Learning Outcomes

After reading this article, you will be able to explain the main types of costs, describe cost behaviour patterns, and apply the high–low method to split semi-variable costs into fixed and variable elements. You will learn to estimate total costs at different activity levels using linear equations and understand the core exam requirements on cost estimation within the ACCA Performance Management (PM) syllabus.

ACCA Performance Management (PM) Syllabus

For ACCA Performance Management (PM), you are required to understand cost classification, identify cost behaviour, and use analytical techniques for forecasting and budgeting. In particular, you should be able to:

- Classify costs as fixed, variable, semi-variable or stepped.

- Analyse fixed and variable cost elements from total cost data using the high–low method.

- Use derived cost equations to estimate future total costs at given activity levels.

- Recognise the limitations of cost estimation techniques used for budgeting and control purposes.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following best describes a semi-variable cost?

- a) Increases in proportion to output

- b) Remains unchanged with changes in activity

- c) Includes both a fixed and a variable component

- d) Rises in discrete steps as activity increases

-

True or false? The high–low method provides an estimate of the fixed and variable elements of a semi-variable cost by analysing only the highest and lowest activity levels.

-

You observe total maintenance costs of $5,000 for 2,000 units and $7,200 for 5,500 units. What is the estimated variable cost per unit?

-

Briefly explain the main limitation of the high–low method in analysing cost behaviour.

Introduction

Understanding how costs behave with changes in activity is fundamental for management accounting, budgeting, and performance management. Classifying costs correctly and using reliable estimation techniques allows managers to prepare budgets, analyse variances, and make informed decisions.

This article provides a structured revision of cost types, cost behaviour, and the use of the high–low method for separating mixed costs. Command of these techniques will help you answer both computational and discussion questions in the ACCA PM exam.

Test Tip: When revising High–low method and cost estimation, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Cost Classification and Cost Behaviour

Costs are commonly classified based on how they respond to changes in activity:

- Fixed costs remain unchanged over a given range of activity (e.g. rent, manager salaries).

- Variable costs change directly in proportion to output (e.g. materials, piecework labour).

- Semi-variable (mixed) costs contain both fixed and variable components (e.g. telephone bills, utilities).

- Stepped costs remain fixed over a certain range, then increase to a new level when activity passes a threshold (e.g. supervisor costs that increase when adding a new shift).

Key Term: Fixed cost

A cost that does not change in total within a relevant range, regardless of changes in activity level. Key Term: Variable cost

A cost that changes in direct proportion to changes in activity level. Key Term: Semi-variable cost

A cost with both fixed and variable elements; part remains constant, part varies with activity. Key Term: Stepped cost

A cost that is fixed within certain limits of activity but increases by discrete amounts when activity passes a threshold.

Cost estimation and control require you to identify these patterns and use historic data to predict future cost behaviour.

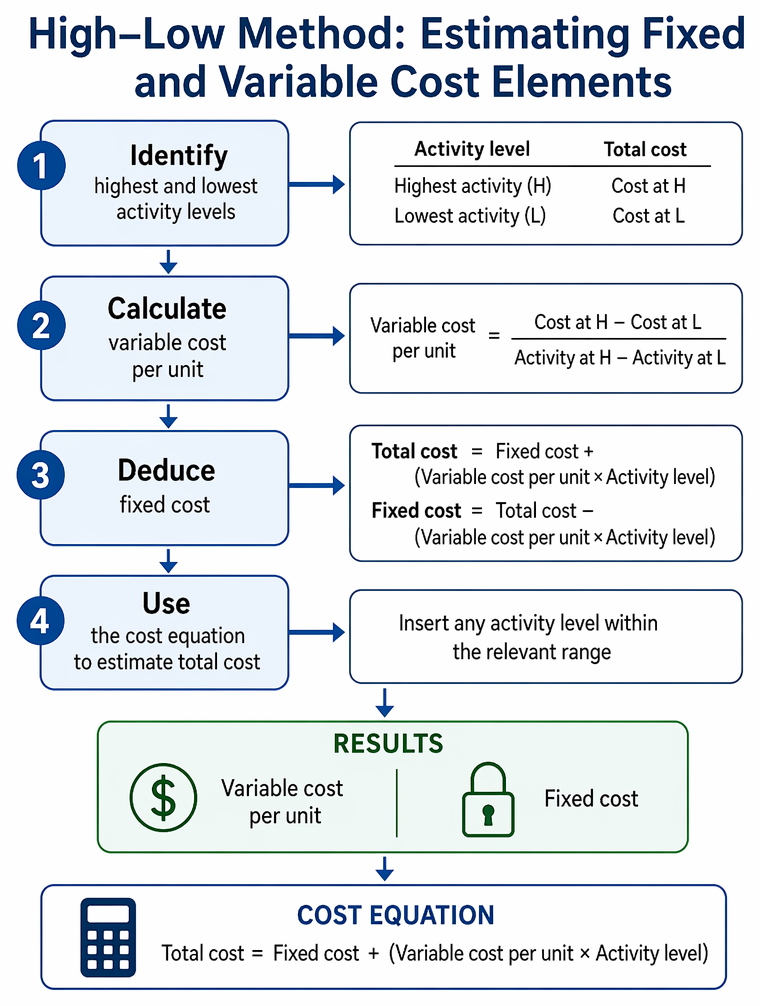

The High–Low Method

When confronted with semi-variable costs, it is important to separate the fixed and variable elements for accurate budgeting and cost control.

