Learning Outcomes

This article explains the core requirements for recognising and measuring property, plant and equipment under IAS 16 and eligible borrowing costs under IAS 23. You will be able to identify when non-current assets should be recognised, detail the components of cost at initial measurement, distinguish between costs that should and should not be capitalised, and apply borrowing cost capitalisation rules to qualifying assets. This knowledge is critical for Strategic Business Reporting (SBR) scenarios.

ACCA Strategic Business Reporting (SBR) Syllabus

For ACCA Strategic Business Reporting (SBR), you are required to understand how to recognise, initially measure and classify property, plant and equipment (PPE), and to determine when borrowing costs can be capitalised. Focus your revision on:

- The criteria for recognising and derecognising PPE under IAS 16

- The measurement of PPE at initial recognition, including which costs are included or excluded

- The requirements for componentisation and treatment of dismantling costs

- The capitalisation of borrowing costs under IAS 23: when it is required, what is a qualifying asset, and start/stop rules for capitalisation

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following should be included in the initial cost of a new factory building?

- a) Site clearance and delivery costs

- b) General administrative salaries

- c) Marketing expenses to advertise products made in the building

- d) Initial operating losses after the factory opens

-

Under IAS 23, which project would typically be a qualifying asset for the capitalisation of borrowing costs?

- a) Purchase of inventory sold within two months

- b) Construction of a new 30-storey office block

- c) Replacement of a company car

- d) Acquisition of land for future, unspecified use

-

If an entity incurs borrowing costs on a loan specific to a new warehouse construction, but suspends work for six months, what should it do regarding capitalisation during that period?

-

Give two examples of costs that should never be included in the initial carrying amount of property, plant and equipment.

Introduction

IAS 16 sets the rules for when property, plant and equipment (PPE) should be recognised as assets and dictates how they must be measured on initial recognition. It also establishes which costs are included in the cost of PPE and which must be expensed immediately. IAS 23 complements this by describing when borrowing costs incurred in constructing or acquiring PPE—or similar assets—must be capitalised and when they must be expensed. Together, these standards define the minimum requirements for bringing non-current tangible assets onto the statement of financial position and for ensuring that only relevant, directly attributable costs are included.

Test Tip: When revising Recognition, initial measurement, and components, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Recognition and Initial Measurement of PPE

IAS 16 defines the conditions that must be met before an item is recognised as PPE. Only assets that bring probable future economic benefits and whose cost can be measured reliably are eligible. PPE is initially recognised at its cost, which must be determined using strict rules about what is and is not capitalised.

Key Term: property, plant and equipment

Tangible items held for use in the production or supply of goods or services, for rental to others, or for administrative purposes and expected to be used over more than one period. Key Term: recognition

Recording an item in the financial statements when it satisfies the relevant criteria of probability of benefit and reliable measurement.

Criteria for Recognition

PPE must be recognised as assets if and only if:

- It is probable that future economic benefits associated with the item will flow to the entity; and

- The cost of the item can be measured reliably.

Expenditure that does not meet both of these criteria is expensed when incurred.

Initial Measurement: Components of Cost

The asset is initially measured at cost. Cost includes:

- Purchase price (including non-refundable taxes, less discounts/rebates)

- Directly attributable costs of bringing the asset to the location and condition necessary for it to operate as intended

- Estimated costs of dismantling and removing the item and restoring the site, if an obligation exists

Key Term: cost

The amount of cash or cash equivalents paid (or the fair value of other consideration given) to acquire an asset at the time of its acquisition or construction, including all costs necessary to bring it to working condition.

Directly attributable costs may include

- Costs of site preparation and delivery

- Installation and assembly

- Professional fees (e.g., architect, engineer)

- Testing to confirm proper functioning (net of any sale proceeds from samples produced)

Certain costs are never included:

- Administrative and general overheads

- Abnormal costs (repairs, wastage, idle time)

- Costs incurred after the asset is available for use, unless they increase economic benefits

- Initial operating losses after the asset is ready for use

- Advertising, staff relocation, or training costs

Key Term: directly attributable costs

Costs that are essential to bringing the asset to the location and working condition for its intended use.

Componentisation and Dismantling

Significant parts of an asset with different useful lives must be accounted for and depreciated separately. If future dismantling or site restoration costs are expected, the present value of these costs forms part of the initial cost of the asset, with a corresponding provision set up.

Key Term: componentisation

Accounting method where significant parts of PPE with different useful lives are recognized, depreciated, and derecognised separately.

Worked Example 1.1

A company buys an item of machinery for £500,000. It pays £10,000 for delivery, £15,000 for installation, and £5,000 to train staff to operate the machine. It must spend £20,000 to dismantle it in 10 years. Calculate the amount to be capitalised.

Answer:

Include the purchase price (£500,000), delivery (£10,000), installation (£15,000), and the present value of dismantling costs (£20,000). Staff training is expensed (£5,000). If the present value of dismantling is £15,000, the total capitalised is £540,000.Exam Warning: In the exam, do not capitalise costs such as staff training or general administration. Explain and justify every cost included in the initial carrying amount based on IAS 16's precise definitions.

