Learning Outcomes

By completing this article, you will be able to distinguish between cost objects, cost units, cost centres, profit centres, investment centres, and revenue centres. You will understand how organisational costs are classified by function, element, and behaviour, and appreciate the practical importance of cost behaviour for budgeting, decision making, and performance assessment. This knowledge will enable you to interpret questions and data relating to internal cost analysis—core skills for the ACCA exam.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand how costs are classified and assigned throughout an organisation. In your revision, focus on:

- Explaining the concept of cost classification by function, element, and behaviour

- Identifying and explaining cost objects and cost units

- Describing the roles of cost, profit, investment, and revenue centres in responsibility accounting

- Interpreting the needs for information of different responsibility centre managers

- Applying cost behaviour analysis in budgeting and control

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the difference between a cost centre and a profit centre?

- Give one example each of a cost object and a cost unit.

- Which type of cost centre manager is also responsible for investment decisions?

- a) Revenue centre

- b) Cost centre

- c) Profit centre

- d) Investment centre

- Which feature best describes a stepped fixed cost?

- a) Cost varies in direct proportion to output

- b) Cost remains constant within certain activity ranges, then increases in steps

- c) Cost is entirely variable

- d) Cost is always direct

Introduction

Cost classification and cost behaviour are building blocks of management accounting. Every organisation must analyse and manage costs to support planning, decision making, and control. Costs must be assigned to activities and products (cost objects) through appropriate units and responsibility centres. Understanding how costs are classified by function, behaviour, and responsibility is critical to producing meaningful information for management.

COST OBJECTS AND COST UNITS

Businesses need to identify the activity or item for which a separate cost measurement is useful. This is where cost objects and cost units are essential.

Key Term: Cost Object

Any activity, item, or segment for which a separate measurement of cost is required, such as a product, service, project, or department. Key Term: Cost Unit

A unit of product or service in relation to which costs are ascertained; the basic measure for costing purposes, such as a kilogram, litre, or individual item.

A cost object can be as broad as an entire division, or as specific as a single customer order. Selecting suitable cost units allows accurate cost allocation to products and services.

Worked Example 1.1

A hotel provides accommodation and meal services to guests. What could be considered (a) a cost object, and (b) a cost unit in this context?

Answer:

(a) Cost object: The hotel's restaurant; (b) Cost unit: A single room-night or a single meal served.

COST CENTRES AND RESPONSIBILITY CENTRES

Responsibility accounting divides an organisation into segments, each overseen by a manager responsible for certain performance areas.

Cost behaviour categories are linked to whether total cost varies, remains constant, steps upward, or contains mixed elements.

