Learning Outcomes

After reading this article, you will be able to explain why organisations use budgets, identify different types of budgets, and clarify their core functions in planning, control, coordination, and communication. You will understand how budgets align business activities, support management decision-making, and ensure departments work towards common objectives. You should be able to distinguish between principal budget types, explain the stages in the budgeting process, and recognise the behaviourally important aspects of budgeting for the ACCA exam.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand budgeting's functions and its role in managing organisational performance. Key syllabus areas relating to this article include:

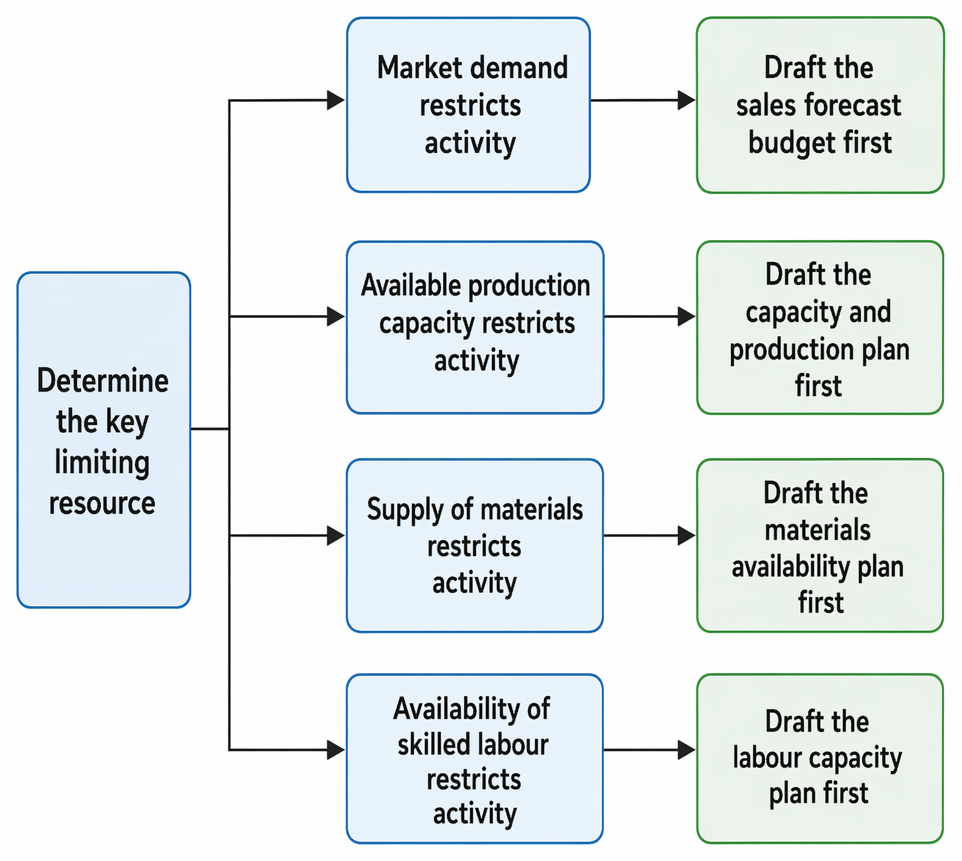

Binding constraints determine whether budgeting begins with the sales budget, capacity and production budget, materials availability budget, or labour capacity budget.

- The purpose of budgeting and why organisations implement budgets

- The planning and control cycle and the connection between strategic objectives and budgets

- Types of budgets: functional budgets, consolidated budgets, fixed and flexible budgets

- The roles of budgeting in coordination and communication

- How budgets motivate and authorise, including behavioural implications

- Responsibility accounting and identification of controllable costs

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which function of budgeting is served when a company sets annual targets and measures performance against them?

- a) Coordination

- b) Control

- c) Motivation

- d) Delegation

-

Identify two main differences between a fixed budget and a flexible budget.

-

Briefly explain what is meant by the "principal budget factor" in budgeting.

-

List one way in which budgeting contributes to effective communication within an organisation.

Introduction

Budgets are a critical tool for effective management. They are formal plans, usually stated in monetary terms, that set out an organisation’s intentions for a future period. Budgets help to translate strategy into actionable plans, ensure resources are allocated efficiently, provide a basis for evaluating performance, and support clear communication across functions.

Management relies on budgets for more than just cost control. Budgets help departments align their activities, define responsibilities, guide decision-making, and provide motivation. Understanding how various types of budgets serve the functions of planning, control, coordination, and communication is central to ACCA success.

Key Term: budget

A quantified financial plan for a defined period, showing expected income, expenditure, and resource allocation to achieve organisational objectives.Test Tip: When revising Planning, control, coordination, and communication, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

THE PURPOSE OF BUDGETS

Budgets offer several well-established benefits within organisations. Their main purposes can be grouped into four core functions:

Planning

Budgets support planning by forcing managers to think systematically about future objectives, required resources, and anticipated obstacles. The process of preparing a budget requires assessing the feasibility of plans and selecting actions that align with company objectives.

Control

Once plans are established, budgets become the yardstick for monitoring performance. Actual results can be compared with the original plan (budget) to identify significant differences, or variances. This enables timely corrective action and future improvements.

Coordination

Budgeting compels different departments and functions within an organisation to work together. For example, the production department must align its output with the sales department's forecasts, and both must consider the procurement of materials and resources. This alignment supports a unified approach to achieving company goals.

Communication

Budgets communicate management’s expectations to staff across the business. Clear budget documents make targets explicit and provide a basis for shared understanding—helping to avoid confusion and misaligned priorities.

Key Term: principal budget factor

The constraint or resource that is most likely to limit the activities of an organisation during the budgeting period. It determines the sequence for preparing functional budgets.

