Learning Outcomes

By the end of this article, you will be able to explain how labour costs are classified, captured, and recorded within management accounts. You will learn the distinction between direct and indirect labour, how to account for payroll and employment costs, and how to prepare accurate journal and ledger entries for labour cost flows. You will understand the use of the payroll control account and identify typical entries required for ACCA exams.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand the principles of labour costing and the accounting processes involved in recording labour costs. The following syllabus areas are addressed in this article:

- Explain and distinguish direct and indirect labour costs

- Prepare journal and ledger entries for recording labour costs in management accounting

- Understand the roles of the payroll, work-in-progress, and overheads accounts in labour cost flows

- Interpret the entries and balances in the labour account

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is classified as an indirect labour cost?

- a) Wages of assembly line workers

- b) Overtime premium for urgent customer order

- c) Factory supervisor’s salary

- d) Piecework wages for production staff

-

When recording payroll costs, where are gross wages initially posted?

- a) Work-in-progress account

- b) Labour account (or wages control account)

- c) Overhead account

- d) Bank account

-

Which account is credited when direct labour is transferred to production?

- a) Labour account

- b) Work-in-progress account

- c) Overhead account

- d) Finished goods account

-

True or false? All overtime premiums are treated as direct labour costs.

Introduction

Labour is a significant cost in many organisations and must be carefully tracked and allocated to ensure accurate product costs and effective management decisions. The recording of labour costs follows defined processes to distinguish direct labour linked to production from indirect labour supporting overall operations. Proper journal and ledger entries are essential for presenting reliable management information, cost control, and reconciliations.

Key Term: direct labour

Labour costs that can be directly identified with and traced to the production of specific products, services, jobs, or cost centres. Key Term: indirect labour

Labour costs not directly traceable to specific products or jobs, typically arising from support functions such as supervision, maintenance, or security.Test Tip: When revising Journal and ledger entries for labour costs, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Labour Cost Classification

Labour costs must be analysed into direct and indirect elements for accurate costing:

- Direct labour: Costs of employees physically working on products or providing direct services—usually charged to work-in-progress.

- Indirect labour: Costs of employees providing supervision, maintenance, cleaning, or administration—not directly included in the cost of units but gathered into overheads.

Direct vs Indirect: Common Examples

| Direct Labour | Indirect Labour | |

|---|---|---|

| Assembly line worker | √ | |

| Factory supervisor | √ | |

| Machine maintenance | √ | |

| Cleaner | √ | |

| Welder for product | √ |

Labour Cost Recording Systems

Labour cost accounting begins with capturing hours and rates, often through time-sheets, clock cards, or electronic systems. Gross payroll is determined by multiplying hours worked (for time-based systems) or units produced (for piecework) by the pay rate, plus allowances or bonuses.

Key Term: payroll control account

An account that collects all gross wages and employment costs before allocation to production, overheads, or other accounts.

Payroll Processing Flow

- Calculate gross wages (includes basic pay and statutory deductions)

- Enter gross wages in the payroll control account (labour account)

- Allocate direct costs to work-in-progress (WIP)

- Allocate indirect costs to production overheads

Net vs Gross Wages

The organisation incurs total employment cost (gross), but employees receive net pay after statutory deductions (PAYE tax, social security, pensions). Only the gross wage is recognised as a cost in management accounts.

