Learning Outcomes

After reading this article, you should be able to explain the difference between equity-settled and cash-settled share-based payment awards under IFRS 2. You will understand how to recognise and measure each type, define vesting and performance conditions, and determine how to account for settlement and for changes in estimates. You’ll be able to apply these concepts and calculations to typical ACCA SBR exam scenarios on employee share schemes.

ACCA Strategic Business Reporting (SBR) Syllabus

For ACCA Strategic Business Reporting (SBR), you are required to understand the accounting treatment of share-based payment transactions, both equity-settled and cash-settled, in accordance with IFRS 2. Focus your revision on the following syllabus areas:

- The types and scope of share-based payment transactions covered by IFRS 2

- Recognition and measurement principles for equity-settled share-based payments

- Recognition and measurement principles for cash-settled share-based payments

- The treatment of vesting and non-vesting conditions, including performance conditions

- Re-measurement requirements and treatment of modifications or cancellations

- Disclosure requirements for share-based payment arrangements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is true for the measurement of an equity-settled share-based payment with employees?

- a) It is measured at inherent value at each reporting date

- b) It is measured at grant date fair value

- c) It is measured at settlement date fair value

- d) It is initially measured at cost

-

A company grants cash share appreciation rights (SARs) to its employees, vesting after three years. Which accounting treatment applies under IFRS 2?

- a) Recognise an equity reserve based on grant date fair value

- b) Recognise a liability, remeasured at each reporting date

- c) No accounting entries until settlement

- d) Recognise a fixed expense only at vesting date

-

True or false? Market-based performance conditions affect the number of equity instruments to be recognised over the vesting period.

-

Briefly explain how the accounting differs for an award that can be settled in either equity or cash, at the entity’s choice.

Introduction

Share-based payment schemes, including share options and share appreciation rights, are commonly used to reward employees and other parties. IFRS 2 Share-based Payment sets out how these transactions must be accounted for. A key distinction is made between equity-settled and cash-settled transactions. Knowing how to identify each type and apply the correct recognition and measurement rules is essential for ACCA SBR.

Key Term: Share-based payment

A transaction in which an entity receives goods or services as consideration for equity instruments or incurs liabilities for amounts based on the price of its shares.

Types of Share-based Payment Schemes

IFRS 2 applies when an entity receives goods or services (including employee services) as payment:

- In equity instruments (e.g., shares or share options)

- In amounts of cash based on the price or value of the entity’s shares

These are typically classified as:

- Equity-settled share-based payments

- Cash-settled share-based payments

Equity-settled Share-based Payment

In equity-settled share-based payment transactions, the entity grants equity instruments (such as shares or options) in return for goods or services.

Key Term: Equity-settled share-based payment

A transaction in which the entity receives goods or services as consideration for equity instruments of the entity.

Measurement:

- For employees, measure at the fair value of the equity instruments granted at the grant date.

- For non-employees, if fair value of goods/services can be reliably measured, use this; otherwise, use the fair value of the equity instruments at the date goods/services are received.

- Expense is recognised over the vesting period (if any), based on the best estimate of the number of equity instruments expected to vest.

Recognition:

- Debit to profit or loss (staff cost/expense or asset if appropriate)

- Credit to equity (usually a separate equity reserve, not share capital until exercised)

Cash-settled Share-based Payment

In cash-settled arrangements, the entity grants a right to receive a cash payment based on the value or appreciation in its equity instruments, rather than shares themselves.

Key Term: Cash-settled share-based payment

A transaction in which the entity acquires goods or services by incurring a liability to pay cash or other assets for an amount based on its equity instruments.

Measurement:

- Initially and at each reporting date, measure the liability at the fair value of the amount to be paid, until it is settled.

- Changes in fair value are recognised in profit or loss immediately.

