Learning Outcomes

After reading this article, you will be able to categorize costs as direct or indirect, explain the difference between product and period costs, and describe cost behaviour for management accounting and decision-making. You will be able to apply these distinctions to cost calculations and explain their significance in budgeting and performance management within the ACCA PM syllabus.

ACCA Performance Management (PM) Syllabus

For ACCA Performance Management (PM), you are required to understand how costs are classified and how cost behaviour impacts planning and control. An accurate distinction between types of costs is essential for correct cost accumulation, budgeting, and performance evaluation. In particular, this article will help your revision for:

- Distinguishing between direct and indirect costs (cost objects, cost centres, responsibility centres)

- Identifying and explaining product and period costs

- Explaining cost behaviour: variable, fixed, semi-variable, stepped

- Applying cost classification to costing, inventory valuation, and budgeting

- Explaining the importance of correct cost classification in performance analysis

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is an example of an indirect cost for a car manufacturing cost centre?

- a) Engine assembly wages

- b) Steel used for chassis

- c) Factory rent

- d) Tyres fitted to each car

-

True or false? A period cost is never included in inventory valuation under absorption costing.

-

Which TWO of the following are usually classified as product costs in a manufacturing business?

- Depreciation of production equipment

- Factory supervisor salary

- Sales manager commission

- Office utilities

-

Briefly define a direct cost and an indirect cost in one sentence each.

Introduction

Management accounting relies on accurate cost classification to support budgeting, costing, and decision-making. Knowing whether a cost is direct or indirect, or whether it relates to a product or a specific period, is fundamental to performance management and control. Understanding cost behaviour—how costs change as output changes—is also critical for effective planning.

This article sets out the key classifications of costs: direct versus indirect, product versus period, and reviews how cost behaviour underpins control, decision-making, and budgeting in performance management.

Key Term: direct cost

A cost that can be identified specifically and exclusively with a particular cost object, such as a product, service, cost centre, or project. Key Term: indirect cost

A cost that cannot be traced in full to a particular cost object and instead supports multiple cost objects, requiring allocation or apportionment.Test Tip: When revising Direct vs indirect and product vs period costs, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

DIRECT AND INDIRECT COSTS

Overview

Costs are first classified according to whether they can be directly attributed to a unit of output, department, or project (cost object).

Direct Costs

These are costs that can be measured and assigned to a single cost object in an economically feasible way.

-

Examples: raw materials for a unit, assembly line labour for a batch, or a sales commission paid for a specific contract

-

In production: direct materials, direct labour, and, where relevant, direct expenses form the "prime cost"

Key Term: prime cost

The sum of all direct costs (direct materials, direct labour, and direct expenses) involved in manufacturing a product.

Indirect Costs

Indirect costs support more than one cost object simultaneously and require methods of indirect assignment (allocation, apportionment, absorption). These are also termed "overheads"

-

Examples: factory rent, equipment depreciation, utilities, and indirect staff (e.g., supervisors)

-

Indirect costs are pooled and then shared between cost objects using appropriate bases (e.g., machine hours, labour hours)

Key Term: overhead

All manufacturing costs other than direct materials, direct labour, and direct expenses; synonymous with indirect costs in many contexts.

Worked Example 1.1

A company manufactures tables. It uses £10 of pine wood per table, spends £4 per table on assembler wages, and pays £150,000 per year for the production manager's salary and factory rent.

Classify each cost as direct or indirect in relation to producing one table.

Answer:

- Pine wood per table: Direct cost (can be traced to each table)

- Assembler wages per table: Direct cost (can be traced to each table)

- Production manager's salary: Indirect cost (supports all tables, not one)

- Factory rent: Indirect cost (required for the entire output, not one table)

Why the distinction matters

The direct/indirect classification is essential for:

- Inventory valuation (which costs go into product cost)

- Setting selling prices

- Performance assessment (who controls the costs)

- Determining responsibility within the organisation

PRODUCT COSTS AND PERIOD COSTS

Costs can also be classified by the time-period to which they relate, and whether they are included in inventory values or expensed immediately.

Key Term: product cost

A cost assigned to goods that are either purchased or manufactured for resale; included in inventory values and expensed as cost of sales when the product is sold. Key Term: period cost

A cost that is charged as an expense in the period in which it is incurred; not included in inventory values.

Product Costs

These comprise all costs involved in acquiring or making a product. In manufacturing, this includes:

- Direct materials

- Direct labour

- Manufacturing overhead (indirect production costs)

Under absorption costing, all these costs are included in inventory until the product is sold.

Non-manufacturing costs (e.g., admin, distribution, selling) are not included as product costs.

Period Costs

All non-product costs are usually period costs. These are expensed in the period in which they are incurred and do not appear in inventory valuation. Examples include:

- Selling and distribution costs

- Head office salaries

- Administration expenses

- Marketing costs

Worked Example 1.2

A manufacturer incurs the following monthly costs:

- Direct materials: £20,000

- Factory rent: £5,000

- Depreciation of delivery vans: £1,200

- Office stationery: £800

Classify each cost as a product cost or a period cost under absorption costing.

