Learning Outcomes

After reading this article, you will be able to apply your understanding of fixed, variable, semi-variable, and stepped costs to cost-volume-profit (CVP) analysis, breakeven calculations, and management decision-making scenarios. You will analyse how cost behaviour impacts contribution margins, margin of safety, and target profit calculations. This article builds on foundational cost classification knowledge and focuses on the practical application of cost behaviour in performance management contexts.

ACCA Performance Management (PM) Syllabus

For ACCA Performance Management (PM), you are required to understand how costs behave and how they are classified. This is a recurring theme throughout cost accounting topics and is core to scenario-based and computational questions. Specifically, you must be confident with:

- The definition and identification of fixed, variable, semi-variable (mixed), and stepped costs

- How to analyse cost behaviour for planning, budgeting, and control purposes

- The impact of cost behaviour on breakeven analysis and forecasting

- The use of techniques (such as the high-low method) to separate mixed costs into fixed and variable components

- Recognising how cost behaviour influences management decisions, variance analysis, and performance management

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which one of the following best describes a 'fixed cost'?

- a) Varies directly with output

- b) Changes with activity in steps

- c) Remains the same within a relevant range, regardless of activity

- d) Is only incurred if there is production

-

A utility bill comprises a monthly standing charge and a variable charge per unit consumed. What type of cost is this?

- a) Fixed cost

- b) Variable cost

- c) Stepped cost

- d) Semi-variable cost

-

Explain in one sentence the key difference between a stepped cost and a fixed cost.

-

You are given monthly data for total maintenance cost and machine hours over six months. Which technique could you use to find the variable and fixed elements of cost?

Introduction

Effective cost management relies on understanding how costs respond as activity changes. Proper classification of costs as fixed, variable, semi-variable, or stepped is fundamental in budgeting, planning, cost-volume-profit analysis, and performance evaluation for ACCA PM. Spotting these behaviours in scenarios is essential for scoring marks in both computational and written questions.

Key Term: fixed cost

A cost that does not change in total over a defined range of activity in the short term, regardless of the actual output level. Key Term: variable cost

A cost that varies in total in direct proportion to changes in activity or production volume, but remains constant per unit. Key Term: semi-variable (mixed) cost

A cost with both fixed and variable components, so total cost varies with activity, but not in direct proportion. Key Term: stepped cost

A cost that remains fixed over small ranges of activity but increases by discrete amounts at certain thresholds of activity.

Cost Classification for Decision-Making

Costs are classified by their behaviour because management decisions, budgets, forecasts, and control processes depend on how costs are likely to move with changes in activity. Misunderstanding cost behaviour can result in forecasting errors and poor decisions.

High-low cost decomposition shows the sequence from selecting extreme activity levels to deriving fixed cost, variable rate, and a cost equation.

