Learning Outcomes

After reading this article, you will be able to explain and apply the IFRS 9 approach to financial asset impairment, describe the expected credit loss (ECL) model, and identify the three stages of credit risk (staging). You will also understand how impairment affects hedge accounting relationships and how expected credit losses are measured and recognized in financial statements for ACCA SBR.

ACCA Strategic Business Reporting (SBR) Syllabus

For ACCA Strategic Business Reporting (SBR), you are required to understand how IFRS 9 assesses impairment of financial assets and the impact on hedge accounting. This article supports your revision on:

- The general approach to impairment of financial assets in IFRS 9

- The expected credit loss (ECL) model and calculation methods

- The three-stage 'staging' model for assessing significant increases in credit risk

- Application of impairment requirements to trade receivables and other financial assets

- The interaction between impairment and hedge accounting relationships

- Practical implications for disclosures and examination scenarios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the difference between 12-month and lifetime expected credit losses in IFRS 9's impairment model?

- When must an entity recognise lifetime expected credit losses on a financial asset?

- How does a significant increase in credit risk affect the measurement of impairment under IFRS 9?

- True or false? All trade receivables must be measured for impairment using lifetime expected credit losses regardless of staging.

- Briefly explain how impairment provisions interact with hedge accounting relationships.

Introduction

IFRS 9 introduced a forward-looking approach to impairment of financial assets. Entities must now assess expected credit losses rather than waiting for objective evidence of impairment. The ECL model requires judgment to identify changes in credit risk (staging) and to estimate losses over either 12 months or the lifetime of the instrument. Understanding this framework, including the application to trade receivables and how impairment interacts with hedged items, is essential for ACCA SBR candidates.

Key Term: Expected Credit Loss (ECL)

The weighted average of credit losses, using the probability of default as weights, over either the next 12 months or over the asset’s lifetime. Key Term: Staging

The process in IFRS 9 of classifying financial assets into Stage 1 (no significant increase in credit risk), Stage 2 (significant increase in credit risk), and Stage 3 (credit-impaired) for impairment measurement.

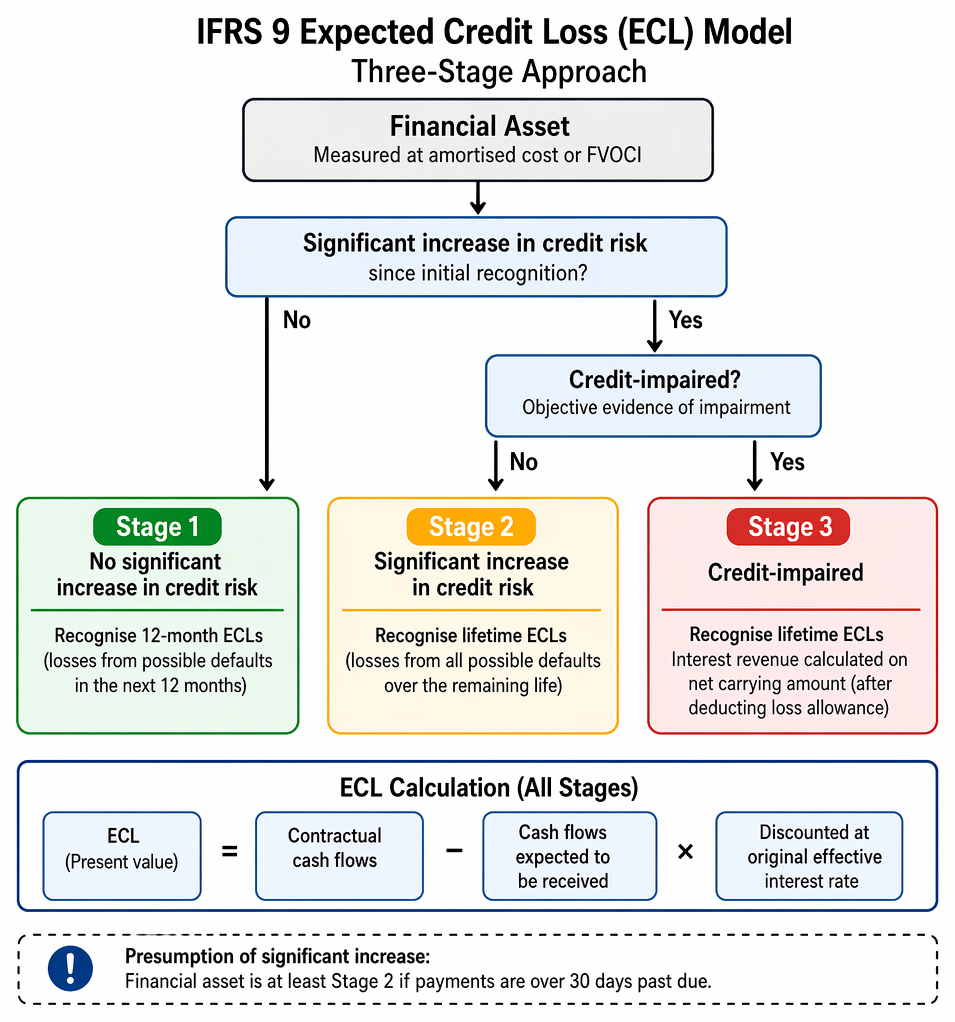

The Expected Credit Loss (ECL) Model

IFRS 9 requires ECLs to be recognized at each reporting date for financial assets carried at amortised cost or at fair value through other comprehensive income. The model uses three 'stages' to assess changing credit risk and applies different impairment calculations accordingly.

