Learning Outcomes

This article explains how to apply equity valuation multiples and comparables analysis in an exam setting, focusing on CFA Level 1–relevant tools and interpretation. It clarifies the economic intuition behind price-based and enterprise-value-based multiples, including why investors use P/E, P/B, P/S, and EV/EBITDA to express views on growth, profitability, and risk. It distinguishes trailing versus forward multiples, highlighting the data inputs, strengths, and limitations of each, and how forecast assumptions can bias valuation conclusions. It sets out a structured comparables process: defining an appropriate peer group, choosing the most informative multiple for an industry, ensuring consistent metric definitions, and computing and summarizing peer statistics. It discusses how to interpret relative valuation gaps, including when a higher or lower multiple is justified by differences in growth, return on equity, capital structure, or business risk. It details common adjustments and normalizing techniques, such as removing non-recurring items, addressing accounting policy differences, and handling loss-making or highly cyclical firms. It also reviews key practical pitfalls, enabling you to evaluate when multiple-based conclusions are weak, misleading, or require corroboration from other valuation approaches.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand and apply basic valuation multiples for equity analysis, with a focus on the following syllabus points:

- Defining and calculating common price and enterprise value multiples such as P/E, P/B, P/S, and EV/EBITDA

- Interpreting differences in multiples between companies

- Applying the comparables or "market approach" to equity valuation and identifying suitable peers

- Adjusting comparables analysis for key differences between firms (growth, risk, accounting choices)

- Recognizing limitations and potential pitfalls of multiples-based valuation

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the key differences between trailing and forward price/earnings ratios, and how might their interpretations differ?

- When is the use of EV/EBITDA preferred over P/E as a valuation multiple?

- What adjustments might an analyst consider when comparing valuation multiples across peer companies?

Introduction

Equity analysts and investors frequently use valuation multiples and comparables analysis as practical tools to assess whether a stock is fairly valued relative to similar firms. This method, known as the "market approach," relies on the principle that similar companies should be valued similarly if they share comparable growth prospects, risks, and profitability. Multiples provide a snapshot view, offering direct and comparative input for investment decisions and target price setting.

Key Term: multiple

A ratio of a stock’s market price, enterprise value, or market capitalization to an accounting metric such as earnings, book value, or sales.Test Tip: When revising Multiples and comparables analysis, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Rationale for Using Multiples and Comparables

Multiples compress complex valuation models into straightforward ratios, allowing quick direct comparisons across firms. The most common multiples are based on price or enterprise value, normalized by company earnings, book value, revenue, or cash flow.

- Common price multiples: P/E (price-to-earnings), P/B (price-to-book), and P/S (price-to-sales)

- Enterprise value multiples: EV/EBITDA (enterprise value to earnings before interest, tax, depreciation, and amortization)

Multiples reflect investors' willingness to pay for each unit of earnings, assets, or sales. Higher multiples typically imply expectations of faster growth, superior profitability, or lower risk versus peers.

Key Term: comparables (or "comps") analysis

A market-based valuation approach where the value of a company is estimated by comparing its valuation multiples to those of similar public companies.

Forward Versus Trailing Multiples

Multiples can use either historical (trailing) or forecasted (forward) financial data:

- Trailing multiples use historical results, such as the last twelve months' net income or EBITDA, which are objective and verifiable.

- Forward multiples use analyst or management forecasts for the coming year, reflecting market expectations about future performance.

Forward-looking multiples are more relevant when company earnings are volatile or expected to change significantly. However, forward estimates involve more subjectivity and potential bias.

Key Term: P/E ratio (price-to-earnings)

The stock price divided by earnings per share; measures the price investors are willing to pay per unit of current (or future) company earnings. Key Term: EV/EBITDA multiple

Enterprise value divided by earnings before interest, tax, depreciation, and amortization; commonly used to compare capital-structure-neutral valuations of companies with varying debt levels.

