Learning Outcomes

This article explains duration, convexity, and interest rate risk for debt securities, including:

- Describing how duration quantifies a bond’s price sensitivity to interest rate changes and why it is central to fixed-income risk management.

- Distinguishing Macaulay, modified, and effective duration, and identifying which measure is appropriate for option-free versus option-embedded bonds.

- Interpreting duration values to estimate approximate percentage price changes for small parallel shifts in the yield curve.

- Explaining convexity as the curvature in the price–yield relationship and how it refines duration-based price change estimates for larger yield moves.

- Applying combined duration and convexity measures to compute estimated price changes for both coupon and zero-coupon bonds.

- Analyzing sources of interest rate risk, including price risk and reinvestment risk, and evaluating how bond characteristics affect each component.

- Evaluating how duration aggregates at the portfolio level and how managers use it to control overall sensitivity to interest rate movements.

- Recognizing key assumptions and limitations of duration and convexity measures, particularly with respect to non-parallel yield curve shifts and bonds with embedded options.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the mechanics and implications of interest rate risk for debt securities, with a focus on the following syllabus points:

- Defining and interpreting duration as a measure of bond price sensitivity to yield changes

- Distinguishing Macaulay, modified, and effective duration, and knowing when to apply each

- Explaining convexity and its effect on bond price–yield relationships

- Understanding price risk and reinvestment risk as key interest rate risks

- Applying duration and convexity to estimate price changes for both option-free and option-embedded bonds

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main difference between Macaulay duration and modified duration?

- If a bond has positive convexity, how does the duration-based price change estimate compare to the actual price change after a large yield move?

- Explain the impact of rising interest rates on price risk and reinvestment risk for a coupon bond.

- For which type of bond is effective duration required instead of modified duration?

Introduction

Interest rate risk is the principal market risk faced by holders of most debt securities. Understanding how and why bond prices respond to yield changes—and quantifying this risk—are essential for CFA candidates.

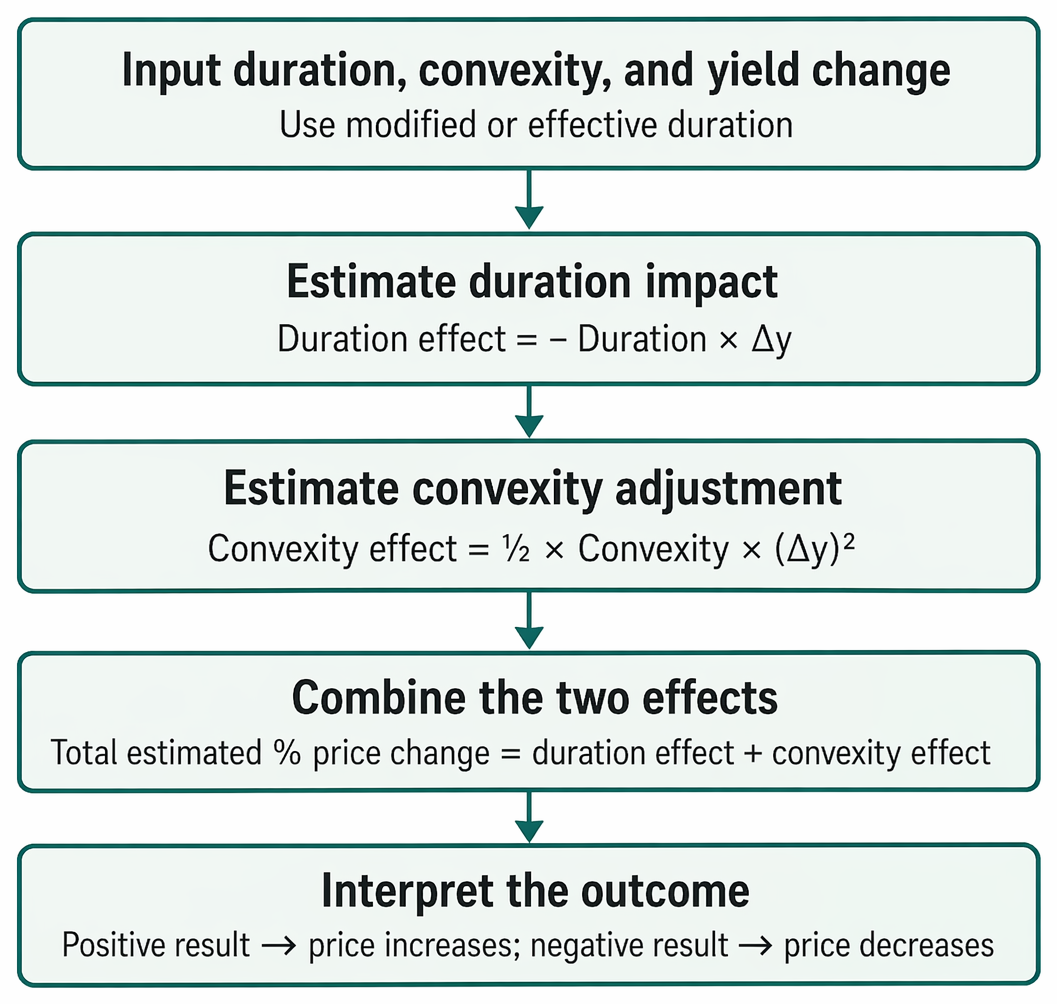

Duration-convexity analysis combines the linear duration term and quadratic convexity term to estimate a bond’s percentage price response to yield shifts.

Test Tip: When revising Duration convexity and interest rate risk, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Nature of Interest Rate Risk

Interest rate risk refers to the possibility that changes in market yields will cause a bond’s price to move in a direction unfavorable to the investor. For fixed-rate bonds, rising yields typically reduce prices, while falling yields increase bond values.

