Learning Outcomes

This article explains how to define, calculate, and interpret core yield measures for fixed‑income securities, with particular emphasis on current yield and yield to maturity (YTM). It clarifies how each measure is derived, what it captures about a bond’s return, and the limitations of using current yield versus YTM in valuation and comparison questions. The article explains the inverse relationship between bond prices and yields, the shape of the price–yield curve, and why convexity causes asymmetric price changes for equal yield moves. It also explains how maturity, coupon rate, and duration drive a bond’s price sensitivity to changes in market interest rates, highlighting which bonds exhibit the greatest interest rate risk. In addition, the article explains how premium and discount prices relate to a bond’s coupon rate, current yield, and YTM, and how yield changes reflect shifts in required return, inflation expectations, and credit risk. Throughout, the focus is on applying these yield and price concepts to typical CFA Level 1 question formats, including qualitative reasoning about direction and relative magnitude of bond price movements.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the major ways yields are measured for debt securities and how bond prices and yields move in relation to each other, with a focus on the following syllabus points:

- Define, calculate, and interpret current yield and yield to maturity (YTM) for bonds

- Describe the inverse relationship between a bond’s price and its yield

- Explain why bond price changes are not the same for equal increases and decreases in yield (price–yield convexity)

- Analyze how changes in market interest rates affect the value of debt securities

- Identify factors affecting the price sensitivity (duration) of bonds

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the effect on a bond’s price if its yield to maturity increases, assuming all else is constant?

- How does the price change of a bond differ for equivalent increases and decreases in yield?

- If a bond is trading below par, what can you say about its current yield versus its coupon rate?

- Briefly explain the impact of maturity and coupon rate on a bond’s price sensitivity to yield changes.

Introduction

Yield measures and the price-yield relationship are foundational concepts in fixed income analysis. Understanding how to calculate a bond’s yield, and how yields and prices move in opposite directions, is essential for both valuation and risk management. As a CFA candidate, you will be expected to compute and compare key yield measures such as current yield and yield to maturity (YTM) and to interpret the practical implications of these yields for market pricing and interest rate risk.

Key Term: Current yield

The annual coupon payment of a bond divided by its current market price; a simple indicator of a bond’s income return. Key Term: Yield to maturity (YTM)

The internal rate of return on a bond, assuming it is held to maturity and all coupons are reinvested at the same rate; incorporates all cash flows and current price.Test Tip: When revising Yield measures and price yield relationship, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Major Yield Measures

The two most commonly referenced yields on conventional fixed coupon bonds are current yield and yield to maturity (YTM):

- Current yield: Current yield shows the annual income return in relation to the bond's market price. It does not account for price gains or losses due to amortization or for time value of money.

- Yield to maturity (YTM): YTM is the discount rate that makes the present value of the bond’s cash flows equal to its current market price. It considers all future coupon payments, the redemption at maturity, and the price at which the bond is currently trading.

Worked Example 1.1

A 5-year bond with a $1,000 face value pays a 6% annual coupon and is trading at $970. Calculate the current yield and the yield to maturity (conceptually, not by full calculation).

Answer:

- Current yield = $60 / $970 ≈ 6.19%.

- The YTM will be higher than 6.19% because the investor also gains $30 (the difference between $1,000 and $970) by holding to maturity. The exact YTM requires solving for the discount rate that equates the bond’s price to the present value of all cash flows.