Costs Excluded from PPE

Strict separation between capital and revenue expenditure is enforced. The following must not be capitalised:

- General administrative costs, unless directly related to asset construction (rare)

- Overheads not specifically attributable to the acquisition or construction

- Costs after an asset is ready for use (unless they increase future economic benefits)

- Costs of opening a facility or introducing a new product or service

- Costs related to advertising or staff re-training

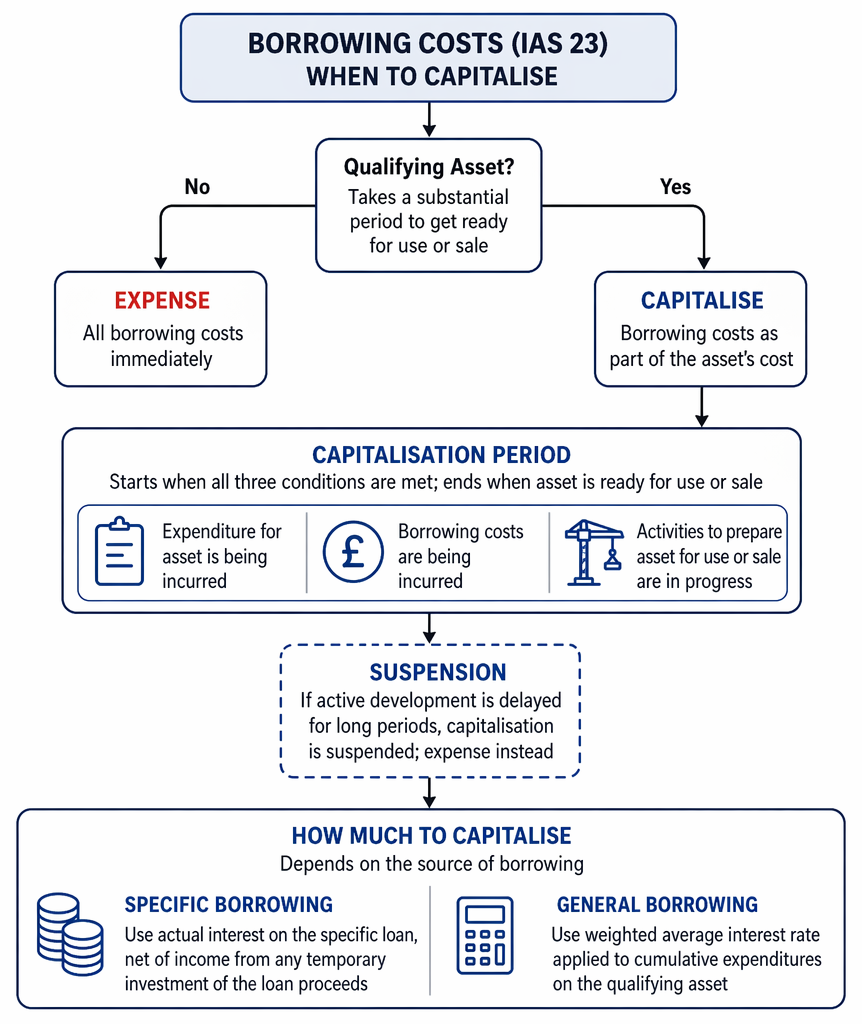

Borrowing Costs (IAS 23)

Borrowing costs are only capitalised when they are directly attributable to the acquisition, construction or production of a qualifying asset. All other borrowing costs are expensed.

Property, plant and equipment cost components comprise acquisition price, attributable preparation costs, restoration provisions, and expenditure recognised immediately in profit or loss.

Key Term: borrowing costs

Interest and other costs incurred by an entity in connection with borrowing funds. Key Term: qualifying asset

An asset that necessarily takes a substantial period of time to get ready for its intended use or sale.

When to Capitalise Borrowing Costs

Borrowing costs that relate directly to a qualifying asset must be capitalised as part of its cost. Examples include major construction projects, such as buildings or production plants. Regular inventory or assets ready for use rapidly are not qualifying assets.

Capitalisation Period

Capitalisation starts when:

- Expenditure for the asset is being incurred

- Borrowing costs are being incurred

- Activities necessary to prepare the asset for use or sale are in progress

Suspension: If active development is delayed for long periods, capitalisation is suspended. Capitalisation ends when the asset is ready for intended use.

Specific vs General Borrowings

- Specific borrowing: If a specific loan is used, capitalise the actual interest net of income from any temporary investment of the loan proceeds.

- General borrowing: Where a project is funded by general borrowings, use a weighted average interest rate, applying it to the cumulative expenditures on the qualifying asset.

Worked Example 1.2

Beta Ltd constructs an office building over 2 years using a specific loan of £4 million at 6% p.a., taken out when construction starts. During a 4-month delay due to permit issues, construction stops. Explain interest capitalisation.

Answer:

For the active construction period, capitalise interest (£4 million × 6% for months of active construction only). During the 4-month suspension, do not capitalise; these costs are expensed.

Worked Example 1.3

Question: Alfa Ltd uses general borrowings (£10 million at 5%) to finance a plant. Total asset expenditure over the year is £4 million. What borrowing costs are capitalised?

Answer:

The capitalised amount is £4 million × 5% = £200,000, using the weighted average rate.

Summary

Under IAS 16, PPE is recognised when probable future benefits exist and cost is measurable. Cost includes purchase price, directly attributable costs, and expected dismantling/restoration costs. General overheads, training, advertising and post-commissioning costs are always expensed. IAS 23 only permits capitalising borrowing costs directly linked to qualifying assets—those taking substantial time to prepare—until the asset is ready for use.

Key Point Checklist

This article has covered the following key knowledge points:

- Define the recognition and initial measurement principles of PPE under IAS 16

- Identify which costs are capitalised as part of PPE and which are always expensed

- Explain the requirements for componentisation and accounting for dismantling obligations

- Determine which assets are qualifying assets under IAS 23

- Apply the rules for capitalising borrowing costs and identifying the start, suspension, and cessation of capitalisation

Key Terms and Concepts

- property, plant and equipment

- recognition

- cost

- directly attributable costs

- componentisation

- borrowing costs

- qualifying asset