Credit risk assessment under IFRS 9 allocates assets to Stage 1, Stage 2, or Stage 3 for 12-month or lifetime ECL.

The Three-Stage Approach (Staging)

- Stage 1: Assets with no significant increase in credit risk since initial recognition. Measure impairment as 12-month ECLs, i.e., losses from possible defaults in the next year.

- Stage 2: Assets with a significant increase in credit risk since initial recognition but not yet credit-impaired. Recognise lifetime ECLs, i.e., losses from all possible defaults over the asset’s remaining life.

- Stage 3: Credit-impaired assets. Continue to recognise lifetime ECLs, but interest revenue is calculated on the net carrying amount (after deducting the loss allowance).

Key Term: 12-month Expected Credit Loss

The portion of lifetime ECLs resulting from default events possible within 12 months after the reporting date. Key Term: Lifetime Expected Credit Loss

The expected credit losses resulting from all possible default events over the expected life of the financial instrument.

When Does Credit Risk Increase Significantly?

Identifying a significant increase in credit risk requires comparison between the risk at initial recognition and at the reporting date. Forward-looking information, such as internal or external credit ratings and observable data, must be considered. Certain rebuttable presumptions assist entities, such as assuming a financial asset is at least Stage 2 if payments are over 30 days past due.

Calculating ECLs

ECLs are calculated as the present value of the difference between contractual cash flows and the cash flows an entity expects to receive, discounted at the asset’s original effective interest rate. Practical methods, such as provision matrices, are permitted for portfolios like trade receivables.

Key Term: Credit-impaired

A financial asset is credit-impaired when there is objective evidence of impairment, such as default, restructuring for economic or legal reasons, bankruptcy or other observable data.

Application to Trade Receivables and Lease Receivables

For trade receivables and contract assets (under IFRS 15), entities must always measure loss allowances at lifetime ECLs, even if a significant increase in credit risk has not occurred (i.e., Stage 2 by default).

Worked Example 1.1

An entity holds a bond with a gross carrying amount of $1,000,000. The probability of default in the next 12 months is estimated at 1%, and the loss given default is 60%. The asset is performing (Stage 1).

Calculate the initial loss allowance required under IFRS 9.

Answer:

12-month ECL = $1,000,000 × 1% × 60% = $6,000.

Worked Example 1.2

A customer’s trade receivable balance is $100,000. Based on historical and forward-looking data, the default rate for balances 31–60 days overdue is 5%. No collateral is held and loss given default is 100%. The receivable is 45 days past due.

How much loss allowance should be recognised?

Answer:

Lifetime ECL = $100,000 × 5% × 100% = $5,000. The entire $5,000 should be recognised, as IFRS 9 requires lifetime ECLs for trade receivables.Exam Warning: Beware: In exam scenarios, always clearly justify the staging—do not assume Stage 2 just because a debtor is slow to pay. Unless overdue by 30+ days or other evidence of increased risk is present, Stage 1 may still apply.

Measurement of Credit Losses

Expected credit losses must be:

- Unbiased and probability-weighted

- Reflective of time value of money (discounted)

- Based on reasonable supportable information (past events, current conditions, future forecasts)

The model is applied without waiting for a triggering loss event. At every reporting date, the loss allowance is updated and any changes flow through the statement of profit or loss.

Key Term: Loss Allowance

The amount recognised in the statement of financial position as a reduction of the gross carrying amount of a financial asset, representing expected credit losses.

Impact on Hedge Accounting

Impairment affects hedge accounting, particularly if the hedged item becomes credit-impaired or expected cash flows change substantially. Where ECLs are recognised or derecognised on hedged assets, the basis adjustment or hedge relationship may need revisiting.

- If a hedged item (like a forecast receipt) is no longer probable due to credit concerns, the hedge relationship may be discontinued.

- Changes in expected cash flows (including ECLs) must be reflected in hedge effectiveness assessments.

Key Term: Hedge Effectiveness

The degree to which changes in the fair value or cash flows of the hedging instrument offset those of the hedged item.

Disclosure Requirements

IFRS 7 requires entities to disclose information about credit risk, ECL measurement assumptions, changes in estimates, and how credit risk is managed. This helps users evaluate exposures and how expected losses may affect future performance.

Revision Tip: Pay extra attention to the distinction between 12-month and lifetime expected credit losses, especially when considering the effect of overdue balances for financial assets that do not automatically require lifetime ECLs like trade receivables.

Summary

IFRS 9 requires a proactive, forward-looking approach to impairment. Entities must always record at least 12-month ECLs, and lifetime ECLs if credit risk increases significantly or for trade receivables. The staging model requires ongoing monitoring of credit risk. Impairment recognition can impact hedge accounting relationships and brings new disclosure obligations.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the expected credit loss (ECL) model under IFRS 9

- Describe the three stages (staging) and their impact on measurement

- Identify how to determine when to recognise lifetime ECLs

- Apply the ECL model to trade receivables and contract assets

- Describe how impairment interacts with hedge accounting

- Understand the calculation and presentation of loss allowances

Key Terms and Concepts

- Expected Credit Loss (ECL)

- Staging

- 12-month Expected Credit Loss

- Lifetime Expected Credit Loss

- Credit-impaired

- Loss Allowance

- Hedge Effectiveness