Key Term: interest rate risk

The potential for a bond's price to move unfavorably in response to changes in market yields.

Duration as a Measure of Sensitivity

Duration is the foundational quantitative tool for measuring bond price sensitivity to changes in yields. It serves both as a risk estimate for small changes in rates and as a key input to bond portfolio immunization and risk control.

Key Term: duration

A measure indicating the approximate percentage change in a bond’s price for a 1% change in yield, assuming all other factors remain constant. Key Term: Macaulay duration

The weighted average time (in years) until a bond's cash flows are received, weighted by present value. Key Term: modified duration

The approximate percentage price change of a bond for a 1% change in yield, calculated as Macaulay duration divided by (1 + yield per period). Key Term: effective duration

A duration measure that estimates price sensitivity for bonds with uncertain cash flows (e.g., with embedded options), reflecting price changes given a parallel shift in the yield curve.

Types of Duration and When to Use Them

- Macaulay duration is primarily a time-weighted measure, rarely used directly for risk estimation.

- Modified duration is used for option-free bonds to estimate price changes for small yield changes.

- Effective duration is required for bonds where cash flows depend on interest rates, such as callable, putable, and mortgage-backed bonds.

Interpreting Duration

Modified or effective duration gives the approximate percentage change in full price for a 1% parallel change in yields.

For example, a modified duration of 5 indicates that a 1% rise in yield lowers the bond’s price by about 5%.

Convexity: Accounting for Nonlinearity

Duration provides an estimate that is accurate only for small yield changes. For larger yield changes, price–yield relationships are curved, not straight. Convexity quantifies the curvature in the price–yield relationship.

Key Term: convexity

A measure that quantifies the degree of curvature in the price–yield relationship of a bond, improving the duration estimate for large yield changes.

Effect of Convexity

Bonds with greater positive convexity experience less price loss for yield increases—and greater price gains for yield decreases—than predicted by duration alone.

Worked Example 1.1

A 7-year, 5% coupon bond with a yield to maturity of 3% has a modified duration of 6.0 and a convexity of 50. Estimate the percentage price change for a 1% increase in yield.

Answer:

- Duration estimate: Change ≈ –6.0% (for +1% yield change)

- Convexity adjustment: 0.5 × 50 × (0.01)² = +0.25%

- Total ≈ –5.75% (estimated price falls by 5.75%)

Sources of Interest Rate Risk

Primary interest rate risks when holding debt securities include:

- Price risk: The risk that the bond price falls when yields rise

- Reinvestment risk: The risk that cash flows are reinvested at rates below original expectations

Key Term: price risk

The risk that a bond’s price declines in response to rising yields. Key Term: reinvestment risk

The risk that interim cash flows (coupon or principal repayments) are reinvested at a lower rate than the yield to maturity assumed at purchase.

Duration, Price Risk, and Reinvestment Risk

- Bonds with longer duration are more sensitive to yield changes (more price risk).

- High coupon bonds have lower duration (less price risk, more reinvestment risk).

- Zero-coupon bonds: highest duration (only price risk, no reinvestment risk since no interim payments).

- Price risk and reinvestment risk partially offset each other: rising rates increase reinvestment income but decrease market value; falling rates do the opposite.

Worked Example 1.2

Assume you hold a 10-year zero-coupon bond trading at $620 with a yield of 5%. If yields rise to 6%, estimate the percentage price change using duration, and compare to the actual percentage change.

Answer:

- Modified duration for zero-coupon bond = time to maturity (10 years)

- Estimated price change ≈ –10% for +1% yield.

- Actual change: New price = $558; % change = (558-620)/620 ≈ –10%.

- For zero-coupon bonds, duration estimate closely matches actual.

Exam Warning: For bonds with embedded options (e.g., callable/putable bonds), always use effective duration, not modified duration. Using the wrong measure will NOT be awarded credit.

Convexity and Large Yield Changes

For large yield changes, duration underestimates price increases and overestimates price decreases. Adding convexity correction gives a more accurate estimate.

Worked Example 1.3

A 15-year, 6% coupon bond has an effective duration of 11 and a convexity of 225. Yields fall by 2%. Estimate the price change.

Answer:

- Duration estimate: +11 × 2% = +22%

- Convexity: 0.5 × 225 × (0.02)² = +0.45%

- Total: +22.45% (using both duration and convexity).

Interest Rate Changes and Portfolio Value

Duration is additive for portfolios: weighted average of component durations (by market value). This allows for estimating total portfolio interest rate sensitivity.

Limitations of Duration Measures

- Duration assumes parallel yield curve shifts.

- For steep or non-parallel shifts, duration provides only a rough estimate.

- For large changes, convexity is needed.

Factors Affecting Duration

- Time to maturity (longer maturity = higher duration)

- Coupon rate (higher coupon = lower duration)

- Yield level (higher yield = lower duration)

- Embedded options (lower effective duration due to cash flow variability)

Summary

Duration and convexity are central for assessing interest rate risk of bonds. Duration approximates how much a bond’s price will change with small yield movements, while convexity improves the estimate for larger changes. Bonds with high duration are more exposed to interest rate movements. Reinforcement by convexity is especially important for large rate moves or bonds with option features.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and interpret Macaulay, modified, and effective duration, and when to use each measure

- Apply duration and convexity to estimate bond price changes for interest rate movements

- Explain the effects of convexity and why positive convexity benefits the investor

- Identify and compare price risk and reinvestment risk as elements of interest rate risk in bonds

- Recognize key limitations when using duration for risk assessment, especially for bonds with embedded options

Key Terms and Concepts

- interest rate risk

- duration

- Macaulay duration

- modified duration

- effective duration

- convexity

- price risk

- reinvestment risk