Learning Outcomes

After reading this article, you will understand how IFRS 2 treats vesting conditions in share-based payment arrangements, identify how different modifications affect accounting, and explain the treatment of cancellations. You will be able to distinguish between service and performance conditions, apply IFRS 2's requirements for accounting when terms or outcomes change, and respond to exam-style scenarios on these topics.

ACCA Strategic Business Reporting (SBR) Syllabus

For ACCA Strategic Business Reporting (SBR), you are required to understand the detailed accounting for share-based payment transactions under IFRS 2, particularly those aspects related to vesting and subsequent changes. This article will help you revise:

- The recognition and measurement of share-based payment transactions

- The nature and accounting effects of vesting conditions (service and performance conditions)

- The accounting treatment of modifications to share-based payment arrangements

- The requirements for cancellations of equity-settled share-based payments

- Revision of how vested and non-vested equity are recognized and adjusted

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A share option is granted, conditional on employees completing three years of service. Which type of vesting condition does this represent?

- a) Market condition

- b) Non-vesting condition

- c) Service condition

- d) Non-market performance condition

-

If an entity increases the number of share options granted (with no change to vesting conditions), how should this modification be accounted for under IFRS 2?

-

True or false? A share-based payment arrangement that is cancelled results in immediate recognition of any remaining amount not yet expensed.

-

Briefly distinguish between a market condition and a non-market performance condition, giving one example of each.

Introduction

Share-based payment arrangements, such as share options granted to employees, are common in modern business. IFRS 2 requires that the fair value of equity instruments granted is recognized as an expense, usually over a vesting period in which services are received. However, detailed rules apply when the right to equity instruments depends on fulfilling certain vesting conditions, or when the terms are changed or cancelled. Knowing how to identify and account for these scenarios is fundamental for ACCA SBR exam success.

Key Term: vesting condition

A requirement that must be fulfilled for the counterparty to be entitled to receive cash, other assets, or equity instruments of the entity under a share-based payment arrangement.Test Tip: When revising Vesting conditions, modifications, and cancellations, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

