Learning Outcomes

After reading this article, you will be able to calculate and interpret labour efficiency, capacity, and production volume ratios. You will understand how these ratios measure workforce performance and how they are used in management control and performance reporting. You will also recognise how these ratios relate to standard costing and variance analysis—a key part of the ACCA syllabus.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand the principles of labour costing and control. This topic is tested through practical scenarios and calculations. Focus your revision on:

- Calculating direct and indirect labour costs for costing and accounting purposes.

- Identifying how systems capture and record labour time and effort.

- Distinguishing between actual and standard hours in production reporting.

- Calculating and interpreting the labour efficiency, capacity, and production volume ratios.

- Understanding the use of these ratios for measuring and controlling workforce performance within responsibility accounting systems.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the formula for calculating the labour efficiency ratio?

- If standard hours for actual output are 1,800, actual hours worked are 1,900, and budgeted hours are 2,000, calculate the capacity and production volume ratios.

- What does a capacity ratio of 95% indicate about actual hours worked?

- Name the three core labour ratios that form part of standard costing performance measurement.

Introduction

Accurate labour costing is essential for effective cost accounting, planning, and performance measurement. Beyond recording total hours worked and paid, businesses need to know how efficiently and consistently the workforce operates compared to targets. For this, three key ratios are used: the labour efficiency ratio, labour capacity ratio, and labour production volume (or activity) ratio. These ratios help managers:

- Assess how well labour is being used.

- Compare actual performance with standard expectations.

- Identify causes of any variances and take corrective action.

A clear understanding of these measures supports better control and more precise costing in both service and manufacturing organisations.

Key Term: Labour efficiency ratio

The proportion of actual productive hours compared to the standard hours for the actual output, expressed as a percentage. Key Term: Labour capacity ratio

The comparison of actual hours worked to the budgeted or planned hours, shown as a percentage. Key Term: Labour production volume ratio

The ratio of standard hours for actual output to the budgeted hours, measuring output achieved against original plans.

Why Labour Ratios Matter

Management accounting relies on both actual data and standards. Labour ratios are a bridge between the two, allowing you to measure how effective the workforce is, track resource usage, and support performance appraisal systems.

- Efficiency ratio reveals productive use of time against the standard.

- Capacity ratio indicates whether available working hours were utilised.

- Production volume ratio (also known as the activity or production volume ratio) shows the extent to which output targets have been met.

These ratios are closely linked and, when used together, assist in variance analysis and responsibility accounting.

Calculating Labour Ratios

Each ratio has a specific formula and a distinct role:

Labour ratio interpretation links efficiency, capacity, and production volume percentages to standard productivity, budgeted hours usage, and planned output outcomes.

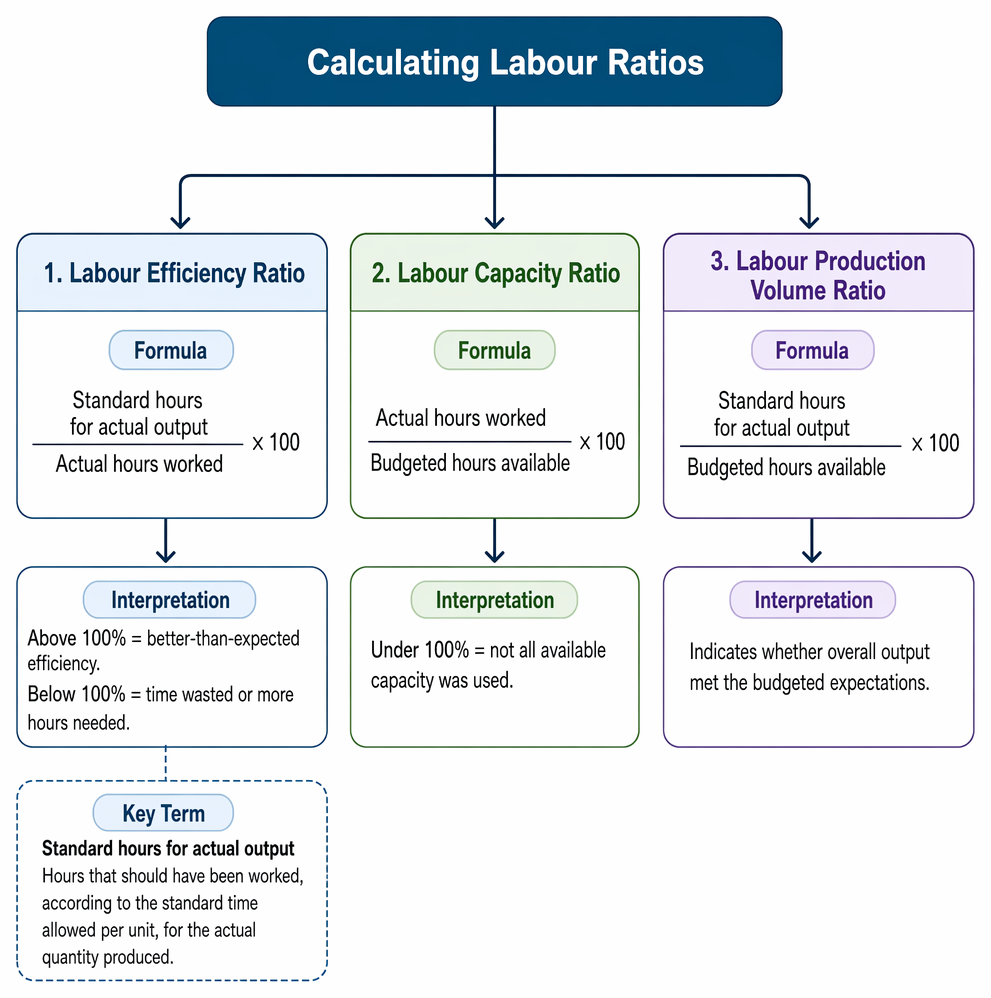

Labour Efficiency Ratio

This measures how efficiently labour was used, by comparing the standard hours required for actual production with the actual hours worked.