Recognition:

- Debit to profit or loss (staff cost/expense or asset if appropriate)

- Credit to liabilities

Key Term: Vesting period

The period during which all the specified vesting conditions must be satisfied for the counterparty to become entitled to the share-based payment. Key Term: Vesting condition

A condition that determines whether the entity receives the services required, typically through service or performance targets. Key Term: Grant date

The date at which the entity and the counterparty agree to a share-based payment arrangement and have a shared understanding of its terms.

Conditions Affecting Share-based Payments

Vesting and performance conditions impact the number of awards that vest and how expense is recognised.

- Service conditions require the counterparty to complete a specified period of service.

- Performance conditions require achievement of a target (financial or non-financial), sometimes related to the market price of shares.

Market conditions are factored into the grant-date fair value. Non-market vesting conditions affect the number of equity instruments expected to vest.

Worked Example 1.1

On 1 January 20X1, Beta Co grants 1,000 share options to each of 200 employees. The fair value of each option at grant date is $12. The scheme requires employees to stay for 3 years. Beta Co estimates at grant that 10% of employees will leave before vesting. In Year 1, 18 employees leave.

Question: What share-based payment expense should Beta Co recognise for the year ended 31 December 20X1?

Answer:

Expected vesting = 182 employees × 1,000 options = 182,000 options Year 1 expense = 182,000 × $12 × 1/3 = $728,000

Accounting for Modifications, Cancellations, and Settlements

Any modification that increases the fair value of an award must be recognised as an additional expense. If the modification reduces the fair value, no adjustment is made.

If an award is cancelled or settled before vesting, the amount that would have been recognised for services received is recognised immediately.

Differences: Equity-settled vs Cash-settled

| Aspect | Equity-settled | Cash-settled |

|---|---|---|

| Recognition | Credit equity | Credit liability |

| Measurement base | Fair value at grant date (employees) | Fair value of liability at each reporting date |

| Remeasurement | No (except for non-employee revision) | Yes, remeasure at each reporting date |

| Settlement | Increase share capital/equity reserves | Settle liability and reverse equity effect |