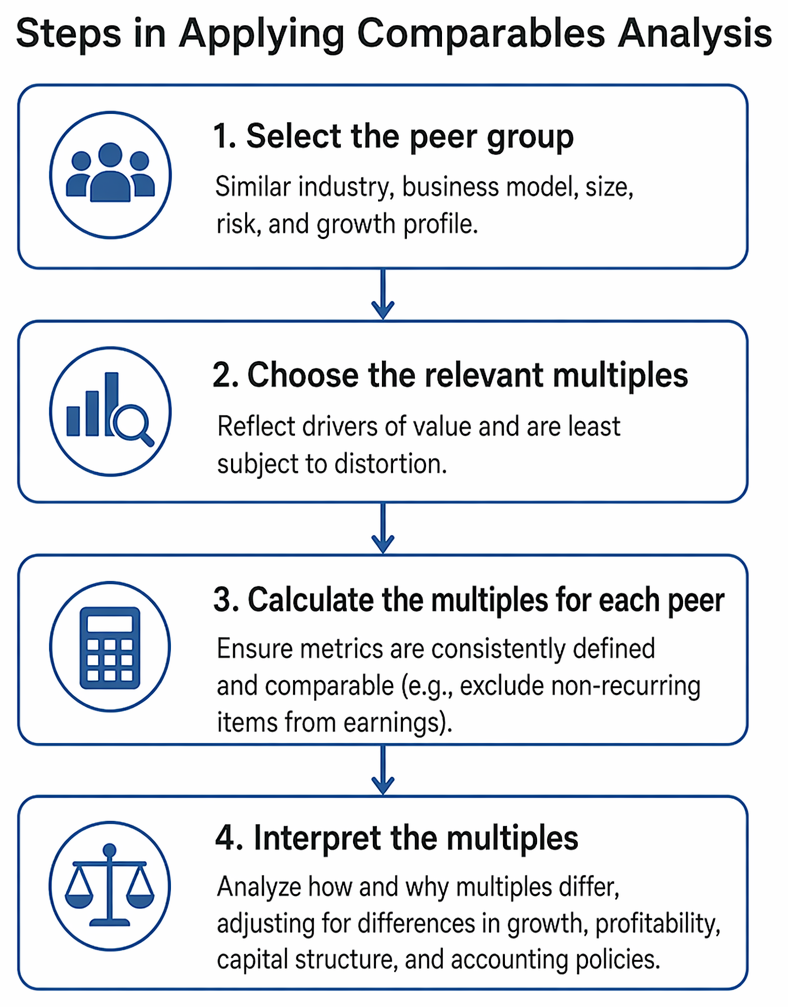

Steps in Applying Comparables Analysis

The comparables approach involves the following main steps:

Relative valuation workflow includes peer identification, consistent multiple computation, peer statistic summary, and analysis of growth, leverage, accounting, and risk differences.

- Select the peer group: Identify companies with similar industry, business model, size, risk, and growth profile.

- Choose the relevant multiples: Decide which ratios best reflect the drivers of value and are least subject to distortion.

- Calculate the multiples for each peer: Ensure metrics are consistently defined and comparable (e.g., exclude non-recurring items from earnings).

- Interpret the multiples: Analyze how and why multiples differ across the group, adjusting for differences in growth, profitability, capital structure, and accounting policies.

Worked Example 1.1

Question: A consumer products analyst is comparing Colgate-Palmolive and Procter & Gamble. Colgate has a P/E of 22x and Procter & Gamble trades at 25x. Both companies have similar debt levels, but Procter & Gamble has higher expected sales growth and a more diversified product portfolio. All earnings are calculated on a forward basis. Should Colgate trade at a lower multiple than Procter & Gamble, and why?

Answer:

Yes. The higher P/E multiple for Procter & Gamble may be justified by superior growth prospects and product diversification, which can lower risk and boost expected future earnings growth. Investors are willing to pay more per dollar of expected earnings for higher quality firms.

Selecting the Right Multiple: P/E vs. EV/EBITDA

The choice of multiple often depends on industry and capital structure differences.

- P/E is widely used and simple, but affected by capital structure (debt levels), non-operating items, and accounting policies.

- EV/EBITDA is less affected by capital structure. It is suitable for comparing firms with different financing or where earnings may be negative (e.g., due to high depreciation) but EBITDA is positive.

Key Term: enterprise value (EV)

The sum of a company's market value of equity, debt, and other interest-bearing liabilities, minus cash and cash equivalents; a measure of total firm value from all capital providers.

Adjustments and Limitations in Comparables Analysis

Strict comparability is rarely possible, and adjustments may be needed for accurate analysis:

- Adjust earnings for non-recurring items (e.g., one-off restructuring charges).

- Control for growth and profitability: Firms with higher growth or returns on equity often command higher multiples.

- Correct for accounting differences: For example, differences in depreciation methods or treatment of leases can impact reported earnings and thus multiples.

- Consider capital structure: Use EV-based multiples if debt levels differ widely.

Key Term: normalizing adjustments

Modifications made to financial statements or metrics to remove non-recurring, unusual, or accounting differences between companies when performing comparables analysis. Key Term: control premium

The additional value an investor is willing to pay for a controlling ownership interest in a company, often above the market price implied by multiples for minority shares.

Key Pitfalls in Using Multiples

- Multiples can be distorted by temporary earnings shocks, accounting policy changes, or market sentiment.

- Peer selection is subjective and may overstate “similarity.”

- Multiples are less meaningful when applied to cyclical or unprofitable companies (e.g., P/E is not defined if earnings are negative).

- Reliance on a single multiple or failure to adjust for clear differences between peers can mislead.

Worked Example 1.2

Question: An infrastructure company (InfraCycle) reports depressed earnings due to a large one-time write-off, giving it a trailing P/E of 80x versus peer average of 18x, but after adjusting for this write-off, its normalized P/E falls to 19x. How should an analyst approach this?

Answer:

The analyst should use the normalized earnings figure and the adjusted P/E multiple for comparison. Using raw trailing P/E without adjustments would be misleading, implying overvaluation that does not accurately reflect ongoing operations.Exam Warning: Be careful using forward-looking multiples: If consensus forecasts are aggressive, P/E or EV/EBITDA ratios may appear low, even if the share is expensive on true, achievable numbers.

Summary

Multiples and comparables analysis are practical, quick-reference valuation tools commonly used in equity analysis. The method rests on the principle that similar companies in comparable industries and environments should command similar valuation measures, after controlling for differences in growth, profitability, and risk. Analysts must choose the relevant multiple, construct an appropriate peer group, and make necessary adjustments for differences. Multiples-based approaches are subject to judgment, and careful consideration must be given to accounting consistency, cyclical swings, and any non-recurring items affecting financial results.

Key Point Checklist

This article has covered the following key knowledge points:

- Understand the use of multiples (P/E, EV/EBITDA, etc.) and comparables analysis for relative equity valuation

- Distinguish between trailing and forward multiples and their applications

- Select and adjust comparables based on peer group, growth, and risk differences

- Recognize the impact of accounting and capital structure differences on multiples

- Be aware of the practical limitations and common pitfalls in using multiples for valuation

Key Terms and Concepts

- multiple

- comparables (or "comps") analysis

- P/E ratio (price-to-earnings)

- EV/EBITDA multiple

- enterprise value (EV)

- normalizing adjustments

- control premium