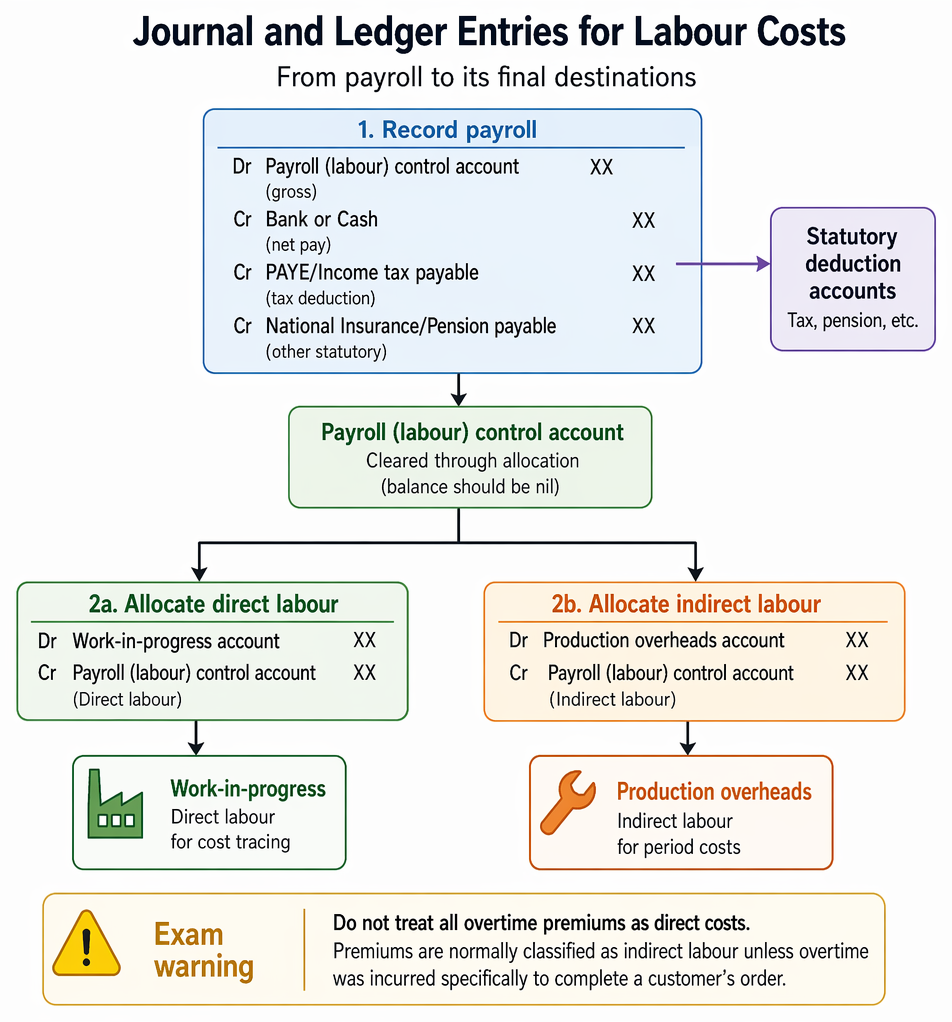

Journal and Ledger Entries for Labour Costs

Proper recording ensures total labour costs are traced from payroll to their rightful destination—supporting product costing, control, and financial reporting.

Payroll journal entries trace labour costs from hours and rates through gross wage recognition, net settlement, deductions, and cost allocation.

Standard Accounts Involved

- Payroll (labour) control account

- Work-in-progress account (WIP)

- Production overhead account

- Bank account (for wage payments)

- Statutory deduction accounts (tax, pension, etc.)

Typical Journal Entries

Step 1: Recording gross wages and deductions

text Dr Payroll (labour) control account [gross wages] Cr Bank or Cash [net pay] Cr PAYE/Income tax payable [tax deduction] Cr National Insurance/Pension payable [other statutory]

Step 2: Allocation of labour costs

-

Direct labour portion:

Dr Work-in-progress account [direct labour] Cr Payroll (labour) control account -

Indirect labour portion:

Dr Production overheads account [indirect labour]

Cr Payroll (labour) control account

At period end, the balance in the payroll control account should be nil if all entries are made correctly.

Worked Example 1.1

A company has gross wages for June totalling £20,000. Of this, £15,000 relates to direct production staff and £5,000 to supervisors and cleaners. The net pay to staff is £16,000 after £4,000 deducted for tax and national insurance. Prepare the journal entries for payroll and allocation.

Answer:

Step 1 – Record payroll: Dr Payroll control account £20,000 Cr Bank £16,000 Cr PAYE/tax payable £4,000 Step 2 – Allocate labour costs: Dr Work-in-progress (direct) £15,000 Dr Production overheads (indirect) £5,000 Cr Payroll control account £20,000

Worked Example 1.2

Question: The payroll department posts wages totalling £10,000. Of this, £8,000 is direct labour, £1,200 is for machine maintenance, and £800 is for canteen staff. How are these costs posted?

Answer:

Dr Work-in-progress £8,000 Dr Production overheads £2,000 Cr Payroll control account £10,000

Allocation Logic

- Direct labour always moves to WIP for cost tracing.

- Indirect labour always moves to overheads.

Exam Warning: Be careful not to treat all overtime premiums as direct costs. Premiums are normally classified as indirect labour unless overtime was incurred specifically to complete a customer's order.

The Labour Account in Practice

The payroll (labour) control account acts as a central hub for all payroll entries. It should balance to zero once all costs are fully allocated and statutory deductions paid.

Typical Movements in the Labour (Payroll) Control Account

| Debit Side | Credit Side |

|---|---|

| Gross wages incurred | Direct labour to WIP |

| Indirect labour to overheads | |

| Deductions to PAYE, NI, etc. | |

| Net pay to bank |

Labour Cost Flows: Overview

- Payroll calculated and entered as gross wage cost.

- Direct labour cost moved to WIP account to become part of product costs.

- Indirect labour cost moved to overheads account for further allocation or absorption.

- Net pay and deductions processed against payroll liability accounts.

Interpreting Labour Account Balances

A nil balance signals all wages have been correctly processed. Any remaining balance indicates incomplete allocation or unpaid wages/deductions requiring further investigation.

Summary Table: Flows for Typical Labour Transactions

| Transaction | Debit | Credit |

|---|---|---|

| Gross wages incurred | Payroll control account | |

| Net wages paid to employees | Bank | |

| Statutory deductions recognised | Tax/pension liability | |

| Direct labour allocated | Work-in-progress account | Payroll control account |

| Indirect labour allocated | Production overheads acct | Payroll control account |

Key Point Checklist

This article has covered the following key knowledge points:

- Define and distinguish direct and indirect labour costs

- Identify the role of the payroll control account in labour cost recording

- Prepare standard journal entries for gross payroll, deduction, and allocation

- Allocate direct and indirect labour correctly to WIP or overheads

- Interpret zero balances and incomplete allocations in the labour control account

Key Terms and Concepts

- direct labour

- indirect labour

- payroll control account