High–low cost estimation sequence from selecting highest and lowest activity observations to forecasting total cost within the relevant range.

Key Term: High–low method

A quick technique for estimating fixed and variable cost elements by comparing total costs at the highest and lowest activity levels observed.

Approach

- Identify the periods with the highest and lowest activity levels, noting the corresponding total costs.

- Calculate the variable cost per unit as the change in total cost divided by the change in activity (“rise over run”).

- Deduce the fixed cost by substituting into the cost equation: Total cost = Fixed cost + (Variable cost per unit × Activity level).

- Use the resulting equation to estimate total costs at any activity level within the relevant range.

Worked Example 1.1

A production manager records total maintenance costs of $12,600 for 3,000 machine hours and $18,600 for 8,000 machine hours.

Required: Estimate the variable cost per machine hour and the monthly fixed cost.

Answer:

Change in activity = 8,000 – 3,000 = 5,000 hours Change in cost = $18,600 – $12,600 = $6,000 Variable cost per machine hour = $6,000 ÷ 5,000 = $1.20 Substitute in either observation: $12,600 = Fixed cost + ($1.20 × 3,000) $12,600 = Fixed cost + $3,600 Fixed cost = $9,000 Equation: Total maintenance cost = $9,000 + $1.20 × machine hours

Worked Example 1.2

A company produces the following total costs at two activity levels:

- 5,000 units: $25,000

- 9,000 units: $33,000

Required: Estimate the total cost if output is 7,000 units.

Answer:

Change in output = 9,000 – 5,000 = 4,000 units Change in total cost = $33,000 – $25,000 = $8,000 Variable cost per unit = $8,000 ÷ 4,000 = $2 Substitute back (using 5,000 units): $25,000 = Fixed cost + ($2 × 5,000) $25,000 = Fixed cost + $10,000 Fixed cost = $15,000 Estimated total cost at 7,000 units: Total cost = $15,000 + ($2 × 7,000) = $29,000Exam Warning: Do not use average costs or combine multiple data pairs in the high–low method. Always use the highest and lowest activity levels, not the highest and lowest costs, since the highest cost may not correspond to the highest activity. Misidentifying the levels can lead to incorrect estimates.

Cost Estimation Equations for Forecasting

The result of the high–low method is a linear cost equation:

Total cost (y) = Fixed cost (a) + (Variable cost per unit (b) × Activity level (x))

This equation allows you to forecast total costs at other activity levels for budgeting and decision making.

Key Term: Cost estimation equation

A mathematical expression of total cost as a function of activity level (e.g. y = a + bx), enabling predictable cost forecasting.

Limitations of the High–Low Method

- It uses only two data points, ignoring all other historical data.

- Results may be skewed if either the high or low point is unrepresentative or influenced by abnormal events.

- Assumes a strictly linear relationship between cost and activity, which may not hold in real operations.

- Not reliable if costs are affected by inflation, seasonality, or activity outside the “relevant range.”

Worked Example 1.3

Maintenance cost data over 6 months:

| Month | Output (units) | Total Cost ($) |

|---|---|---|

| January | 1,000 | 8,000 |

| February | 1,400 | 8,400 |

| March | 1,700 | 8,850 |

| April | 2,400 | 9,600 |

| May | 2,000 | 9,200 |

| June | 1,600 | 8,600 |

Required: Estimate fixed and variable cost elements.

Answer:

Highest activity: April (2,400 units, $9,600) Lowest activity: January (1,000 units, $8,000) Variable cost per unit = ($9,600 – $8,000) / (2,400 – 1,000) = $1,600 / 1,400 = $1.14 Fixed cost: $8,000 = Fixed + ($1.14 × 1,000) ⇒ Fixed = $8,000 – $1,140 = $6,860

Summary

Cost behaviour analysis and the high–low method equip managers with simple tools for budgeting and decision making. While useful for quick estimates, be alert to its restrictions: use with care and complement with more robust statistical techniques if possible.

Key Point Checklist

This article has covered the following key knowledge points:

- Classify costs as fixed, variable, semi-variable, or stepped

- Describe and identify cost behaviour patterns relevant to budgeting and control

- Apply the high–low method to separate fixed and variable elements of semi-variable costs

- Construct linear cost equations for forecasting total costs at any given activity level

- Recognise limitations of the high–low method and describe potential alternative approaches

Key Terms and Concepts

- Fixed cost

- Variable cost

- Semi-variable cost

- Stepped cost

- High–low method

- Cost estimation equation