Learning Outcomes

After reading this article, you will be able to explain how to identify and analyse limiting factors in short-term decision-making scenarios. You will know how to calculate and use contribution per unit of scarce resource, rank products, and determine the optimal production plan when faced with resource constraints. You will also understand the principles of relevant costing as applied to these decisions.

ACCA Performance Management (PM) Syllabus

For ACCA Performance Management (PM), you are required to understand the impact of limiting factors on short-term decision making and how to apply relevant costing efficiently. Focus your revision on:

- Identifying limiting (scarce) factors in production or service scenarios

- Calculating and interpreting contribution per unit and per limiting factor

- Ranking products or options to optimise resource use

- Determining optimal plans when faced with one or more limiting factors (including ranking and allocation)

- Understanding and applying relevant costing for decision making, including opportunity costs

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the correct approach to selecting which products to manufacture when there is one scarce resource?

- a) Highest selling price per unit

- b) Lowest material cost per unit

- c) Highest contribution per unit of scarce resource

- d) Most units demanded

-

In a situation where machine hours are limited, how do you rank products for production?

- a) By maximum total sales value

- b) By lowest labour hour per unit

- c) By contribution per machine hour

- d) By minimum variable cost

-

True or false? An opportunity cost is always included when a resource used could have been put to an alternative profitable use.

-

What step should be taken after ranking products by contribution per unit of limiting factor?

Introduction

In practice, businesses frequently face restrictions on resources such as labour, machine hours, or materials. These restrictions, known as limiting factors or key factors, prevent an organisation from meeting all of its potential demand. In such cases, efficient use of limited resources is essential for maximising overall profit. This article explains how to apply relevant costing and contribution concepts to make informed short-term decisions when resources are in short supply.

Key Term: Limiting Factor

The resource or input that is in shortest supply relative to demand, thereby limiting output and influencing production planning. Key Term: Contribution per Unit of Limiting Factor

The amount of contribution (sales less variable cost) earned for each unit of the limited resource used, calculated as contribution per unit divided by units of the resource required per product.

RELEVANT COSTING AND THE LIMITING FACTOR PROBLEM

Relevant costing is central to short-term decisions. Only costs and revenues that will change as a result of a decision should be considered. When one resource is limited, the objective is usually to maximise total contribution, as fixed costs are assumed not to change in the short run.

When multiple products compete for the same scarce resource, contribution per unit alone is not enough. Instead, prioritise products based on the contribution they generate per unit of the limiting factor. This approach ensures the best use of the scarce resource, driving total profit higher.

Key Term: Relevant Cost

The future cash flow that will change as a direct result of a specific decision. Key Term: Opportunity Cost

The value of the benefit forgone by choosing one alternative over the next best alternative.

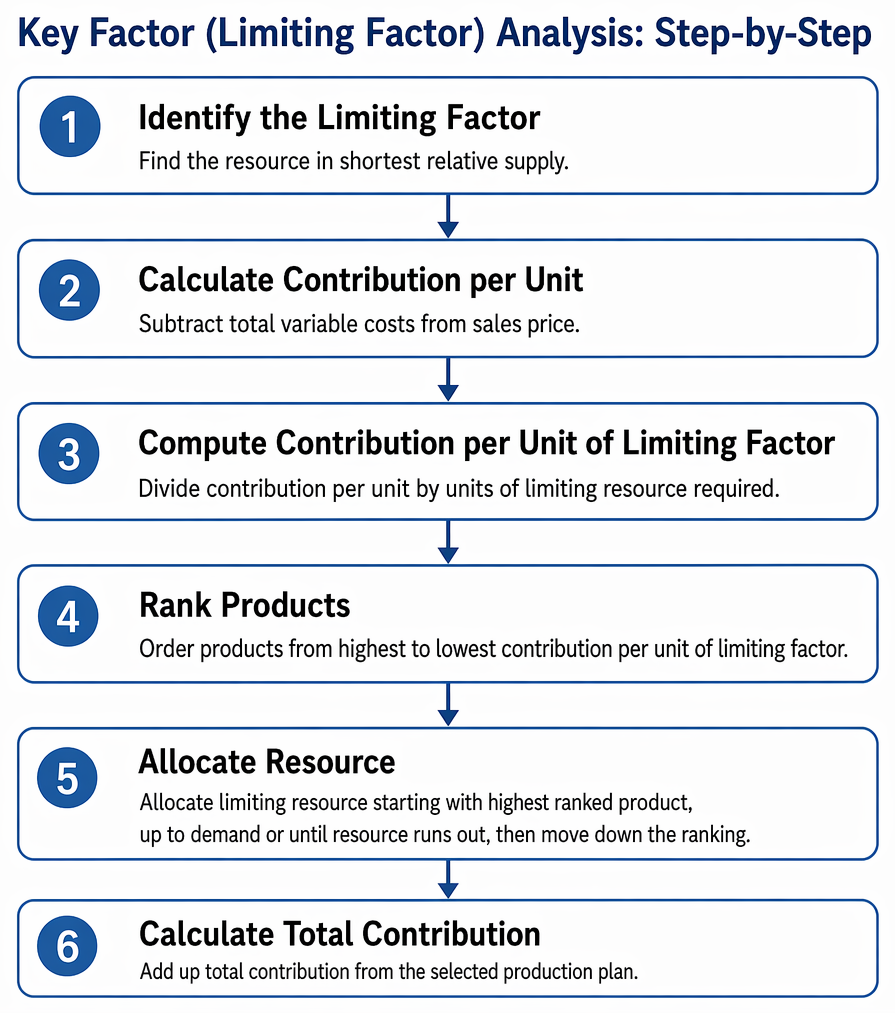

KEY FACTOR (LIMITING FACTOR) ANALYSIS: STEP-BY-STEP

To determine the optimal production plan when a resource is limited, follow this structured approach:

Short-term production choices with scarce resources are mapped from limiting-factor identification to contribution ranking or linear programming.

