Learning Outcomes

After reading this article, you will be able to explain and apply the recognition, measurement, and derecognition of property, plant and equipment (PPE) under IAS 16 and borrowing costs under IAS 23. You will understand the calculation and accounting for depreciation, the application of the revaluation model, and how to account for asset disposals. You will also be able to identify which costs can be capitalised, how to depreciate components, and when to derecognise assets.

ACCA Strategic Business Reporting (SBR) Syllabus

For ACCA Strategic Business Reporting (SBR), you are required to understand and apply the principles that underpin the accounting for property, plant and equipment and borrowing costs, including measurement models, depreciation methods, revaluation, and derecognition. Revision should focus on:

- The recognition and initial measurement requirements for PPE under IAS 16

- The subsequent measurement choices: cost versus revaluation model

- Depreciation methods, useful life, and residual value considerations

- The need to depreciate significant components separately

- Accounting for revaluations (including treatment of gains and losses and depreciation post-revaluation)

- The rules for derecognition/disposal of PPE

- Determining which costs qualify for capitalisation under IAS 23

- The period over which borrowing costs may be capitalised

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What initial costs may be included in the cost of PPE under IAS 16?

- True or false? Revaluation increases under the revaluation model are always recognised in profit or loss.

- Describe the main difference between the cost and revaluation models for PPE measurement under IAS 16.

- When must borrowing costs be capitalised under IAS 23?

- What conditions must be met for derecognition of a PPE item?

Introduction

Property, plant and equipment (PPE) represent the tangible long-term assets used in business operations. IAS 16 sets out the rules for the recognition, measurement (including subsequent revaluation), depreciation, and derecognition of PPE. IAS 23 addresses borrowing costs, clarifying when interest and similar costs may be capitalised as part of qualifying assets, including self-constructed items of PPE. A solid understanding of these standards is essential for the ACCA exam, often featuring both numerical and discursive questions. Examiners frequently assess whether students can apply rules, select appropriate measurement bases, perform calculations, and explain the effects of revaluations and disposal transactions on the financial statements.

Key Term: property, plant and equipment

Tangible assets that are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes, and are expected to be used during more than one period.Test Tip: When revising Depreciation, revaluation model, and derecognition, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Recognition and Initial Measurement

An item of PPE is recognised as an asset when it is probable that future economic benefits will flow to the entity and its cost can be measured reliably. On initial recognition, PPE is measured at cost.

Cost includes:

- Purchase price (net of discounts and rebates)

- Directly attributable costs to bring the asset to its location and working condition (e.g., delivery, installation, professional fees)

- Initial estimate of dismantling, removal, or restoration obligations

Some costs must not be included:

- General administrative and overhead expenses

- Costs incurred after the asset is ready for use

- Abnormal amounts of wasted material or labour

Key Term: cost model

PPE is carried at cost less accumulated depreciation and accumulated impairment losses. Key Term: revaluation model

PPE is carried at a revalued amount, being fair value at the date of revaluation less subsequent depreciation and impairment.

Subsequent Measurement: Cost or Revaluation Model

After initial recognition, entities may choose either the cost model or the revaluation model for each class of PPE.

- Cost Model: Carry assets at cost less accumulated depreciation and impairment.

- Revaluation Model: Carry assets at fair value (measured reliably) less subsequent depreciation and impairment.

If adopting revaluation, the entire class of assets must be revalued regularly so the carrying amount does not differ materially from fair value at the end of the reporting period.

Accounting for Revaluation Increases and Decreases

- A revaluation surplus (increase) is recognised in other comprehensive income (OCI) and held in a revaluation reserve in equity, unless reversing a prior revaluation deficit in profit or loss.

- A revaluation deficit is recognised in profit or loss, unless reversing a previous revaluation surplus credited to OCI for that asset.

Worked Example 1.1

On 1 January 20X1, Delta acquires a building for $2 million. The useful life is 50 years. On 31 December 20X4, the building is revalued to $3 million. Explain the accounting entries for the revaluation and subsequent depreciation.

