Learning Outcomes

After studying this article, you will be able to distinguish between cost-plus, marginal cost-plus, and target costing approaches. You will learn how to calculate prices using each method, evaluate their suitability in different scenarios, and explain the impact of each method for management decision-making and performance measurement.

ACCA Performance Management (PM) Syllabus

For ACCA Performance Management (PM), you are required to understand how different pricing strategies are selected and applied, their financial basis, and their implications for business decisions. Revision for this topic should focus on:

- The calculation and application of cost-plus and marginal cost-plus pricing

- The principles of target costing, including the calculation of target costs and identification of a cost gap

- The advantages and limitations of each pricing approach

- How target costing encourages cost management and links to market-based pricing

- When each pricing method is appropriate in practice

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A company calculates the selling price of its products by adding 20% to the full unit cost. This is an example of:

- a) Marginal cost-plus pricing

- b) Full cost-plus pricing

- c) Target costing

- d) Market skimming pricing

-

Which one of the following is a key step in the target costing approach?

- a) Set a cost based on recent production costs

- b) Set a price based on competitor prices and deduct a required profit margin to calculate the target cost

- c) Add a profit margin to the marginal cost per unit

- d) Ignore competitive forces

-

True or false? Marginal cost-plus pricing risks not covering a business’s fixed costs if not properly monitored over time.

-

Briefly explain when it may be preferable to use target costing rather than cost-plus pricing.

Introduction

Setting the right selling price for products or services is essential for maximising profitability and long-term sustainability. Businesses may choose from several pricing methods, including cost-based and market-based approaches. Three approaches especially relevant for ACCA Performance Management are: cost-plus pricing, marginal cost-plus pricing, and target costing. Each has distinct calculation methods, fundamental assumptions, and practical implications.

Key Term: cost-plus pricing

A pricing method where a fixed percentage or amount (“mark-up” or “margin”) is added to the full unit cost to determine the selling price. Key Term: marginal cost-plus pricing

A pricing method where a mark-up is added only to the variable (“marginal”) cost per unit, excluding fixed overheads, to set a selling price. Key Term: target costing

A market-driven pricing method where the selling price is set based on what customers are willing to pay, then a required profit margin is deducted to establish the “target cost”—the maximum allowable cost to achieve the desired profit.

COST-PLUS PRICING

Cost-plus pricing is the traditional starting point for many businesses. The company calculates its production cost per unit (either fully absorbed cost or just prime cost) and then adds a mark-up or margin to achieve the required profit.

There are two common variants:

- Full cost-plus pricing: The mark-up is applied to the full production cost per unit, including allocated fixed overheads.

- Marginal cost-plus pricing: The mark-up is applied only to the variable (“marginal”) cost per unit.

The formulae can be summarised as:

- Full cost-plus price = Full production cost per unit + mark-up

- Marginal cost-plus price = Marginal cost per unit + mark-up

Worked Example 1.1

A manufacturer’s full unit cost is $40, which includes fixed and variable costs. The company applies a 25% mark-up on cost. What is the selling price per unit?

Answer:

Selling price = $40 + (25% × $40) = $40 + $10 = $50 per unit.

Advantages and Limitations

Advantages:

- Simple and easy to apply.

- Ensures costs are covered (if volumes are achieved as budgeted).

- Facilitates stable prices over time for customers.

Limitations:

- May ignore customer willingness to pay and competitor prices.

- Relies on allocating all costs accurately, including fixed overheads.

- If actual sales volumes are lower than planned, fixed costs may not be recovered, leading to losses.

Worked Example 1.2

A business makes a product with a marginal (variable) cost per unit of $22 and fixed costs budgeted at $18 per unit (based on an annual output of 1,000 units). The company wishes to price the product on a marginal cost-plus basis with a 50% mark-up. What is the price per unit?

