Learning Outcomes

After reading this article, you will be able to distinguish between absorption and marginal costing systems, explain how each treats fixed production overheads, and calculate both inventory values and profit under both methods. You will also be able to reconcile differences in reported profit using profit reconciliation statements, in line with ACCA Performance Management (PM) exam requirements.

ACCA Performance Management (PM) Syllabus

For ACCA Performance Management (PM), you are required to understand and apply different costing methods for inventory valuation and profit calculation. In particular, focus your revision on:

- Explaining the concepts of absorption costing and marginal costing

- Calculating profit and inventory values under each method

- Reconciling the profit difference between the two costing systems

- Assessing the implications of each method for internal reporting and decision making

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which statement best describes how absorption costing treats fixed production overheads?

- a) Expensed in full in the period incurred

- b) Included in inventory valuation

- c) Treated as a period cost only

- d) Excluded from the computation of profit

-

Marginal costing treats fixed production overheads as:

- a) Part of the product cost

- b) Included in closing inventory

- c) Written off in full as an expense of the period

- d) Allocated between closing inventory and cost of sales

-

True or false? If production exceeds sales, absorption costing will report a higher profit than marginal costing.

-

Briefly explain why opening and closing inventory levels impact the profit reported under absorption and marginal costing.

Introduction

Accurately measuring product costs is necessary for inventory valuation, internal reporting, and performance assessment. Two widely-used techniques are absorption costing and marginal costing. Each method allocates fixed production overheads differently, producing distinct impacts on calculated inventory values and period profit.

Understanding the differences is critical for both the ACCA exam and practice, particularly when you are required to analyze company performance or recommend costing systems for decision making.

Key Term: Absorption costing

A costing system in which all production costs (variable and fixed) are absorbed into units produced, so inventory and cost of sales include a share of fixed production overheads. Key Term: Marginal costing

A costing system in which only variable production costs are included in unit cost; all fixed production overheads are treated as period costs and written off in full against contribution.

Absorption Costing vs Marginal Costing—Core Principles

Absorption costing and marginal costing differ mainly in their treatment of fixed production overheads.

- Absorption costing allocates fixed overheads across the units produced, including them in inventory valuations. This results in closing inventory values that contain a share of fixed costs.

- Marginal costing treats all fixed production overheads as period costs, writing them off directly to the statement of profit or loss. Inventory only reflects variable production costs.

This fundamental difference means that profit calculations and inventory values will usually not be the same under the two systems unless there is no change in inventory.

Effects on Inventory Valuation and Reported Profit

The key impact is that absorption costing includes a proportion of fixed overheads in closing inventory, deferring their recognition as an expense until the inventory is sold. Marginal costing expenses all fixed production overheads straight away, regardless of how much is sold.

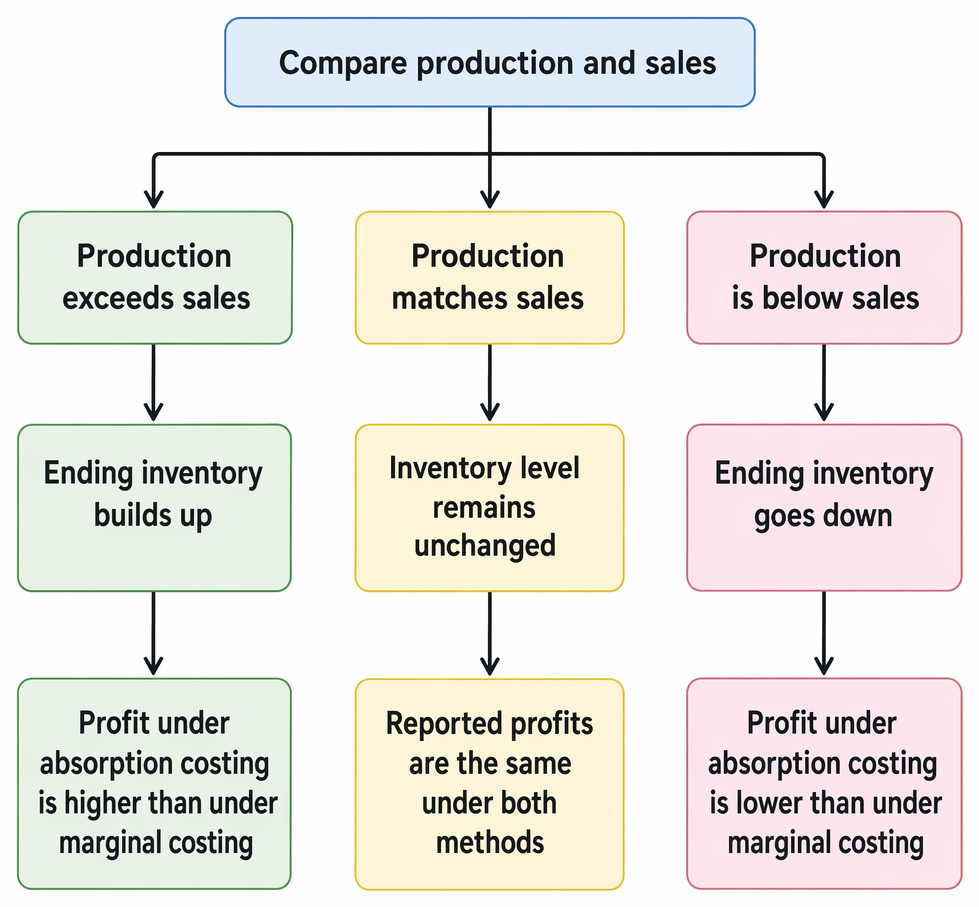

When production and sales levels differ, profit under each method may not be the same.

