Learning Outcomes

After reading this article, you will be able to explain why and how cost data and forecasts must be adjusted for price changes in budgeting and decision-making. You will understand how to use index numbers to restate historical and projected figures at constant price levels, distinguish between nominal and real values, and perform calculations for inflation-adjusted cost estimations. This article will prepare you to identify when adjustment is necessary and apply relevant formulas and techniques in ACCA exam questions.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand the effects of inflation and price changes on cost estimation and forecasting. This article covers the following essential syllabus points:

- Explain the purpose of index numbers and calculate simple and weighted index numbers.

- Adjust historical and forecast data for price movements using index numbers.

- Distinguish between real and nominal monetary values in budgeting and forecasting.

- Interpret the implications of inflation and deflation for management decision making.

- Apply adjusted cost data to forecasts and budget preparation.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the main reason for adjusting historical cost data when forecasting future costs in an environment of rising prices?

- a) To comply with legal requirements

- b) To express all costs at a common price level

- c) To eliminate variable costs

- d) To identify sunk costs

-

A project incurred material costs of $60,000 in 20X5 (index 120). What is the equivalent cost in 20X8 if the index for 20X8 is 144?

-

Define the difference between "real" and "nominal" values in cost data.

-

Which index formula would you use to adjust a set of historical costs to current price levels:

- a) Simple index

- b) Chain base index

- c) Weighted index

- d) All of the above, depending on the data set

Introduction

When making forecasts or preparing budgets, it is important to recognize that reported costs from past periods may not reflect current or future price levels, especially when inflation or other significant price changes have occurred. Adjusting cost data is essential for meaningful comparison, accurate planning, and effective decision-making. The use of index numbers ensures that all data used in estimation are stated at a consistent price level, removing distortions caused by inflation or deflation.

Cost estimations that ignore inflation can result in unreliable budgets, underestimated resource requirements, and poor management decisions. You must be able to restate historical and projected figures as "real" values, using index numbers to adjust nominal or money amounts, ensuring that all forecasts are stated in terms consistent with the planning period.

Key Term: Index Number

A statistic that expresses a value in relation to a base period, typically expressed as a percentage, used to compare changes in prices or quantities over time.

THE NEED FOR PRICE ADJUSTMENTS IN COST FORECASTING

Any significant change in the general price level (inflation or deflation) affects costs, revenues, and profits. Simply using unadjusted (“nominal”) historical data in forecasts or budgets will not provide an accurate picture if prices have changed. Budgets created without adjusting for price movements will underestimate required expenditure and overestimate profits in an inflationary environment.

When are adjustments required?

- Whenever historical cost or revenue data are used in forecasts and price levels have changed since then.

- When budgeting for future periods in an environment where inflation is likely to occur.

- When comparing performance across different time periods.

Real vs Nominal Values

Key Term: Nominal Value

A monetary amount stated at the value prevailing in the period in which it was recorded, not adjusted for changes in price level. Key Term: Real Value

A monetary amount that has been adjusted to remove the effects of inflation or deflation, so that all values are expressed at a constant price level.

INDEX NUMBERS: FORMULAS AND APPLICATION

Index numbers are central to restating historical or forecast data at a consistent price level. The most common is the price index, which tracks changes in prices over time relative to a base year.

Calculating a Simple Price Index

To convert values from one period to another, or to express all data in "current" terms:

Simple Price Index for Year T =

To adjust a cost from Year A (index = IA) to Year B (index = IB):

Key Term: Deflating

The process of adjusting historical values to a common price level using an index number, removing the effects of inflation.

ADJUSTING COST DATA FOR PRICE MOVEMENTS

Cost restatement for price movements applies target-index-to-original-index scaling to convert historical expenditure to the required price level.