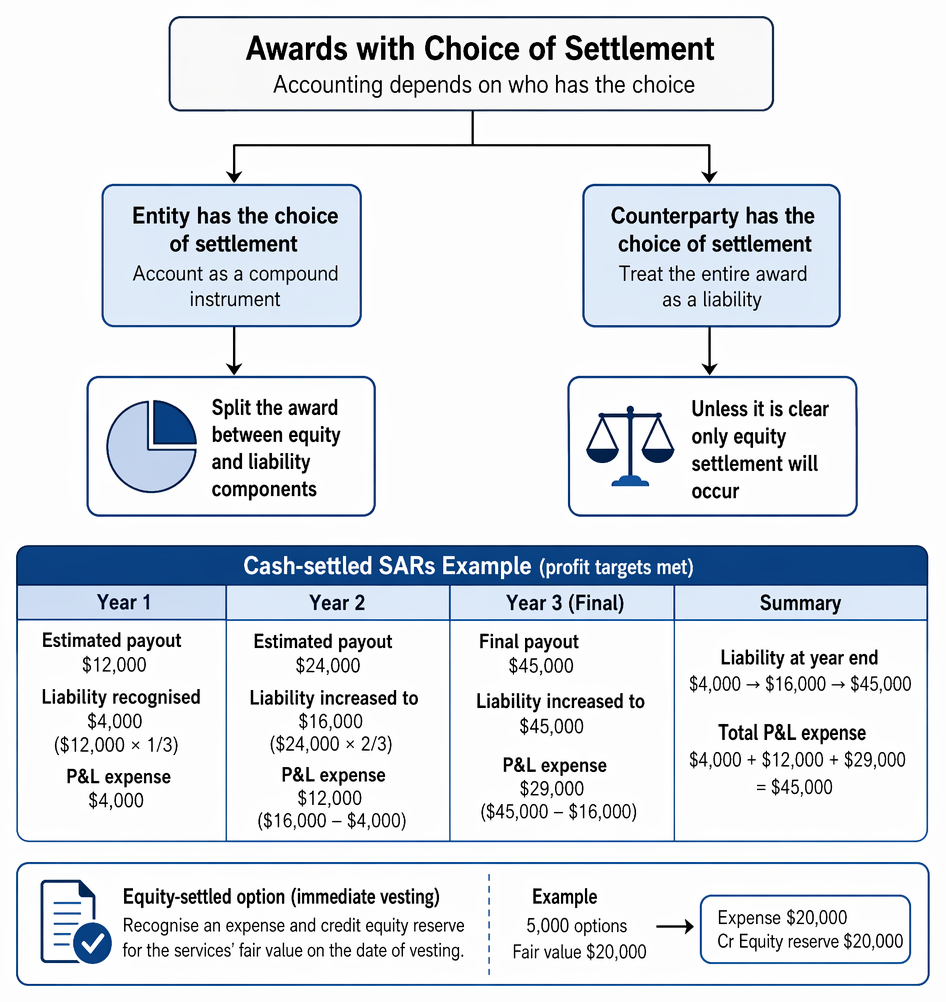

Awards with Choice of Settlement

Some schemes allow either the entity or the counterparty to choose between equity or cash settlement. The accounting depends on who has the choice.

Equity-settled awards use grant-date fair value, recognise expense over the vesting period, revise for non-market forfeitures, and reclassify within equity on exercise.

- If the entity can choose, account as a compound instrument: split the award between equity and liability components.

- If the counterparty can choose, treat the entire award as a liability unless it is clear that only equity settlement will occur.

Worked Example 1.2

Circle Ltd grants senior managers SARs worth up to $50,000 payable in cash (cash-settled) if profit targets are met over three years. The estimated fair value of expected payout is:

- Year 1: $12,000

- Year 2: $24,000

- Year 3: $44,000 (final payout: $45,000)

Question: What amount is recognised as a liability and in profit or loss each year?

Answer:

End of Year 1: Recognise $4,000 ($12,000 × 1/3) Year 2: Liability increased to $16,000 ($24,000 × 2/3); P&L expense is $12,000 ($16,000 - $4,000) Year 3: Liability increased to $45,000 (final); Expense is $29,000 ($45,000 - $16,000)

Worked Example 1.3

On 1 January 20X2, Delta Plc issues 5,000 share options to a consultant in exchange for services, which are reliably valued at $20,000. The options will vest immediately.

Question: How should Delta Plc account for this transaction?

Answer:

Recognise an expense and credit equity reserve for $20,000 on 1 January 20X2 (date of vesting).Exam Warning: In the exam, carefully distinguish equity-settled from cash-settled awards. For equity-settled awards with employees, do not revalue the grant date fair value, except for changes in estimate of the number expected to vest. For cash-settled awards, remeasure the liability at fair value each reporting date.

Revision Tip: If asked to show calculations, always state clearly the number of awards expected to vest and the fair value used. For cash-settled awards, include the movement in liability as an expense each year.

Summary

IFRS 2 requires all share-based payment transactions to be recognised. Equity-settled awards are measured at grant date fair value, with expense spread over the vesting period and a credit to equity. Cash-settled awards result in a liability remeasured at each reporting date, with changes passing through profit or loss. Vesting and performance conditions affect when and how much is recognised. Complex or hybrid schemes need careful analysis to identify the correct accounting treatment.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the difference between equity-settled and cash-settled share-based payments under IFRS 2

- Apply the correct measurement and recognition for both types of award

- State how vesting and performance conditions affect recognition

- Demonstrate how to account for remeasurement and settlement

- Identify the required disclosures for share-based payment arrangements

Key Terms and Concepts

- Share-based payment

- Equity-settled share-based payment

- Cash-settled share-based payment

- Vesting period

- Vesting condition

- Grant date