TYPES OF BUDGETS

Organisations use different types of budgets, each with a specific role in the management cycle.

Functional Budgets

Functional budgets are prepared for individual business functions or departments. Common examples include:

- Sales budget

- Production budget

- Materials usage budget

- Labour budget

- Overheads budget

- Marketing or distribution budget

Each functional budget details expected activity levels, resources needed, and associated costs or revenues.

Comprehensive Budget

The comprehensive budget brings together all functional budgets into overarching statements, typically as:

- The budgeted statement of profit or loss

- The budgeted statement of financial position (balance sheet)

- The budgeted cash flow statement

The comprehensive budget gives the overall financial picture for the organisation and summarises planned operations.

Key Term: comprehensive budget

The summary budget incorporating all functional budgets, resulting in budgeted financial statements for the business as a whole.

Fixed and Flexible Budgets

- Fixed budget: Prepared for a single, predetermined level of activity and does not change, regardless of what level of activity actually occurs.

- Flexible budget: Adjusts budgeted amounts according to the actual level of activity, recognising variable and fixed cost behaviour.

Key Term: fixed budget

A budget set for one activity level that remains unchanged irrespective of actual output achieved. Key Term: flexible budget

A budget designed to change with changes in activity, reflecting variable and fixed cost patterns.

Principal Budget Factor

Budget preparation starts with the function where constraints are most binding (the principal budget factor). Often, this is sales demand, but it could be production capacity, material supply, or skilled labour availability.

Worked Example 1.1

Question: A clothing manufacturer has limited sewing machine capacity next year due to delayed equipment deliveries, but strong market demand. What is the principal budget factor, and which budget should be prepared first?

Answer:

The scarce sewing machine capacity is the principal budget factor, so the production capacity (number of machine hours available) should be budgeted before others.

THE BUDGETING PROCESS

The budgeting process typically follows these steps:

- Identify organisational objectives and long-term plans.

- Determine the principal budget factor.

- Prepare the budget for the limiting factor.

- Prepare remaining functional budgets in logical sequence.

- Aggregate to form the consolidated budget.

- Obtain review and approval by senior management or budget committee.

- Implement budgets and monitor actual results against them.

Source of Data: Budget preparation draws on a range of internal (historical data, forecasts, departmental input) and external data (market analysis, supplier quotations, economic indicators).

Key Term: budget committee

A group of senior managers responsible for overseeing, reviewing, and approving the budget process and final budgets. Key Term: budget manual

A document setting out budget policies, procedures, responsibilities, and schedules within an organisation.

Worked Example 1.2

Question: During the annual planning cycle, the purchasing manager must estimate raw material requirements based on forecasted production. Which budget links these two processes, and what coordination does it encourage?

Answer:

The materials usage budget integrates the production and purchasing functions, ensuring material requirements match planned output—coordinating procurement with production needs.

BUDGETS AS CONTROL TOOLS

Budgets are central to management control. By comparing actual results with budgets, managers can quickly identify deviations and take corrective action. Regular budget monitoring allows for prompt identification of:

- Cost overruns

- Revenue shortfalls

- Resource shortages

If results differ materially from the budget, variance analysis is performed to investigate causes.

Key Term: variance

The difference between budgeted and actual figures for income, expenditure, or resource usage. Key Term: goal congruence

The alignment of individual, departmental, and organisational objectives, so that all parties are working towards the same outcomes.

BUDGETS FOR COORDINATION AND COMMUNICATION

Budgets play a direct role in unifying departments and clarifying expectations.

- Coordination: Requiring departments to agree on interdependent targets (e.g., sales, production, purchasing) reduces conflicts and synchronises activities.

- Communication: Making all parties aware of organisational priorities, constraints, and performance targets ensures consistency and reduces misunderstandings.

BEHAVIOURAL AND MOTIVATIONAL ASPECTS

Budgets do not only set numbers—they influence how individuals behave. Participation in the budgeting process can boost motivation, leading to higher commitment and better performance (“goal congruence”).

However, imposed budgets (set only by senior management) may breed resentment or passive resistance if managers see targets as unrealistic or unfair.

Exam Warning: Budget targets should be both challenging and achievable. Unreasonable or imposed budgets can demotivate staff and reduce performance.

AUTHORITY, RESPONSIBILITY, AND CONTROL

Budgets assign authority and responsibility for resource use.

- Authorisation: Budget approval signals that planned expenditure is authorised, providing spending limits and guidance.

- Responsibility: Budget holders are accountable for achieving targets and controlling costs within their remit.

SUMMARY TABLE: Types of Budgets and Their Functions

| Budget Type | Function | Typical User |

|---|---|---|

| Sales Budget | Planning, Coordination | Sales, Planning Managers |

| Production Budget | Planning, Resource Allocation | Operations Managers |

| Materials Budget | Planning, Control, Coordination | Purchasing Managers |

| Labour Budget | Planning, Control | HR, Production Managers |

| Overheads Budget | Cost Control, Planning | Department Managers |

| Cash Budget | Liquidity Management, Control | Finance Managers |

| Consolidated Budget | Aggregation, Overall Planning | Senior Management |

Key Point Checklist

This article has covered the following key knowledge points:

- The main purposes of budgeting: planning, control, coordination, communication

- Types of budgets: functional, consolidated, fixed, flexible

- The principal budget factor and its impact on the budget sequence

- The budget preparation process and coordination between functions

- The importance of communication and motivation in budgeting

- The control function of budgets, variance analysis, and authorisation

- Authority and responsibility assigned through budget holding

Key Terms and Concepts

- budget

- principal budget factor

- comprehensive budget

- fixed budget

- flexible budget

- budget committee

- budget manual

- variance

- goal congruence