Learning Outcomes

After reading this article, you will be able to calculate expected values and interpret them for decision making within business contexts. You will understand key probability principles, evaluate outcomes using probability-weighted averages, and recognise the practical uses and limitations of expected values. This knowledge will support you in applying quantitative tools to real-world decision-making scenarios common on the ACCA exam.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand how expected values underpin decision making using probability in management accounting. Focus your revision on:

- Explaining basic concepts of probability and probability distributions

- Calculating expected values (EV) and interpreting their meaning in a business context

- Applying expected values to decisions under uncertainty

- Evaluating the benefits and limitations of EV as a decision tool

- Recognising the significance of probability estimates and risk in outcome forecasting

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What does the 'expected value' represent in probability terms for a business decision?

- If a project has profit outcomes of $2,000 (P=0.4), $1,000 (P=0.5), and -$500 (P=0.1), calculate its expected value.

- State one scenario where using expected value may give misleading guidance to management.

- How does the probability of each possible outcome influence the expected value calculation?

Introduction

ACCA candidates frequently face choices under uncertainty – from sales forecasts to project investments. Decision making in such situations often depends on evaluating possible outcomes and their likelihood. Expected value (EV) is a central concept that summarises uncertain prospects as a single weighted average, directly supporting rational decision making. However, while the EV provides useful guidance, it cannot replace judgement or account for all risks. This article explains how to calculate, interpret, and use expected values correctly, highlighting potential pitfalls to avoid in real-world use.

Probability and Expected Value Concepts

Understanding probability is essential when dealing with uncertainty. A probability quantifies the chance of an event occurring and always lies between 0 (impossible) and 1 (certain). When there are several possible outcomes, each is assigned a probability, and together these probabilities must sum to 1.

Key Term: probability

A numerical measure between 0 and 1 representing the likelihood of a given event occurring. Key Term: expected value (EV)

The sum of all possible outcomes, each multiplied by its probability; a probability-weighted average result of a decision or process.

Calculating Expected Value

The EV is calculated using the formula:

Where:

- is the probability of outcome

- is the value (profit, cost, etc.) of outcome

The EV provides the long-run average result if a decision is repeated many times.

Test Tip: In EV calculations, check that the probabilities for all outcomes sum to 1 before multiplying each outcome by its probability and adding the results.

Worked Example 1.1

A business faces three possible sales outcomes for a new product next month:

- Outcome A: $10,000 profit, probability 0.2

- Outcome B: $6,000 profit, probability 0.5

- Outcome C: $2,000 profit, probability 0.3

What is the expected value of profit?

Answer:

Business Relevance

The EV approach is often used for:

- Forecasting average profits or costs from uncertain events

- Comparing mutually exclusive projects or alternatives

- Stock-level or pricing decisions when demand is variable

Interpretation of Expected Value

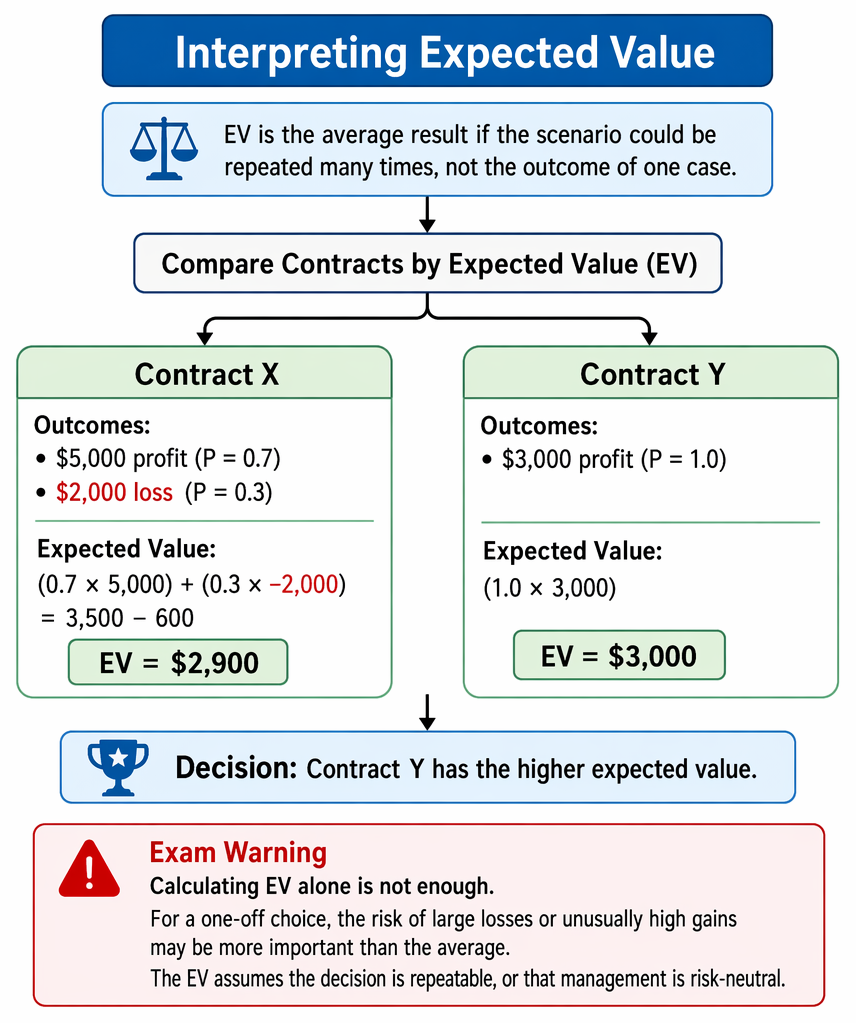

The EV does not predict what will happen in any single case; it represents the average result if the scenario could be repeated many times. For one-off, high-stake decisions, actual outcomes may differ widely from the expected value.

Expected value is presented through probability-weighted calculation, long-run interpretation, business uses, and constraints relating to risk attitude and one-off decisions.

Worked Example 1.2

A company can accept one of two contracts:

- Contract X: $5,000 profit (P=0.7), or a $2,000 loss (P=0.3)

- Contract Y: $3,000 profit (P=1.0)

Which contract has the higher expected value?

Answer:

Contract X: (0.7 × 5,000) + (0.3 × -2,000) = 3,500 - 600 = $2,900 Contract Y: (1.0 × 3,000) = $3,000 Contract Y has the higher expected value.Exam Warning: Calculating EV alone is not enough. For a one-off choice, the risk of large losses or unusually high gains may be more important than the average.

Application in Decision Making

Expected value helps management compare alternative actions where outcomes are uncertain.

Example uses include:

- Deciding how many units to produce or order when demand is uncertain

- Choosing between investment projects with different risk profiles

- Setting sales quotas or incentive payments

Limitations of Expected Value

While useful, EV has significant limitations:

- If outcomes are extreme or probabilities are unreliable, the average may not reflect the practical risk faced.

- EV ignores how comfortable management is with risk (risk attitude).

- In single-instance ('one shot') decisions, the actual gain/loss will likely not match the EV.

Key Term: risk attitude

The degree of comfort management has with uncertain outcomes, including the possibility of losses or unusually variable results.

Worked Example 1.3

A construction firm can bid on a contract:

- Win: Profit $100,000 (P=0.2)

- Lose: Loss $10,000 (P=0.8, representing bid preparation cost)

Expected Value? Should they proceed?

Answer:

The average EV is positive, but there is an 80% chance of losing $10,000. Management's risk appetite determines if they proceed.

Test Tip: Use the EV to compare options, but also consider the spread and probabilities, especially if extreme outcomes are possible.

Summary

The expected value method summarises a range of possible business outcomes into a single number, weighted by probability. It is an efficient method for comparing alternatives in repetitive or risk-neutral decisions. However, the method cannot reflect risk aversion, probability estimation errors, or the implications of rare but high-impact events. Judgement and risk awareness remain essential complements to quantitative EV analysis in business decision making.

Key Point Checklist

This article has covered the following key knowledge points:

- Understanding of probability and its business use

- Calculation of expected value (EV) and interpretation

- Use of EV in business decision making

- Comparison of alternatives using EV

- Practical limitations of the expected value approach

- Importance of considering risk and probability accuracy

Key Terms and Concepts

- probability

- expected value (EV)

- risk attitude