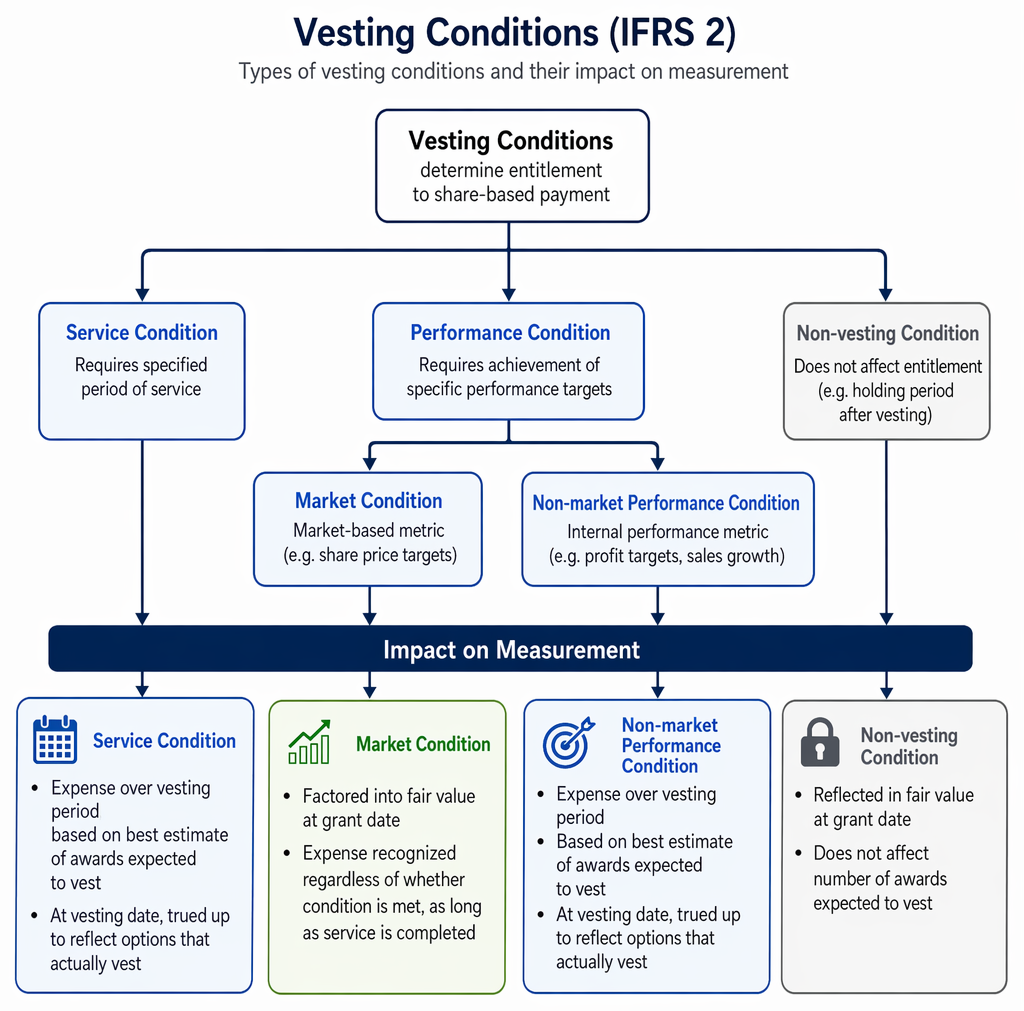

Vesting Conditions

Vesting conditions determine whether an employee or counterparty will become entitled to the share-based payment. They impact both the measurement and timing of expense recognition.

Equity-settled share-based payment expense is measured from grant date through vesting using expected vesting estimates and cumulative recognition under IFRS 2.

Types of Vesting Conditions

Vesting conditions are divided into service conditions and performance conditions.

- Service condition: Requires the employee to complete a specified period of service.

- Performance condition: Requires achieving specific performance targets while possibly also serving a specified period.

Performance conditions are further split into:

- Market conditions: Related to market-based metrics (e.g., share price targets).

- Non-market performance conditions: Related to internal performance metrics (e.g., profit targets, sales growth).

Key Term: service condition

A vesting condition that requires the counterparty to complete a specified period of service. Key Term: performance condition

A vesting condition that requires specified performance targets to be met. Key Term: market condition

A performance target related to the market price of the entity’s equity instruments, such as share price hurdles. Key Term: non-market performance condition

A performance target unrelated to the market price of equity instruments, such as earnings per share or profit goals. Key Term: non-vesting condition

A condition that does not determine whether the counterparty becomes entitled to share-based payment (e.g., holding period requirements after vesting).

Impact on Measurement

Only vesting conditions can affect whether the options vest. Under IFRS 2:

-

Non-market vesting conditions (service, non-market performance):

- Expense is recognized over the vesting period, based on the best estimate of awards expected to vest.

- At vesting date, expense is trued up to reflect options that actually vest.

-

Market conditions:

- Factored into the fair value at grant date; expense is recognized regardless of whether condition is met, as long as service is completed.

-

Non-vesting conditions:

- Reflected in the fair value at grant date; do not affect the number of awards expected to vest.

Worked Example 1.1

Bremner Ltd grants 100 employees 300 share options each, conditional on three years’ service and achieving a cumulative profit target. The grant date fair value is $5 per option. After year 1, 10 employees have left and Bremner estimates a further 10% will leave by year 3. By year 2, actual leavers are 15, and expected total leavers remain 20%. In year 3, the profit target is met and only 18 have left in total.

How much should be recognized as an expense each year?