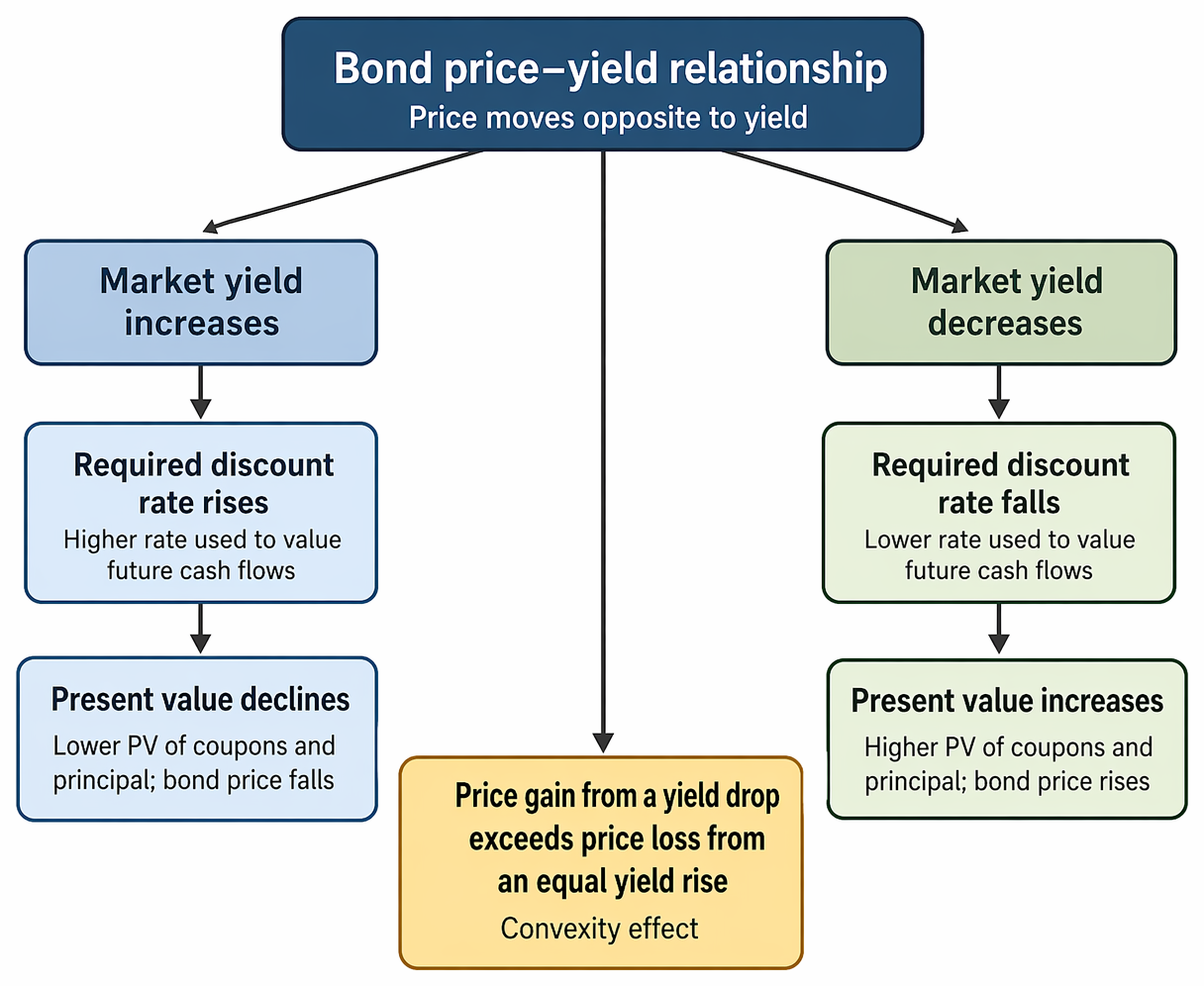

Price–Yield Relationship

One of the most fundamental principles in bond valuation is the inverse relationship between price and yield: when market yields rise, bond prices fall, and when market yields fall, bond prices rise.

Market yield increases reduce bond present value and price, while equal yield declines produce larger gains because of convexity.

Key Term: Price-yield relationship

The mathematical and graphical relationship in which a bond’s price moves inversely to changes in its required yield to maturity.

- The present value of all future cash flows (coupons and principal) decreases as the discount rate (market yield) increases, and vice versa.

- For a given change in yield, the price increase from a yield decrease is larger than the price decrease from an equivalent yield increase—this is called convexity.

Key Term: Convexity

The property of a bond’s price-yield curve that results in larger price gains for a drop in yields than price losses for an equal yield rise; a measure of the curvature in the price-yield relationship of bonds.

Worked Example 1.2

Question: A 10-year, 5% annual coupon bond is trading at par ($1,000). If market yields rise to 6%, what happens to the bond’s price? What if yields fall to 4%?

Answer:

- If yields rise to 6%, the bond price falls below $1,000.

- If yields drop to 4%, the price rises above par.

- The price increase when yields fall by 1% is greater than the price decrease when yields rise by 1% (due to convexity).

Factors Affecting Price Sensitivity to Yield Changes

Not all bonds react the same way to yield changes. Key factors:

- Maturity: The longer the maturity, the greater the price sensitivity to changes in yield (higher duration).

- Coupon rate: Lower coupon rates result in greater price sensitivity (higher duration).

- This means that all else equal, long-term, low-coupon bonds have the greatest price risk from changes in yields.

Worked Example 1.3

Bond A: 4-year, 8% coupon; Bond B: 10-year, 5% coupon. All else equal, which bond will have a greater price drop if yields rise 1%?

Answer:

Bond B will experience a larger price decline, as it has both a longer maturity and a lower coupon rate, making it more sensitive to changes in yield.

Premium and Discount Bonds: Yield Relationships

- If a bond’s price is above par (premium), its current yield and YTM are both lower than its coupon rate.

- If a bond’s price is below par (discount), its current yield and YTM are higher than its coupon rate.

Exam Warning: When answering CFA Level 1 questions, do not assume current yield equals coupon rate unless the bond is trading at par. Be careful not to confuse current yield with YTM—they are different, especially when bonds trade away from par value.

Interpreting Yield Changes in the Market

- Yield changes reflect shifts in required return due to changes in prevailing interest rates, inflation expectations, other risk premia, or issuer-specific credit risk.

- Interest rate risk (or market risk) is the main driver of volatility in high-quality bonds, while credit risk dominates lower-rated bonds.

- Bond price volatility increases with longer duration and lower coupons, amplifying gains and losses when market yields fluctuate.

Summary

The yield measures most relevant for CFA Level 1 are current yield (annual coupon over price) and yield to maturity (IRR of all cash flows at the current price). Bond prices and yields move in opposite directions; long maturity and low coupon magnify price sensitivity to yield changes. The convexity of the price-yield relationship means that bonds’ price gains from yield drops outweigh losses from equal yield rises. These principles are critical for effective fixed income analysis.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and calculate current yield and yield to maturity for bonds

- Understand the inverse relationship between price and yield

- Explain convexity and why price gains exceed price losses for equal yield changes

- Identify how maturity and coupon influence bond price sensitivity to yield

- Distinguish between current yield and YTM, especially for bonds away from par

- Interpret yield changes, relating price movements to interest rate risk

Key Terms and Concepts

- Current yield

- Yield to maturity (YTM)

- Price-yield relationship

- Convexity