Answer:

Carrying amount before revaluation: $2 million less 4 years’ depreciation ($2m/50 × 4 = $0.16m) = $1.84m. Revalued amount: $3m. Revaluation surplus: $3m - $1.84m = $1.16m, recorded in OCI. Future annual depreciation: $3m/46 = $65,217.

Depreciation

Depreciation allocates the depreciable amount (cost less residual value) of PPE systematically over its useful life, beginning when the asset is available for use and ending when it is derecognised.

Key points:

- All PPE with a finite useful life must be depreciated.

- Depreciation must reflect the pattern of consumption of the asset’s future economic benefits (often straight-line, but units of production or reducing balance may be appropriate).

- Useful life and residual value should be reviewed at least annually; changes are accounted for prospectively as a change in accounting estimate.

- Depreciation is charged until the asset is derecognised, even if temporarily idle.

Key Term: depreciation

The systematic allocation of the depreciable amount of an asset over its useful life.

Componentisation

Where significant parts of an asset have different useful lives, each part should be depreciated separately (e.g., aircraft engines and cabin interiors). When a part is replaced, the carrying amount of the replaced part is derecognised, and the cost of the new part is capitalised.

Worked Example 1.2

QuickTravel owns a bus ($100,000) with an engine ($35,000) that must be replaced every 5 years; the body is expected to last 20 years. Depreciation rates are straight line. Calculate annual depreciation and treatment when the engine is replaced at the end of year 5 for $40,000.

Answer:

Annual depreciation: Engine: $35,000/5 = $7,000. Body: $65,000/20 = $3,250. Total: $10,250 p.a. At replacement, the carrying amount of the old engine (zero) is derecognised. The new engine cost is capitalised and depreciated over its new useful life.Exam Warning: Inaccurate separation of components or failure to derecognise replaced parts is a frequent source of exam mistakes. Always identify and account for significant components as required.

Derecognition of PPE

Derecognition occurs when an asset is disposed of or when no future economic benefits are expected from its use or disposal. The gain or loss is calculated as the difference between net disposal proceeds and the carrying amount, and is recognised in profit or loss. If a revalued asset is disposed of, any balance in the revaluation reserve relating to that asset may be transferred to retained earnings.

Key Term: derecognition

The removal of the carrying amount of an asset (or liability) from the statement of financial position.

Worked Example 1.3

Tiger Ltd sells an item of machinery (cost $200,000, accumulated depreciation $120,000) for $90,000. The revaluation reserve from a prior revaluation of this asset stands at $10,000.

Answer:

Carrying amount: $200,000 – $120,000 = $80,000. Gain on disposal: $90,000 – $80,000 = $10,000 (profit or loss). The $10,000 revaluation reserve can be transferred directly to retained earnings.