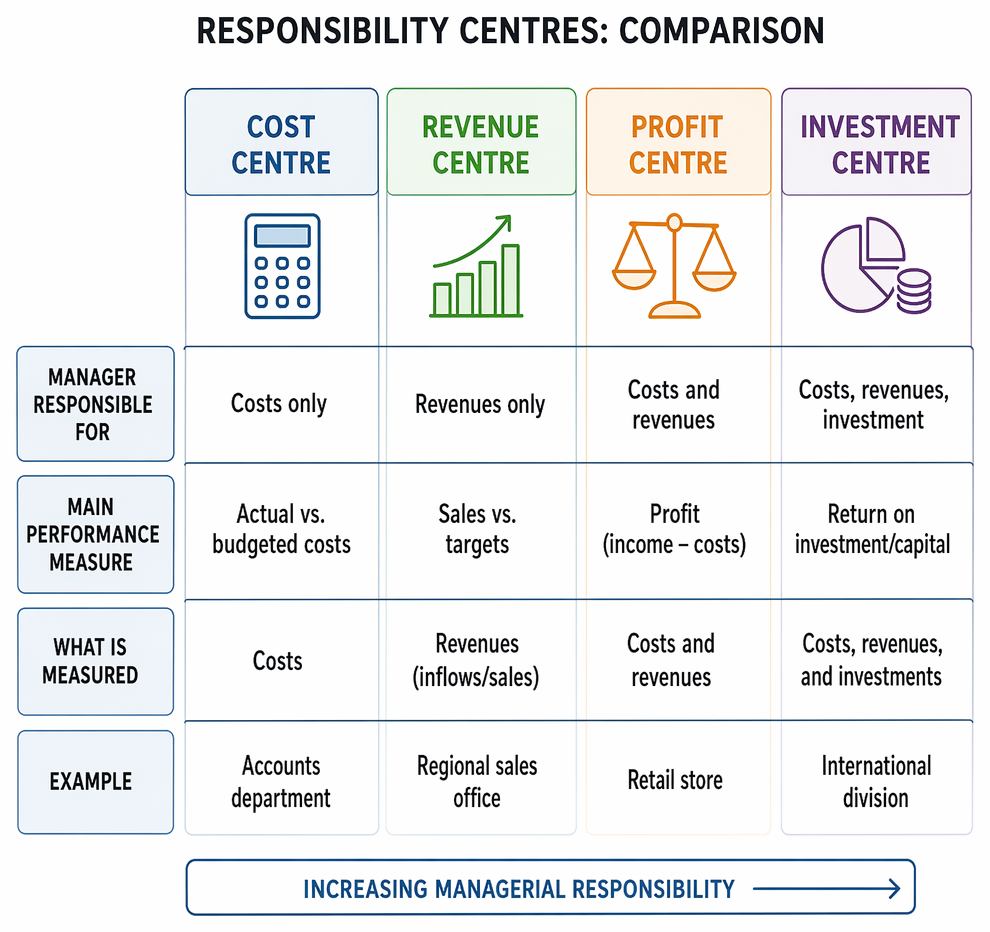

Key Term: Cost Centre

A location, department, activity, or equipment for which costs are collected and controlled, and where a manager is responsible only for those costs. Key Term: Revenue Centre

A part of the organisation responsible primarily for generating revenue, where only inflows (sales) are measured and not allocated costs. Key Term: Profit Centre

A segment for which both revenues and costs are identified, allowing measurement of profitability and the manager is responsible for both. Key Term: Investment Centre

A segment where the manager is responsible not only for revenues and costs, but also for investments in assets and use of capital.

A manufacturing company may have departments such as machining, assembly, and sales. Each can be organised as a cost, profit, or investment centre depending on the level of responsibility conferred.

Responsibility Centre Comparison Table

| Type | Manager Responsible For | Main Performance Measure | Example |

|---|---|---|---|

| Cost Centre | Costs only | Actual vs. budgeted costs | Accounts department |

| Revenue Centre | Revenues only | Sales vs. targets | Regional sales office |

| Profit Centre | Costs and revenues | Profit (income - costs) | Retail store |

| Investment Centre | Costs, revenues, investment | Return on investment/capital | International division |

Worked Example 1.2

Question: In a national retail group, sales teams in each region generate sales but have no authority over costs or investments. What type of responsibility centre best describes a regional sales team?

Answer:

A revenue centre—responsible for sales, but not costs or capital investment.

INFORMATION NEEDS OF RESPONSIBILITY CENTRE MANAGERS

The type of information required depends on the centre's nature:

- Cost centre managers need detailed cost reports and variance analysis to control spending.

- Profit centre managers require income statements with both revenue and cost data, plus budget comparisons.

- Investment centre managers need data on investment returns, asset utilisation, and capital employed, in addition to profitability and cost data.

Managers must be accountable only for performance measures they can reasonably influence.

Exam Warning: It is incorrect to hold a cost centre manager responsible for revenue performance or investment decisions. Only assign responsibility for factors within their control.

COST BEHAVIOUR: VARIABLE, FIXED, STEPPED, SEMI-VARIABLE

Understanding cost behaviour is essential for planning and forecasting.

- Variable costs change directly with activity level (e.g., direct materials).