- Identify the Limiting Factor: Determine which resource (e.g. labour, machine hours, materials) is in shortest relative supply.

- Calculate Contribution per Unit: For each product, subtract total variable costs from sales price.

- Compute Contribution per Unit of Limiting Factor: Divide each product’s contribution per unit by the units of limiting resource required per product.

- Rank Products: Rank all products in order of highest to lowest contribution per unit of limiting factor.

- Allocate Resource: Allocate the limiting resource starting with the highest ranked product, up to the demand or until the resource runs out, then move down the ranking.

- Calculate Total Contribution: Add up total contribution from the selected production plan.

Worked Example 1.1

A company makes two products, A and B. Each A gives a $12 contribution, requiring 4 machine hours per unit. Each B gives a $10 contribution, requiring 2 machine hours per unit. Maximum sales are 400 units of A and 600 units of B. Only 2,000 machine hours are available.

Required: Determine the optimal production quantities to maximise total contribution.

Answer:

- Contribution per machine hour, A: $12 ÷ 4 = $3

- Contribution per machine hour, B: $10 ÷ 2 = $5

- Rank: B (higher), then A

- Step 1: Produce all 600 B, requiring 1,200 machine hours (600 × 2)

- Step 2: Remaining hours: 2,000 – 1,200 = 800

- A units possible = 800 ÷ 4 = 200 Production plan: 600 B, 200 A Total contribution: (600 × $10) + (200 × $12) = $6,000 + $2,400 = $8,400

Revision Tip: Instead of memorising formulas, practice this method using different scenarios—most exam questions follow this logical sequence.

OPPORTUNITY COSTS AND RELEVANT COSTS IN SHORT-TERM DECISIONS

Not all costs are relevant. Only future cash flows that change due to the decision should be included.

In the case of scarce resources, if the resource could be used on an alternative profitable activity, the opportunity cost of not pursuing that activity must be added to the relevant cost.

Worked Example 1.2

A manufacturer can use 1,000 hours of skilled labour to produce either Product X or Product Y. X yields $20 per unit contribution, needing 4 labour hours per unit. Y yields $12 per unit, needing 3 hours per unit. X’s maximum demand is 100 units, Y’s is unlimited.

Required: What is the opportunity cost if labour hours are used to make 100 units of X instead of Y?

Answer:

- Labour needed for 100 X: 100 × 4 = 400 hours

- Remaining hours: 1,000 – 400 = 600 hours for Y

- Y units = 600 ÷ 3 = 200

- If all 1,000 hours used for Y: 1,000 ÷ 3 = 333 units (rounded)

- Contribution: 333 × $12 = $3,996

- Contribution from X+Y: (100 × $20) + (600 ÷ 3 × $12 = 200 × $12) = $2,000 + $2,400 = $4,400

- Opportunity cost: $3,996 – $4,400 = –$404

Actually, using 400 hours for X and the rest for Y yields a higher contribution; thus, the opportunity cost is the profit you give up if you cannot allocate resources optimally.

MULTI-LIMITING FACTOR SCENARIOS

With two or more scarce resources (e.g., both labour and materials restrict output), linear programming is required. At ACCA PM level, you should be able to form simple linear programming problems and understand that the solution will lie where constraint lines meet (the ‘feasible region’).

You may be given two simultaneous constraints and asked to find the intersection using algebra, or interpret a feasible region on a graph.

Worked Example 1.3

A company produces Product P ($15 contribution/unit, uses 3 machine hours and 2 kg materials) and Product Q ($10/unit, 2 machine hours and 5 kg materials). There are 120 machine hours and 180 kg materials available.

Required: Write the constraints and, if P = x units, Q = y units, formulate the objective.

Answer:

- Objective: Maximise C = 15x + 10y

- Machine hours: 3x + 2y ≤ 120

- Materials: 2x + 5y ≤ 180

- Non-negativity: x ≥ 0, y ≥ 0

Exam Warning: Do not simply rank on contribution per unit when resources are limited. Always convert to contribution per limiting factor or you may select unprofitable products and lose easy marks.

Summary

Limiting factor analysis ensures efficient allocation of scarce resources by ranking products according to their contribution per unit of the limited input. This method maximises short-term profit, as only costs and revenues changing as a result of the decision are relevant. Understanding and applying opportunity cost is essential when alternative uses exist for limited resources.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify limiting (scarce) factors in resource allocation scenarios

- Calculate contribution per unit and per limiting factor

- Rank products or services based on contribution per scarce resource

- Allocate resources in order of ranking, up to demand or resource limit

- Recognise and include opportunity costs when relevant

- Understand that only future, differential, cash flows are relevant to short-term decisions

Key Terms and Concepts

- Limiting Factor

- Contribution per Unit of Limiting Factor

- Relevant Cost

- Opportunity Cost