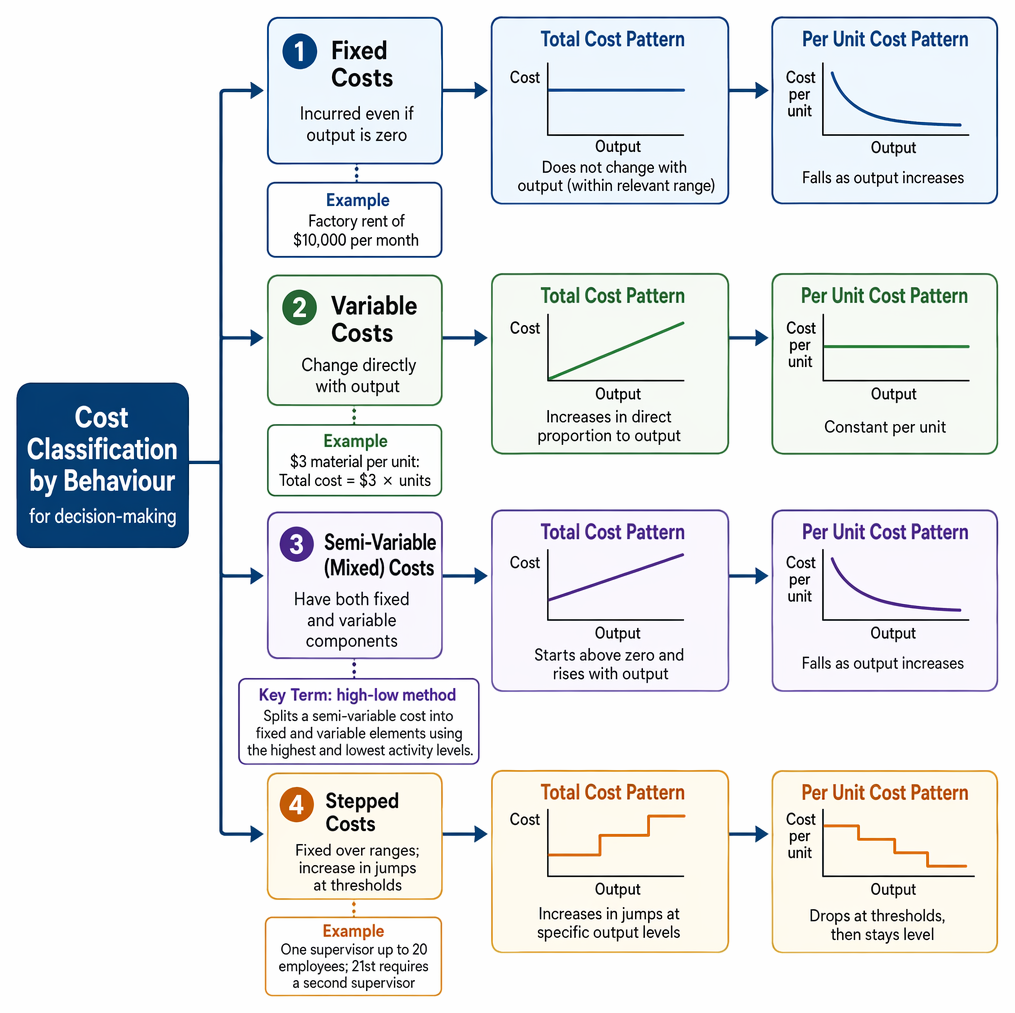

Fixed Costs

Fixed costs, such as rent, salaries, or depreciation, are incurred even if output is zero. They do not change in total as production rises within a relevant range (such as factory physical capacity). However, the fixed cost per unit will fall as output increases:

- Example: A factory's rent of $10,000 per month is fixed whether 1 or 1,000 units are produced.

Variable Costs

Variable costs, such as raw materials or direct labour (in piecework systems), change directly with output. They are constant on a per unit basis:

- Example: If each product uses $3 of material, total material cost will be $3 × number of units produced.

Semi-Variable (Mixed) Costs

Some costs have both a fixed and a variable component. For instance, a mobile phone contract might have a fixed line rental plus a charge per minute used. In cost analysis, these need to be split into their fixed and variable parts.

Key Term: high-low method

A technique for analysing and splitting a semi-variable cost into fixed and variable elements using the highest and lowest activity levels.

Stepped Costs

Stepped (or step-fixed) costs are fixed over certain activity intervals, but increase in jumps when output reaches specific thresholds, often due to limits on existing capacity (such as extra supervisors or machinery).

- Example: One supervisor can monitor up to 20 employees; hiring the 21st employee requires a second supervisor, doubling supervisor costs instantly.

Recognising Cost Behaviour in Practice

Correctly classifying costs when presented with a scenario is essential to prevent errors in decision-making models, budgeting, and variance analysis.

Worked Example 1.1

A manufacturing business pays a monthly electricity bill that includes a $600 standing (fixed) charge and $0.08 for every kWh of electricity used.

Question: Classify this cost and state how it would behave as output rises.

Answer:

This is a semi-variable (mixed) cost, consisting of a fixed part ($600 per month) and a variable part ($0.08 per kWh). The total electricity cost will rise as output increases, but the increase will not be strictly proportional to output unless electricity usage per unit stays constant.

Worked Example 1.2

A call centre hires one team leader for every ten operators. Each team leader is paid $2,000 per month. The number of operators varies by workload.

Question: What type of cost is the total team leader salary, and how does it behave as the number of operators increases from 7 to 16?

Answer:

Team leader salary is a stepped cost. It is $2,000 for up to 10 operators. When hiring the 11th operator, a second leader is needed, so cost increases instantly to $4,000 and remains fixed for 11–20 operators.

Worked Example 1.3

You are given the following cost data:

| Machine Hours | Total Maintenance Cost ($) |

|---|---|

| 1,000 | 4,000 |

| 2,500 | 6,500 |

| 3,500 | 8,500 |

Question: Using the high-low method, calculate the variable cost per machine hour and the fixed maintenance cost.

Answer:

Variable cost per hour: ($8,500 – $4,000) / (3,500 – 1,000) = $4,500 / 2,500 = $1.80 per machine hour. Fixed cost: $4,000 – (1,000 × $1.80) = $2,200.

How Cost Behaviour Affects Budgets and Decision-Making

The classification of costs directly influences:

- Budget formulation: Variable and fixed costs must be treated differently when preparing budgets for various output levels.

- CVP (Cost-Volume-Profit, or breakeven) analysis: Only variable costs are deducted to find contribution per unit; fixed costs must be considered on a period basis.

- Variance analysis and standard costing: Standards for costs must be set based on their behaviour.

Exam Warning: Do not treat all costs as variable when performing breakeven or margin of safety calculations. Only include costs that truly vary with production in your variable cost per unit figure.

Revision Tip: When analysing costs, always ask: "Will this cost change if activity changes by one unit?" If yes, it's variable or semi-variable; if no, it's fixed or stepped over the relevant range.

Summary

- Fixed costs do not change in total with output, but unit fixed cost decreases as output increases.

- Variable costs change directly in total with activity, but are constant per unit.

- Semi-variable costs have both fixed and variable elements; split them to aid forecasting and control.

- Stepped costs increase in jumps at certain activity levels, not smoothly with each unit.

| Cost Type | Total Behaviour | Unit Behaviour | Example |

|---|---|---|---|

| Fixed | Constant | Decreases as volume rises | Factory rent |

| Variable | Proportional to volume | Constant | Raw materials |

| Semi-variable | Mixed behaviour | Varies with output | Utility bills (standing + usage) |

| Stepped | Fixed within intervals, jumps up at thresholds | Sudden jumps at cutoffs | Supervisor salaries for teams |

Key Point Checklist

This article has covered the following key knowledge points:

- Outline the definition and behaviour of fixed, variable, semi-variable, and stepped costs

- Explain the importance of cost classification for ACCA exam topics, especially budgeting and CVP analysis

- Apply the high-low method to split mixed costs

- Identify cost behaviour errors in exam questions

- Recognise how cost types influence managerial decisions and financial control

Key Terms and Concepts

- fixed cost

- variable cost

- semi-variable (mixed) cost

- stepped cost

- high-low method