Learning Outcomes

By the end of this article, you will be able to explain how inventory is valued using FIFO, LIFO, and AVCO methods. You will understand the principles, advantages, and disadvantages of each approach, perform calculations to determine material issues and inventory balances, and recognise the impact on profits and financial statements. This will support your ability to select and apply appropriate valuation methods for ACCA exam scenarios.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand how inventory values affect reported profits, decision making, and accounting controls. In particular, focus your revision on the following syllabus points:

- The principles and objectives of materials and inventory control in manufacturing and service environments

- Valuation of material issues and closing inventory under FIFO, LIFO, and AVCO methods

- The impact of inventory valuation methods on reported profits and inventory values

- Benefits and limitations of different inventory valuation systems

- Preparation and interpretation of inventory records, including stores ledger accounts

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- State the main principle of FIFO inventory valuation.

- A company purchased 100 units at $5, then 200 units at $6. If 150 units are issued, what is the value of the issue under LIFO?

- Which inventory valuation method averages costs after every purchase?

- True or false: LIFO is acceptable under IAS 2 for published financial statements.

Introduction

Inventory valuation is a core area of materials and inventory control. The method chosen to value materials issued and closing inventory has a direct effect on cost calculations, profit measurement, and financial position. Accurate and consistent valuation is needed for both internal management decisions and external financial reporting.

Key Term: inventory valuation

The method used to assign monetary values to material issues and closing inventories, affecting cost records and financial statements.

Methods of Inventory Valuation

There are three main methods for valuing material issues and closing inventory:

FIFO (First-In, First-Out)

FIFO assumes materials are issued in the order in which they arrive. The earliest costs are assigned to goods issued first.

Key Term: FIFO

A method where materials received earliest are considered issued first; closing inventory consists of the most recent purchases.

LIFO (Last-In, First-Out)

LIFO assumes the most recently purchased materials are issued first. The latest costs appear in issues, and older costs remain in closing inventory.

Key Term: LIFO

A method where the most recent purchases are issued first; closing inventory represents the oldest costs.

AVCO (Average Cost / Weighted Average Cost)

AVCO calculates a new average unit cost after every purchase, based on total cost divided by total units. Both issues and closing inventory are valued at the latest average cost.

Key Term: AVCO

A method where materials issues and closing inventory are valued at the weighted average cost per unit after each purchase.

The Stores Ledger Account

All inventory records use a stores ledger to monitor receipts, issues, and balances.

| Date | Receipts | Issues | Balance |

|---|---|---|---|

| 1 Jan | 100 @ $5 | 100 @ $5 | |

| 5 Jan | 200 @ $6 | 100 @ $5, 200 @ $6 |

Each inventory valuation method applies different rules for updating these records.

Worked Example 1.1

Worked Example 1.1 Details

A business has the following material transactions:

- 1 March: Opening balance – 100 units @ $2.00

- 2 March: Purchase – 70 units @ $2.20

- 3 March: Issue – 40 units

- 4 March: Purchase – 50 units @ $2.30

- 5 March: Issue – 70 units

Required: Determine the value of issues and closing inventory under FIFO, LIFO, and AVCO.

Answer:

- FIFO:

- Issues: 40 units @ $2.00 (3 Mar), 70 units = 60 @ $2.20 + 10 @ $2.00 (5 Mar)

- Closing Inventory: Combine most recent purchases.

- LIFO:

- Issues: 40 units @ $2.20 (3 Mar), 70 units = 50 @ $2.30 + 20 @ $2.20 (5 Mar)

- Closing Inventory: Consists of oldest units.

- AVCO:

- After every receipt, calculate new average cost. Issues and closing inventory are at latest average.