- If production > sales: Absorption costing carries forward some fixed overheads into the next period as part of unsold inventory. Reported profit will be higher under absorption costing.

- If production < sales: Absorption costing releases previously absorbed fixed overheads via cost of sales—this can reduce profit compared to marginal costing.

Exam Warning: Always check for opening and closing inventory levels when comparing profits under absorption and marginal costing. Only the fixed overheads in these inventories cause the difference in reported profit.

Worked Example 1.1

A company produces widgets with the following costs:

- Variable production cost per unit: $10

- Fixed production overhead: $10,000 per month

- Output for April: 2,000 units

- Sales for April: 1,800 units

- Selling price: $25 per unit There is no inventory at the start of April.

Required: Calculate profit for April under absorption costing (fixed overhead absorbed at $5 per unit) and marginal costing. Reconcile any difference.

Answer:

Absorption costing:

- Fixed O/H rate: $10,000 / 2,000 units = $5/unit

- Cost per unit: $10 (variable) + $5 (fixed) = $15

- Units in inventory: 2,000 - 1,800 = 200 units (all closing)

- Sales revenue: 1,800 × $25 = $45,000

- Cost of sales: 1,800 × $15 = $27,000

- Closing inventory: 200 × $15 = $3,000

- Overheads absorbed: $5 × 2,000 = $10,000 (no over/under absorption)

- Profit: $45,000 - $27,000 = $18,000

Marginal costing:

- Variable cost of sales: 1,800 × $10 = $18,000

- Contribution: $45,000 - $18,000 = $27,000

- Less fixed overhead (whole period): $10,000

- Profit: $17,000

Reconciliation: Absorption profit $18,000 Marginal profit $17,000 Difference: $1,000 = Fixed overhead in closing inventory (200 × $5)

Profit Reconciliation Statement

The difference in reported profit equals the change in inventory (units) multiplied by the fixed overhead absorption rate per unit:

Key Term: Fixed overhead absorption rate

The fixed production overhead cost assigned to each unit produced for absorption costing purposes.

Inventory increases, no change, or decreases determine whether absorption-costing profit is higher than, equal to, or lower than marginal-costing profit.

Profit difference = Change in inventory (units) × Fixed overhead rate per unit

- If inventory increases (production > sales): profit under absorption costing is higher.

- If inventory decreases (sales > production): profit under absorption costing is lower.

Test Tip: For profit reconciliation, identify whether inventory increased or decreased, then multiply the inventory movement by the fixed overhead absorption rate.

Worked Example 1.2

Continuing Example 1.1, in May the company produces 1,600 units and sells 1,800 units.

Required: Calculate the profit under each method and reconcile the difference.

Answer:

Absorption costing:

- Opening inventory: 200 units @ $15 = $3,000

- Production: 1,600 units

- Total available: 1,800 units sold = 200 from opening, 1,600 from current

- Sales revenue: 1,800 × $25 = $45,000

- Cost of sales: 1,600 × $15 = $24,000 (current) + $3,000 (opening) = $27,000

- Fixed overhead absorbed: $5 × 1,600 = $8,000

- Overhead under-absorbed: Actual $10,000 – absorbed $8,000 = $2,000 adverse expense

- Profit: $45,000 – $27,000 – $2,000 = $16,000

Marginal costing:

- Variable cost of sales: 1,800 × $10 = $18,000

- Contribution: $45,000 – $18,000 = $27,000

- Fixed overhead: $10,000

- Profit: $17,000

Reconciliation: Now, inventory decreases by 200 units. 200 units × $5 rate = $1,000 Absorption profit $16,000 Marginal profit $17,000 Absorption profit is lower by $1,000, as 200 units’ worth of overheads are released from inventory.

Summary Table: Key Differences

| Aspect | Absorption Costing | Marginal Costing |

|---|---|---|

| Inventory valuation | Variable + fixed production costs | Variable production costs only |

| Fixed overheads | Allocated to units produced | Expensed in period incurred |

| Profit affected by stock | Yes—depends on inventory change | No—depends on units sold |

| Reporting use | External and internal use, statutory | Internal management, decision making |

| Consistency with IAS 2 | Yes (required for published accounts) | No |

When to Use Each Method

- Absorption costing is required for external financial reporting and inventory valuation (IAS 2).

- Marginal costing is more suitable for internal management decision making, as it clearly shows contribution and the impact of changes in sales/production.

Key Point Checklist

This article has covered the following key knowledge points:

- Define absorption costing and marginal costing, and explain the principal differences

- Calculate inventory values and profit under each system

- Prepare a profit reconciliation statement between the two methods

- Identify circumstances in which each costing system is most appropriate

- Recognize the implications for decision making and external reporting

Key Terms and Concepts

- Absorption costing

- Marginal costing

- Fixed overhead absorption rate