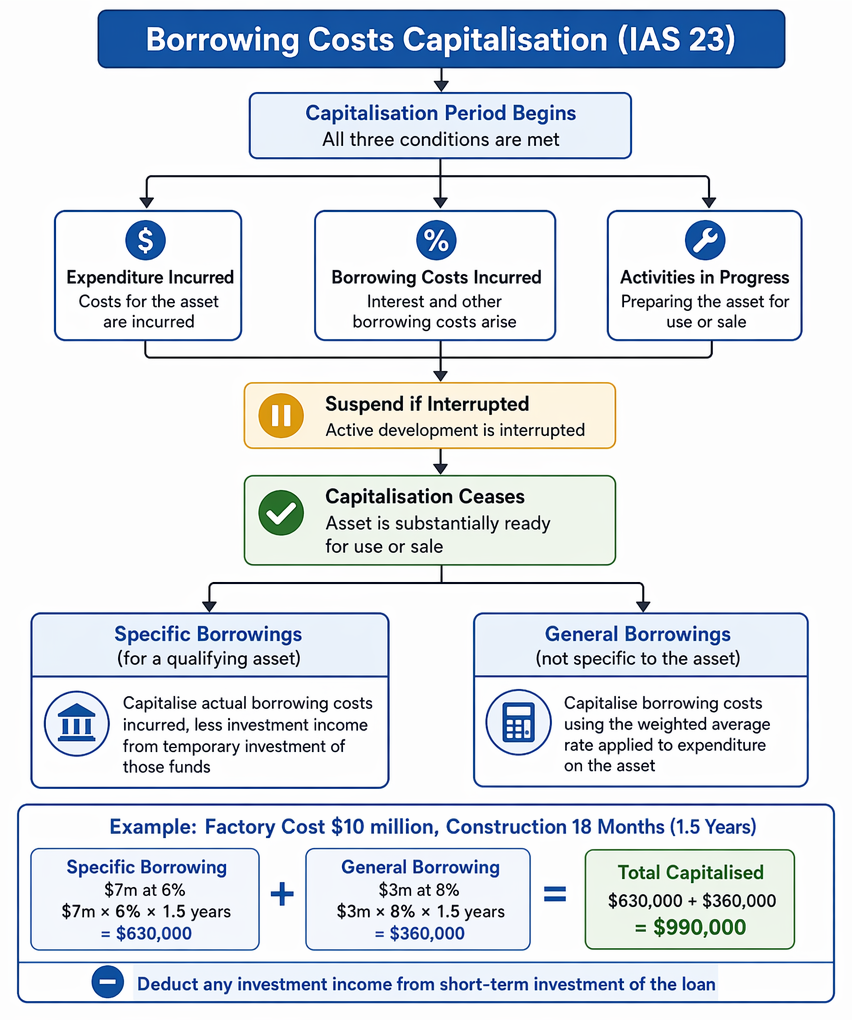

Borrowing Costs (IAS 23)

Borrowing costs are interest and other costs incurred in connection with borrowing of funds. IAS 23 requires that borrowing costs directly attributable to the acquisition, construction, or production of a qualifying asset must be capitalised as part of the cost of the asset.

PPE revaluation accounting under IAS 16 shows how fair value movements affect OCI, profit or loss, and depreciation of revalued amounts.

Key Term: borrowing costs

Interest and other costs incurred by an entity in connection with the borrowing of funds. Key Term: qualifying asset

An asset that necessarily takes a substantial period of time to get ready for its intended use or sale.

Capitalisation Period

Borrowing costs capitalisation begins when:

- Expenditure for the asset is incurred;

- Borrowing costs are being incurred; and

- Activities to prepare the asset for use or sale are in progress.

Suspension is required if active development is interrupted. Capitalisation ceases when the asset is substantially ready for use or sale.

Specific and General Borrowings

- If funds are borrowed specifically for a qualifying asset: Capitalise actual borrowing costs incurred, less investment income from temporary investment of those funds.

- If funded from general borrowings: Capitalise borrowing costs, applying the weighted average rate to expenditure on the asset.

Worked Example 1.4

Ridgeway Co. constructs a factory costing $10 million. $7m is financed by a specific loan at 6%; the remainder is from general borrowings at a weighted average rate of 8%. Construction takes 18 months. Calculate borrowing costs to be capitalised.

Answer:

Specific borrowing: $7m × 6% × 1.5 years = $630,000. General borrowing: $3m × 8% × 1.5 years = $360,000. Total capitalised: $990,000. Any investment income from short-term investment of the loan must be deducted.

Summary

IAS 16 and IAS 23 set clear rules for recognising, measuring, and derecognising PPE and related borrowing costs. After initial recognition at cost, PPE may be measured using either the cost or revaluation model, with significant impacts on reported results and equity. Depreciation policies must reflect the consumption of benefits and be reviewed annually. Assets must be derecognised on disposal, with gains or losses reported in profit or loss. Borrowing costs may be capitalised when they relate to qualifying assets but must be expensed otherwise.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify recognition and measurement requirements for PPE under IAS 16

- Differentiate between the cost and revaluation models for subsequent measurement

- Apply proper depreciation, componentisation, and annual reviews

- Account for revaluation surpluses and deficits

- Recognise and measure borrowing costs for qualifying assets under IAS 23

- Calculate and record gains/losses on derecognition of PPE

Key Terms and Concepts

- property, plant and equipment

- cost model

- revaluation model

- depreciation

- derecognition

- borrowing costs

- qualifying asset