Answer:

Marginal cost plus 50% mark-up: Selling price = $22 + (50% × $22) = $22 + $11 = $33 per unit. Note: There is a risk that if too many units are sold at this price, total fixed costs may not be covered.Exam Warning: Cost-plus and marginal cost-plus prices depend heavily on the correct allocation of costs and expected output. If actual volumes are not achieved, costs might not be fully recovered. In exam questions, be clear about whether the mark-up is on marginal or full cost and use the correct base for calculations.

TARGET COSTING APPROACH

As markets become more competitive, businesses may find that cost-plus prices exceed what customers are willing to pay or competitor prices. Target costing reverses the calculation. Businesses estimate a competitive market price, deduct a required profit margin, and set the “target cost” for the product. Achieving the target cost then becomes the objective during product design and production planning.

Process summary:

- Estimate a competitive selling price.

- Deduct the required profit margin to determine the allowable (“target”) cost.

- Compute the cost gap (if any) by comparing the target cost and the estimated achievable cost.

- Apply cost-reduction and value analysis techniques to meet the target cost.

Key Term: cost gap

The difference between the current estimated product cost and the target cost. Represents the amount by which costs must be reduced to achieve desired profitability.

Worked Example 1.3

A company plans a new product. Market research suggests a competitive price is $120/unit. Management requires a profit margin of $30 per unit. What is the target cost, and what should be done if the estimated unit cost is $98?

Answer:

Target cost = Selling price – Required profit Target cost = $120 – $30 = $90 per unit Estimated unit cost is $98—so there is a cost gap of $8 ($98 – $90). The company must redesign the product, improve processes, or seek cost reductions to close the gap and meet the target.

Techniques for Closing the Cost Gap

If a cost gap exists, possible actions include:

- Redesigning the product to remove non-value-adding features

- Negotiating with suppliers for better material costs

- Streamlining production processes to improve efficiency

- Reviewing the supply chain for opportunities to lower costs

Suitability and Practical Considerations

Target costing is most useful:

- Prior to launching new products

- In highly competitive, price-sensitive markets

- Where product cost can be influenced at the design stage

Once designs are fixed and production is underway, it is much harder to achieve large cost reductions.

Key Term: value analysis

A systematic approach to assessing every feature of a product or process to determine whether it adds value for the customer relative to its cost. Used to support cost reduction under target costing. Key Term: mark-up

The percentage or amount added to a cost base (e.g., full or marginal cost) to determine a selling price. May be calculated as a percentage of cost or of sales price.

