1–5) The £2,000 already spent is a sunk cost and not relevant. Book value of the old asset and depreciation are excluded.

Exam Warning: Exam Warning: Always exclude sunk costs, non-cash items, and costs that would occur regardless of the investment. Only incremental, future cash flows that change if the project is accepted are relevant for appraisal.

The Approval Process for Capital Projects

Due to their size and long-term impact, capital investments follow stricter approval controls than routine expenses.

Typical Approvals Process

- Initial proposal submitted by department or project sponsor

- Review by relevant managers or capital expenditure committee

- Independent assessment of costs, benefits, and risks

- Board-level approval for very large or strategic projects

- Ongoing reporting on expenditure versus budget and expected returns

Organisations set authorisation limits: projects above a certain amount may require approval by the finance director or board. Delegating authority sensibly helps control risk while allowing operational flexibility for routine replacement projects within lower limits.

Key Term: capital expenditure authorisation

The structured process and hierarchy for obtaining approval to incur capital spending, ensuring oversight and control.

Linking Asset Budgeting and Investment Appraisal

Asset expenditure budgeting and investment appraisal are closely connected—budgets provide a pipeline of likely capital projects, while appraisal ensures only projects adding sufficient value are approved. Monitoring actual cash flows and project benefits helps organisations improve forecasts and decision-making in future periods.

Worked Example 1.2

Question: A hospital seeks approval for a new diagnostic imaging unit costing £500,000. Departmental limits require board approval for all projects over £250,000. The investment appraisal indicates annual running cost savings of £80,000 and improved patient throughput. What additional information should the board review before giving final authorisation?

Answer:

The board should review:

- Appraisal calculations and sensitivity analysis

- Funding sources and impact on liquidity

- Risk assessment (e.g., delays, cost overruns)

- Alignment with strategic objectives

- Compliance with capital approval policy

Monitoring and Control of Asset Expenditure

After approval and implementation, the actual expenditure and realised benefits must be monitored:

- Compare actual cash outflows and project progress against the original budget

- Report variances promptly to senior management

- Revise or stop projects if costs exceed expected benefits

- Document lessons learned for use in future investment planning

Revision Tip: Revision Tip: Always focus on incremental, future cash flows—not profit or accounting-based measures—when identifying relevant information for capital budgeting exam questions.

Summary

Budgeting for capital assets ensures organisations allocate resources wisely and control substantial, long-term investments. Only incremental and future cash flows are relevant for investment decisions, while non-cash items and sunk costs are excluded. The asset budgeting process includes careful forecasting, detailed appraisal, formal approval, and continuous monitoring to ensure that each investment project delivers the expected value.

Key Point Checklist

This article has covered the following key knowledge points:

- The distinction between asset and expense items in financial planning

- The stages and purpose of preparing an asset expenditure budget

- How to identify and evaluate relevant and irrelevant cash flows for investment appraisal

- Understanding approval processes for capital projects and authorisation limits

- The importance of monitoring approved asset spending and project outcomes

Key Terms and Concepts

- asset expenditure budget

- capital project

- relevant cash flow

- sunk cost

- incremental cash flow

- capital expenditure authorisation