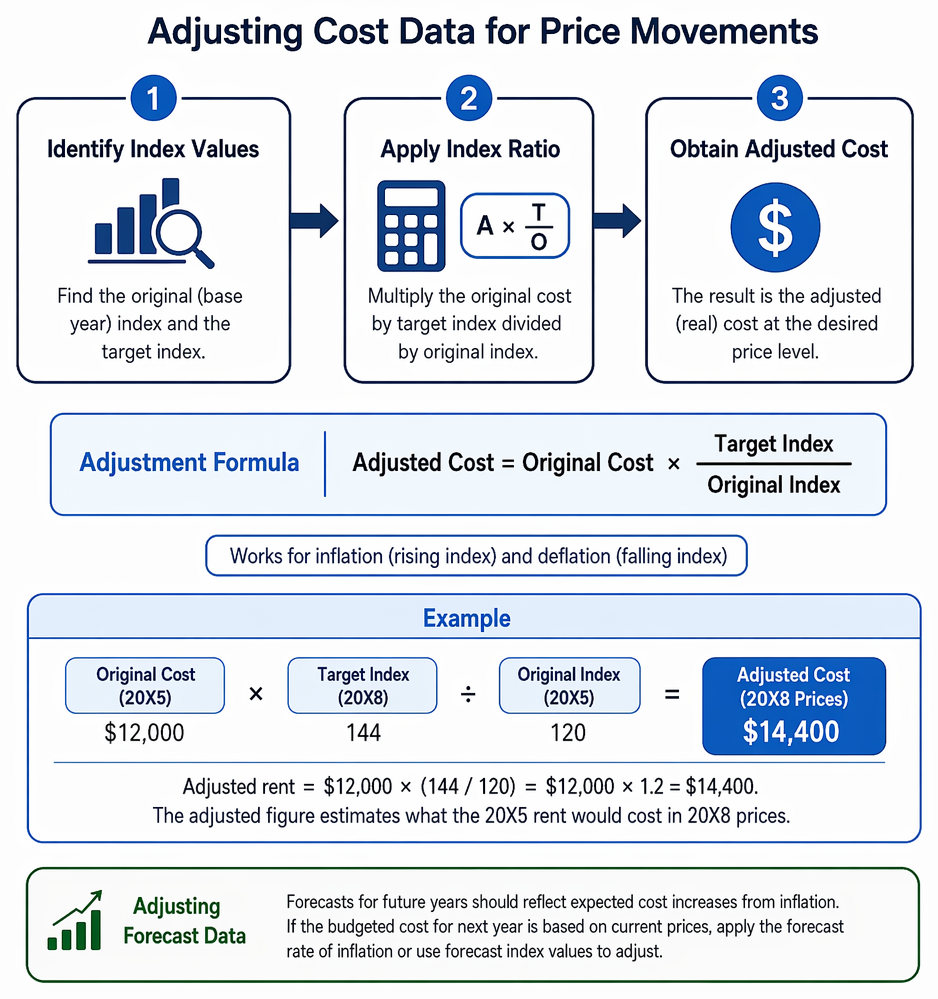

Procedure

- Identify the current and base year index values.

- Multiply the original cost by the ratio of the target index to the original index.

- The result is the adjusted, or real, cost at the desired price level.

This method works for both inflation (rising index) and deflation (falling index).

Worked Example 1.1

A firm’s rent expenditure in 20X5 was $12,000. The general price index in 20X5 was 120. You need to estimate the equivalent cost in 20X8, when the index is 144.

Answer:

Adjusted rent = $12,000 × (144 / 120) = $12,000 × 1.2 = $14,400. The adjusted figure estimates what the 20X5 rent would cost in 20X8 prices.

Adjusting Forecast Data

Forecasts for future years should reflect expected cost increases from inflation. If the budgeted cost for next year is based on current prices, apply the forecast rate of inflation or use forecast index values to adjust.

Key Term: Forecasting

The process of estimating future outcomes (such as costs or revenues) using historical data, adjusted where necessary for anticipated changes such as inflation.

USING WEIGHTED AND CHAIN BASE INDICES

In real-world cost estimation, items may be affected by price changes at differing rates. Sometimes, a weighted price index, such as the Consumer Price Index (CPI), is used to reflect realistic patterns of spending.

Key Term: Weighted Index

An index number that assigns relative importance (weights) to items or components according to their significance or proportion of total value. Key Term: Chain Base Index

An index where each period is compared with the immediately previous period, allowing for continuous updating of the weights and for structural changes over time.

In practice, you may be provided with weighted or chain base indices in exam scenarios. Apply the same conversion method as for simple indices, ensuring you use the correct index for the relevant item.

Worked Example 1.2

The unit material cost for a product in 20X3 was $20 (material price index 110). In 20X7, the price index is 143. What is the equivalent unit cost in 20X7?

Answer:

Adjusted cost = $20 × (143 / 110) = $20 × 1.3 = $26.

ADJUSTING DATA FOR MULTIPLE YEARS AND FOR BUDGETING

When preparing multi-year budgets or forecasts, all costs and revenues should be expressed at projected price levels. This is accomplished by applying expected inflation rates or index numbers. This adjustment ensures comparability across years and prevents under/over-estimation arising from price level differences.

Adjustment sequence for budgeting:

- Restate all historical data at the current or future price level using appropriate indices.

- Apply forecast index values (if available) to project cost increases year on year.

- Ensure that all cash flows within multi-year forecasts are at consistent real or nominal prices as required.

REAL AND NOMINAL VALUES IN PRACTICE

Budgetary and investment appraisal decisions sometimes require distinguishing between real and nominal values:

- Use nominal values (“money of the day”) where cash flow is projected at unadjusted prices (including anticipated inflation).

- Use real values where all amounts are stated at current (constant) prices; apply discounting using a real rate (i.e., excluding inflation).

Worked Example 1.3

A capital project will incur $50,000 of maintenance costs after five years. Maintenance cost is quoted in current prices; annual inflation is expected to be 3%. Calculate the inflated nominal cost in year 5.

Answer:

Future index = 100 × (1.03)^5 = 100 × 1.159 = 115.9 Adjusted cost = $50,000 × (115.9 / 100) = $57,950Exam Warning: Failing to adjust historical cost data for inflation will lead to underestimated budgets and weaken financial control. Always check whether figures are quoted in nominal or real terms before applying indices.

Revision Tip: In calculations, always use the actual relevant index numbers provided in the exam question. Do not assume inflation rates unless stated.

Summary

Accurate cost estimation for budgeting and forecasting requires expressing all values at a common price level. Index numbers allow you to adjust costs and revenues for inflation or deflation, producing real, comparable data. Understanding the difference between real and nominal values and correctly applying price indices is essential for meaningful analysis and reliable forecast figures.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify the need to adjust cost data for price changes in forecasting and budgeting.

- Explain and apply simple, weighted, and chain base indices to adjust costs.

- Distinguish between real and nominal values for budgeting and investment appraisal.

- Perform step-by-step calculations for expressing cost data at a consistent price level.

- Recognize typical exam requirements—when, how, and why to adjust for inflation.

Key Terms and Concepts

- Index Number

- Nominal Value

- Real Value

- Deflating

- Forecasting

- Weighted Index

- Chain Base Index