Answer:

- Direct materials: Product cost (part of inventory until sold)

- Factory rent: Product cost (is a manufacturing overhead)

- Depreciation of delivery vans: Period cost (distribution, not production)

- Office stationery: Period cost (administration)

Importance of the Classification

The product/period distinction is significant because:

- Inventory valuation (financial statements): Only product costs are included in inventory values

- Profit measurement: Period costs are charged to profit in the period incurred, product costs are matched to revenue when the inventory is sold

- Decision-making: Affects cost-based pricing, make-or-buy decisions, and performance appraisal

Revision Tip: Remember: Only production costs go into the value of inventory. All non-production costs are treated as period costs and expensed straight away.

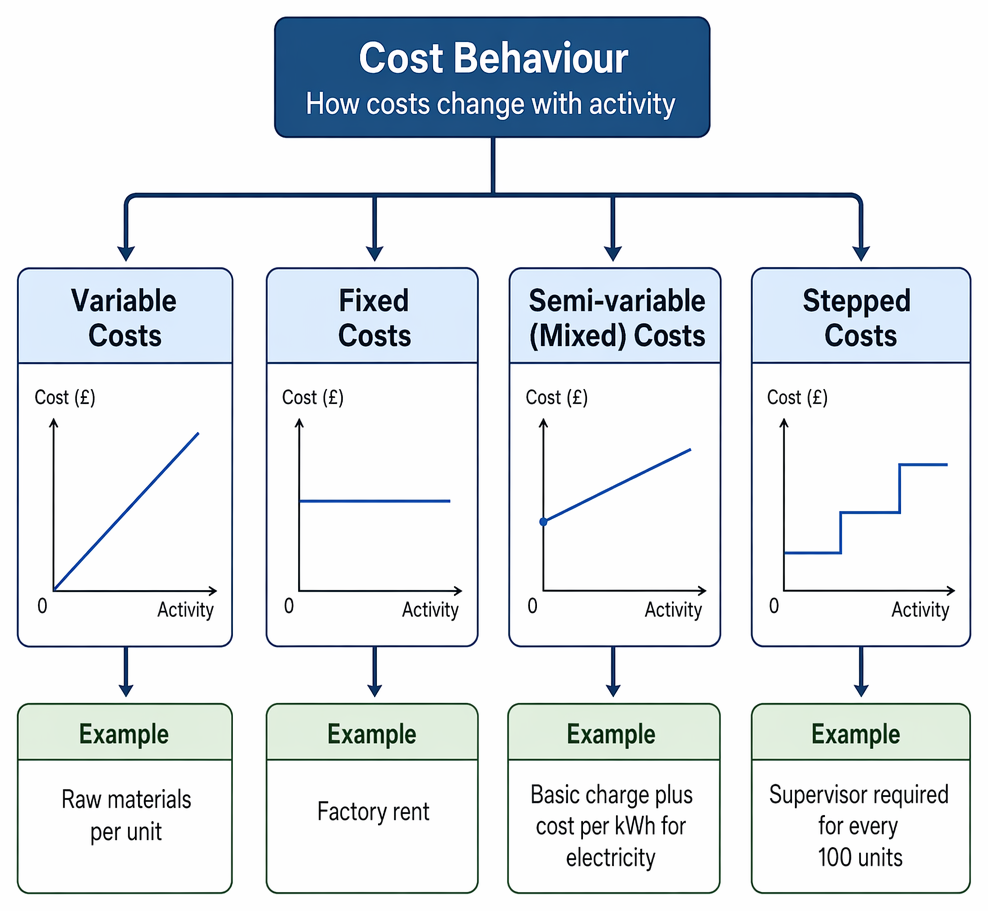

COST BEHAVIOUR: VARIABLE, FIXED, SEMI-VARIABLE, STEPPED

A further essential cost distinction is by behaviour—how costs change with the volume of activity. This directly affects decision-making, forecasting, and control.

Indirect production overheads are pooled, allocated, reapportioned, and absorbed to products using an absorption base before under- or over-absorption analysis.

- Variable costs: Change in direct proportion to activity (e.g., raw materials per unit)

- Fixed costs: Remain constant over a relevant range, regardless of output (e.g., factory rent)

- Semi-variable (mixed) costs: Have both variable and fixed components (e.g., basic charge plus cost per kWh for electricity)

- Stepped costs: Remain fixed over a certain range of activity, then increase in a stepwise fashion (e.g., supervisor required for every 100 units)

Correctly identifying cost behaviour aids in budgeting, calculation of breakeven, and resource planning.

Worked Example 1.3

A call centre pays £2,000 per month rent (fixed) and £1.50 per call handled (variable). In January, they handled 5,000 calls.

What is the total cost, and how would you describe it?

Answer:

Fixed cost: £2,000 Variable cost: 5,000 calls × £1.50 = £7,500 Total cost: £9,500 This is a mixed (semi-variable) cost structure.

Summary

Correct cost classification underpins reliable costing information, budgeting, and control. Direct costs are directly attributable to a product, service, or project; indirect costs benefit more than one cost object. Product costs are attached to inventory until sale, while period costs are expensed when incurred. Understanding cost behaviour enables effective decision-making and performance evaluation.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish between direct costs (traced to a single cost object) and indirect costs (shared, allocated, or apportioned)

- Understand the distinction between product costs (included in inventory) and period costs (expensed in the period)

- Identify examples of each cost category in manufacturing and service environments

- Explain the importance of correct cost classification for inventory valuation, budgeting, and performance assessment

- Recognise cost behaviour types and their relevance in forecasting and decision-making

Key Terms and Concepts

- direct cost

- indirect cost

- prime cost

- overhead

- product cost

- period cost