- Fixed costs remain constant within a relevant range, irrespective of output (e.g., factory rent).

- Stepped fixed costs are fixed over certain activity ranges but increase in steps when output passes certain thresholds.

- Semi-variable costs include both fixed and variable components (e.g., telephone bill with a fixed line charge plus usage).

Worked Example 1.3

Question: A factory supervisor earns a fixed salary that increases by $2,000 per annum for every increment of 20 additional employees overseen. What type of cost behaviour is this?

Answer:

This is a stepped fixed cost—remains constant within a certain activity range, then increases in a step as activity exceeds that limit.Revision Tip: To identify whether a cost is direct or indirect, always ask: "Can this cost be specifically traced to a single cost unit or cost object?" If yes, it's direct; if not, it's indirect/overhead.

DIRECT AND INDIRECT COSTS

Assigning costs accurately is essential for decision making.

Key Term: Direct Cost

A cost that can be attributed and traced directly to a particular cost object or cost unit, e.g., raw materials for a product. Key Term: Indirect Cost

A cost that cannot be directly traced to a single cost object or unit; these are overheads, spread across multiple outputs, e.g., factory electricity.

For example, the salary of a maintenance engineer is an indirect cost—it's shared across production.

Worked Example 1.4

A bakery buys flour for making bread and pays rent for its premises. Which is a direct cost for a loaf of bread, and which is indirect?

Answer:

Flour is a direct cost for each loaf; rent is an indirect cost (overhead).

PRODUCTION VS NON-PRODUCTION COSTS

- Production costs relate to manufacturing or providing a service, including direct materials, direct labour, and production overheads. These are included in inventory valuations.

- Non-production costs include administrative, selling, distribution, and finance costs. These are period expenses, not included in product valuation.

| Cost Category | Included in Inventory? | Example |

|---|---|---|

| Production Cost | Yes | Machine operator's wages, ingredients |

| Non-production Cost | No | Advertising, office rent |

COST CARDS: COST SUMMARIES FOR MANAGEMENT

A cost card summarises the unit or batch cost by integrating all relevant cost elements.

Key Term: Cost Card

A document or system that records all costs (direct and indirect) assigned to a product, batch, or service unit.

Cost cards support pricing, profitability analysis, and control.

Worked Example 1.5

Question: A company produces custom hats. Each hat uses £4 of material, £3 of direct labour, and £2 in indirect overheads. What information would the cost card supply?

Answer:

The cost card shows direct costs (£4 + £3 = £7) and total cost per unit (£9 per hat).

CODES FOR COST CLASSIFICATION

Efficient cost collection requires systematic classification using cost codes. Coding can be by sequence, block, hierarchy, significant digit, or mnemonic.

Key Term: Cost Code

A unique combination of symbols and/or numbers applied to costs for classification and easier analysis.

Codes assist in streamlined entry, analysis, and reporting—key for larger organisations.

Summary

Effective cost classification lets managers assign costs accurately to activities, products, and departments. There are clear distinctions between cost objects, units, cost centres, profit centres, and investment centres. Each type of responsibility centre requires specific information for accountability and performance management. Direct costs can be traced to outputs; indirect costs must be spread or apportioned. Recognising variable, fixed, stepped, and semi-variable behaviour is essential for budgeting and forecasting. Cost cards and coding systems support efficient reporting and analysis.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguishing cost objects and cost units, with clear examples

- Identifying cost, profit, investment, and revenue centres, and their purposes

- Understanding the information needs of different responsibility centre managers

- Classifying costs as direct or indirect for effective cost assignment

- Explaining variable, fixed, stepped, and semi-variable cost behaviour

- Recognising the difference between production and non-production costs

- Describing the purpose of cost cards and cost codes

Key Terms and Concepts

- Cost Object

- Cost Unit

- Cost Centre

- Revenue Centre

- Profit Centre

- Investment Centre

- Direct Cost

- Indirect Cost

- Cost Card

- Cost Code