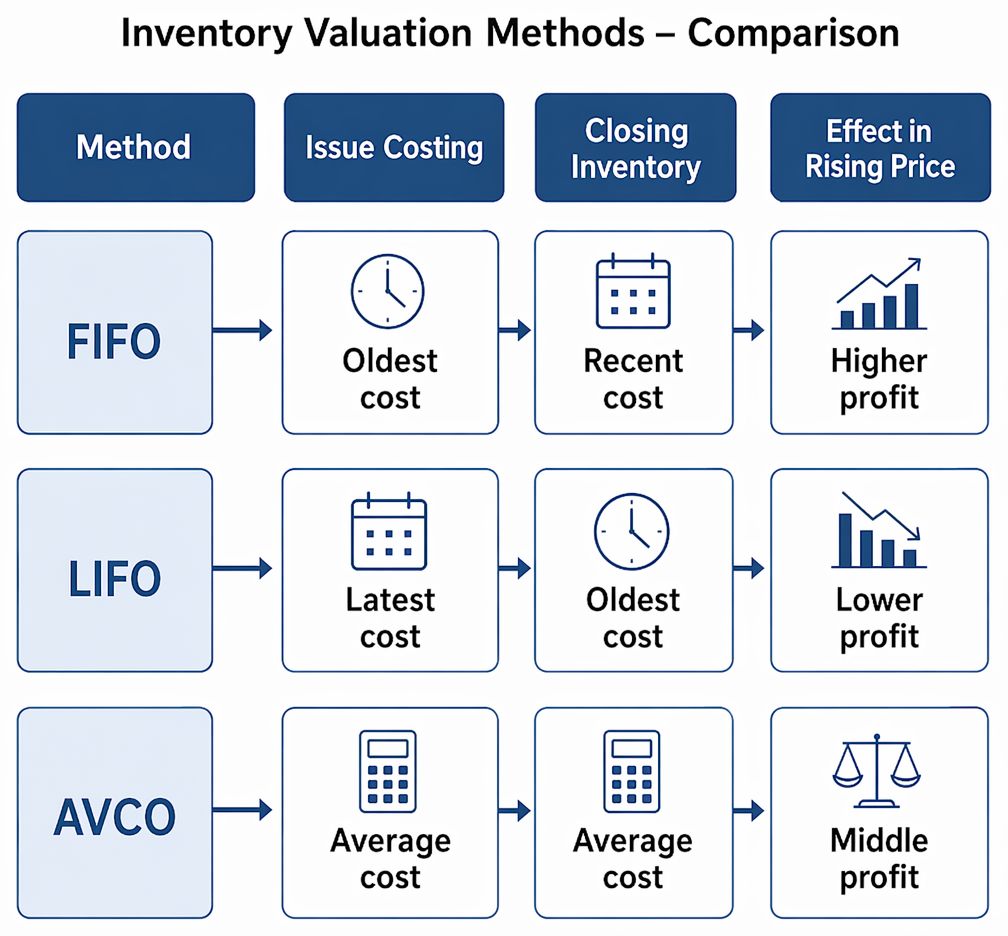

Comparison Table

Inventory valuation decision rules map reporting context and costing objectives to FIFO, LIFO, or AVCO, with LIFO excluded from external reporting.

| Method | Issue Costing | Closing Inventory | Effect in Rising Price |

|---|---|---|---|

| FIFO | Oldest cost | Recent cost | Higher profit |

| LIFO | Latest cost | Oldest cost | Lower profit |

| AVCO | Average cost | Average cost | Middle profit |

Worked Example 1.2

A company bought 200 units at $8 each and 400 units at $9 each. If 300 units are issued, calculate the value of issues and closing balance under AVCO.

Answer:

Total units after both purchases = 600 units; total cost = (200 × 8) + (400 × 9) = $1,600 + $3,600 = $5,200 Average cost = $5,200 / 600 = $8.67 per unit Issues: 300 units × $8.67 = $2,601 Closing inventory: 300 units × $8.67 = $2,601

Advantages and Disadvantages

FIFO

Advantages:

- Closing inventory reflects current prices.

- Logical and widely understood.

Disadvantages:

- Not realistic if usage order differs from receipt.

- In periods of rising prices, increases profit (higher tax).

LIFO

Advantages:

- Issue prices are up to date.

- In rising prices, lowers profit (lower tax).

Disadvantages:

- Closing inventory is at outdated costs.

- Not permitted under IAS 2 for external reporting.

AVCO

Advantages:

- Smooths out price fluctuations.

- Accepted by accounting standards.

Disadvantages:

- Issue price may never match actual purchase price.

- Can be complex if frequent receipts.

Exam Warning: LIFO is not permitted for published financial statements under International Accounting Standard IAS 2, but may be used in internal reporting or management accounts. Always check the exam scenario for context.

The Effect on Profit and Inventory Values

The inventory valuation method affects cost of goods sold and closing inventory. In periods of rising prices:

- FIFO leads to lower cost of goods sold and higher profit; closing inventory is higher.

- LIFO results in higher cost of goods sold and lower profit; closing inventory is lower.

- AVCO produces values between FIFO and LIFO.

Accounting and Control

Inventory records should be updated accurately and regularly, matching the chosen valuation method. Physical counts must support book records to ensure control and detect discrepancies.

Key Term: stores ledger

A record showing quantities and values of materials received, issued, and remaining in inventory, maintained using the chosen valuation method.

Common Errors

- Failing to update averages after every receipt (AVCO)

- Using LIFO for financial reporting (not allowed under IAS 2)

- Mixing methods within the same period

Revision Tip: Always recalculate the average cost after every purchase under AVCO. Do not average over the whole period unless specified.

Summary

Inventory valuation methods determine how material issues and closing inventories are costed. This directly affects reported profits and stock values. FIFO uses earliest costs, LIFO uses latest costs, and AVCO averages costs. The choice of method impacts profit, taxes, and decision making, especially when prices change.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the purpose and importance of inventory valuation methods

- Apply FIFO, LIFO, and AVCO to calculate material issues and closing inventory

- Distinguish the impact of each method on profits and reporting

- Identify advantages and disadvantages of each approach

- Recognise common errors in applying inventory valuation methods

Key Terms and Concepts

- inventory valuation

- FIFO

- LIFO

- AVCO

- stores ledger