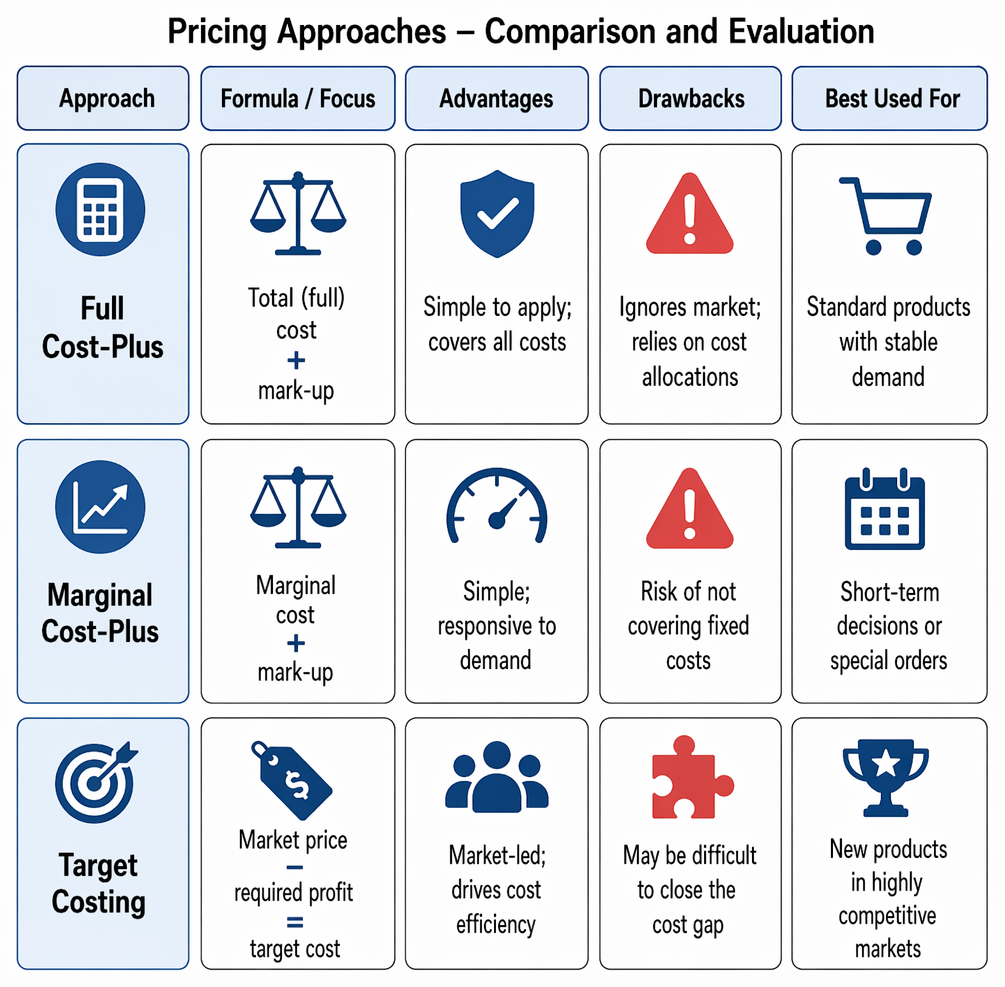

Comparison and Evaluation Table

Pricing method choice is mapped to typical applications, including market-led target costing, stable-demand full cost-plus, and spare-capacity marginal cost-plus.

| Approach | Formula / Focus | Advantages | Drawbacks | Best Used For... |

|---|---|---|---|---|

| Full Cost-Plus | Full cost + mark-up | Easy, covers all costs | Ignores market, relies on allocations | Standard products with stable demand |

| Marginal Cost-Plus | Marginal cost + mark-up | Simple, responsive to demand | Risk of not covering fixed costs | Short-term or special orders |

| Target Costing | Market price – required profit = target cost | Market-led, encourages efficiency | May be hard to close cost gap | New products, highly competitive markets |

Worked Example 1.4

A business has a full production cost per unit of $50, a marginal cost per unit of $32, and faces a competitive market price of $55. The company requires a 20% profit margin. Should it use cost-plus or target costing, and what pricing method is likely to be most effective?

Answer:

Cost-plus price (full) = $50 + (20% × $50) = $60 Cost-plus price (marginal) = $32 + (20% × $32) = $38.40 Target cost = $55 (market price) – (20% × $55) = $44 Target costing is appropriate. Since the full cost-plus price is above the market, the business must reduce costs to meet the $44 target cost or consider not launching the product.Revision Tip: For PM exam questions, always check if the question refers to full cost, marginal cost, or a competitive market price. Select the approach that fits the scenario and show clear workings in your answer.

Summary

- Cost-plus pricing adds a mark-up to full costs, ensuring cost recovery if expected volumes are achieved.

- Marginal cost-plus pricing applies a margin only to variable costs and suits limited cases (e.g., special orders or spare capacity). It is risky as a long-term policy due to fixed cost under-recovery.

- Target costing starts with the market price, works backwards to the allowed cost, and drives cost reduction efforts.

- In competitive markets, target costing links pricing decisions directly to customer expectations and cost control.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain and apply both cost-plus and marginal cost-plus pricing methods

- Calculate prices and mark-ups for both methods

- Define target costing and calculate target costs and cost gaps

- Outline what actions may be taken to close a cost gap

- Evaluate advantages and limitations of each approach

- Identify which situations suit each pricing method for ACCA exam purposes

Key Terms and Concepts

- cost-plus pricing

- marginal cost-plus pricing

- target costing

- cost gap

- value analysis

- mark-up