Answer:

Year 1: 100 employees × 90% expected to stay × 300 × $5 × 1/3 = $45,000 Year 2: 100 × 80% × 300 × $5 × 2/3 = $80,000; Cumulative is $80,000, so year 2 expense = $80,000 – $45,000 = $35,000 Year 3: 82 employees (100 – 18) × 300 × $5 × 3/3 = $123,000; Expense in year 3 = $123,000 – $80,000 = $43,000

Modifications

IFRS 2 defines a modification as any change in terms or conditions of a share-based payment arrangement, including cancellations and settlements.

Types of Modifications

Common modifications:

- Increasing or decreasing the number of instruments

- Changing vesting conditions (e.g., shortening or extending the vesting period, amending performance targets)

- Changing the exercise price

Key Term: modification

A change in the terms and conditions of a share-based payment arrangement.

Accounting for Modifications

Accounting depends on whether the modification is beneficial or not beneficial to the holder:

- If the modification increases the fair value of the equity instruments (or is otherwise beneficial), the incremental value is expensed over the remaining vesting period.

- If the modification is not beneficial (e.g., reduces fair value), ignore the reduction and continue to recognize the original grant-date fair value.

Other key rules:

- If a vesting condition is relaxed (e.g., service period reduced), recognize expense sooner.

- If the vesting condition is made more difficult (e.g., higher performance target), ignore the change unless the award is forfeited.

Worked Example 1.2

Question: An entity grants 500 options at fair value $4 each, vesting after three years of service. After one year, terms are modified to grant each participant an extra 50 options with the same vesting date. Fair value of additional options at grant is $5. How is the modification accounted for?

Answer:

- The original 500 options: account as normal over the 3-year period using original fair value.

- Incremental value: 50 × $5 × number of employees expected to vest; recognize this incremental value over the remaining 2 years (years 2 and 3).

Exam Warning: In the exam, you must correctly identify the type of condition affected—service vs performance, market vs non-market. Improperly adjusting for a change in market conditions (which are recognized only at grant date) is a common exam error.

Cancellations

If an equity-settled share-based payment is cancelled during the vesting period (by the entity or counterparty), IFRS 2 requires immediate recognition in profit or loss of any amount not yet recognized at the cancellation date.

Where new awards are granted to replace cancelled options, these are treated as a new grant, and the fair value of the replacement (plus any unrecognized portion of the original) is expensed over the new vesting period.

Key Term: cancellation

The entity or the counterparty unilaterally terminates a share-based payment arrangement during the vesting period.

Worked Example 1.3

Question: On 1 January 20X1, ClubCo grants employees options vesting in 3 years, with a fair value of $8 each. On 31 December 20X2, the entity cancels all options due to restructuring. Before cancellation, $80,000 had been recognized of the total $120,000 expected cost. What is the correct entry at cancellation?

Answer:

Recognize the unrecognized $40,000 immediately as expense in year 2 (total recognized equals the cumulative grant-date fair value for the number of options expected to vest before cancellation).

Treatment of Forfeitures

Forfeitures occur when vesting conditions are not met (e.g., employees leave before vesting). No expense is recognized for options that do not vest due to failure to satisfy vesting conditions.

However, cancellations are treated differently: any unrecognized cost is immediately recognized. Only actual forfeitures (i.e., failure to satisfy vesting conditions, not a cancellation) reduce the recognized expense.

Summary

IFRS 2 requires careful attention to vesting conditions when measuring share-based payments. Service and non-market performance conditions affect the number of awards expected to vest, while market and non-vesting conditions affect grant-date fair value. Modifications that benefit employees lead to increased expense; adverse modifications are ignored. Cancellations accelerate recognition of any remaining expense. Annual reassessment is essential for non-market vesting conditions.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the difference between service, performance, market, and non-market vesting conditions

- Identify how vesting conditions affect share-based payment expense recognition

- Account for modifications and incremental fair value

- Describe the accounting for cancellations versus forfeitures

- Apply the rules to practical and exam scenarios

Key Terms and Concepts

- vesting condition

- service condition

- performance condition

- market condition

- non-market performance condition

- non-vesting condition

- modification

- cancellation