Formula:

A result above 100% shows better-than-expected efficiency; below 100% suggests time was wasted or more hours were needed.

Key Term: Standard hours for actual output

The hours that should have been worked, according to the standard time allowed per unit, for the actual quantity produced.

Labour Capacity Ratio

This examines how many hours were actually worked compared to what was originally budgeted or planned to be available.

Formula:

A ratio under 100% means not all available capacity was used.

Labour Production Volume Ratio

Also called the 'activity' or 'production volume' ratio, this shows whether the overall output met the budgeted expectations.

Formula:

The Link Between Ratios

The three ratios are mathematically connected:

This means the overall achievement (volume ratio) is the result of both efficient use (efficiency ratio) and the amount of capacity actually utilised (capacity ratio).

Using Labour Ratios in Performance Reporting

Labour ratios are used in standard costing to enable:

- Comparison of workforce performance over time.

- Identification of causes of adverse (or favourable) labour variances.

- Appraisal of production managers' or supervisors' effectiveness.

For managers, these ratios highlight where time was lost, whether due to inefficiencies, lack of work, machine breakdowns, or outside factors such as low demand. Action can then be taken to address specific issues—by improving processes, increasing training, or adjusting workforce size.

Worked Example 1.1

Worked Example 1.1 Details

A company budgets 1,200 hours for a production period and expects to make 600 units. The standard time per unit is 2 hours. Actual output is 650 units and it took 1,300 hours to produce them.

Required: Calculate the efficiency, capacity, and production volume ratios.

Answer:

Standard hours for actual output = 650 units × 2 hours = 1,300 hours Actual hours worked = 1,300 Budgeted hours = 1,200 Efficiency ratio: = (1,300 / 1,300) × 100 = 100% Capacity ratio: = (1,300 / 1,200) × 100 = 108.3% Production volume ratio: = (1,300 / 1,200) × 100 = 108.3% Interpretation: The workforce exactly met the standard in productivity, but worked more hours than budgeted, giving a higher overall output (volume ratio).

Interpreting Results

- Above 100%: Indicates performance exceeded standard or plan.

- Below 100%: Indicates performance fell short—may be due to inefficiency, lost hours, or insufficient workload.

It is important to review the causes. A low efficiency ratio, for example, might mean extra time spent due to poor training, equipment issues, or substandard materials.

Key Term: Idle time

Periods in which employees are paid but not producing output (e.g., due to breakdowns or waiting for materials). Idle time is not included in standard hours for actual output.

Practical Application and Caveats

Labour ratios support both operational and strategic control. However, their usefulness depends on an accurate and realistic standard being set. If the standard is out of date or does not reflect attainable conditions, ratios may mislead. Non-productive hours (such as training or unplanned downtime) should be accounted for separately.

Worked Example 1.2

A manufacturer sets a budget for 1,500 productive hours in a month. Actual hours worked were 1,400, of which 60 hours were idle due to machine maintenance. Standard hours for the actual output achieved were 1,320.

Required: Calculate the efficiency, capacity, and production volume ratios.

Answer:

Standard hours for actual output = 1,320 Actual hours worked = 1,400 Budgeted hours = 1,500 Efficiency ratio: = (1,320 / 1,400) × 100 = 94.3% Capacity ratio: = (1,400 / 1,500) × 100 = 93.3% Production volume ratio: = (1,320 / 1,500) × 100 = 88% Commentary: Both underutilised capacity and reduced efficiency contributed to a significantly reduced volume ratio.Revision Tip: Labour ratios frequently appear in questions on responsibility accounting, variance analysis, or standard costing. Practise calculating all three together, and remember their mathematical link.

Common Exam Pitfalls

Exam Warning: Do not confuse "standard hours for actual output" with "actual hours worked." Always base the efficiency ratio on the time that should have been used for the actual output, not the hours actually worked.

If the standard time per unit is not given, calculate standard hours by multiplying actual output by the standard hours per unit.

Summary

Labour efficiency, capacity, and production volume ratios are essential management tools for monitoring hours worked, workforce efficiency, and alignment with operational plans. By comparing standards with actuals, these ratios reveal the effectiveness of labour resource usage, identify reasons for variances, and guide corrective management action.

Key Point Checklist

This article has covered the following key knowledge points:

- The role of labour ratios in management accounting and standard costing

- Calculation and interpretation of the labour efficiency ratio

- Calculation and interpretation of the labour capacity ratio

- Calculation and interpretation of the labour production volume (activity) ratio

- The mathematical connection between all three ratios

- The importance of using correct and realistic standards

- Application of labour ratios in performance assessment and variance analysis

Key Terms and Concepts

- Labour efficiency ratio

- Labour capacity ratio

- Labour production volume ratio

- Standard hours for actual output

- Idle time