Learning Outcomes

This article explains key options strategies and the major option “greeks” relevant for the CFA Level 1 exam, including:

- Describing and comparing core single‑option positions and multi‑leg strategies (spreads, straddles, strangles, and covered or protected positions) in terms of payoff shape and risk/return characteristics.

- Defining delta, gamma, theta, and vega and interpreting what each greek tells you about directional risk, curvature/convexity, time decay, and volatility exposure for an individual option.

- Explaining how moneyness (in‑, at‑, and out‑of‑the‑money) and time to expiry affect the sign and approximate magnitude of each greek.

- Calculating approximate changes in an option’s value using given greek values and assessing how those changes affect strategy profitability under different market scenarios.

- Aggregating greeks across positions to evaluate total portfolio sensitivity and identify which risk dimensions dominate a given strategy.

- Using delta, gamma, theta, and vega to design or evaluate hedging approaches, including delta‑hedging and volatility‑trading applications commonly tested in CFA Level 1 questions.

- Recognizing how the sign and magnitude of each greek differ for long versus short positions and for different strategies, and using this intuition to quickly eliminate wrong answer choices on the exam.

- Distinguishing between “long volatility” and “short volatility” strategies using vega, gamma, and theta.

- Interpreting exam wording that implicitly describes greek exposures (for example, “profits from big moves in either direction” or “earns income if the price stays in a range”).

- Distinguishing between “long volatility” and “short volatility” strategies using vega, gamma, and theta.

- Interpreting exam wording that implicitly describes greek exposures (for example, “profits from big moves in either direction” or “earns income if the price stays in a range”).

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are required to understand options in constructing risk/return strategies and applying greek sensitivity measures, with a focus on the following syllabus points:

- Describing and evaluating common options strategies (spreads, straddles, combinations).

- Explaining option delta, gamma, theta, and vega, and their economic implications.

- Calculating the greeks for basic positions and using them to explain risk exposures.

- Demonstrating how the greeks inform dynamic hedging and risk management.

- Comparing payoff profiles and risk characteristics of covered and protective positions.

- Distinguishing between directional and volatility‑oriented uses of options.

- Relating moneyness, time to expiry, and volatility to option price and greeks.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A European call option on a stock has a delta of 0.55. Which statement best describes this delta and how a trader might use it?

- a) If the stock price increases by $1, the call price will fall by about $0.55; the trader uses this to measure time decay.

- b) If the stock price increases by $1, the call price will rise by about $0.55; the trader can treat the option as roughly equivalent to 0.55 shares of stock.

- c) If the stock price increases by $1, the call price will rise by about $1.55; the trader can treat the option as one share plus an additional 0.55 share.

- d) If implied volatility rises by 1%, the call price will rise by $0.55; the trader uses this to hedge volatility risk.

-

Which greek primarily measures the sensitivity of an option’s price to changes in the volatility of the reference asset?

- a) Delta

- b) Gamma

- c) Theta

- d) Vega

-

An option position has a large positive gamma. What does this imply for delta hedging?

- a) Delta is stable, so the hedge rarely needs adjusting.

- b) Delta will change quickly as the asset price moves, requiring frequent hedge rebalancing.

- c) Delta is always close to zero, so no hedging is necessary.

- d) Delta is always equal to one, so the position can be hedged with a one‑for‑one stock position.

-

Why is theta typically negative for a long call option on a non‑dividend‑paying stock?

- a) Because higher volatility over time reduces the option’s value.

- b) Because time passing reduces the remaining opportunity for favorable price movements.

- c) Because interest rates normally fall as expiry approaches.

- d) Because the strike price automatically adjusts downward over time.

-

A trader buys a long straddle (long ATM call and long ATM put). At initiation, which combination of greek signs best describes this position?

- a) Positive delta, negative gamma, positive theta, negative vega

- b) Near‑zero delta, positive gamma, negative theta, positive vega

- c) Near‑zero delta, negative gamma, positive theta, negative vega

- d) Positive delta, positive gamma, positive theta, positive vega

-

An investor sells 10 at‑the‑money put options on a stock. Each has a delta of –0.55 (for the long position). Ignoring contract size, what is the approximate net delta sign and directional exposure of the investor’s position?

- a) Delta negative; loses if the stock price falls.

- b) Delta positive; loses if the stock price falls.

- c) Delta negative; loses if the stock price rises.

- d) Delta positive; loses if the stock price rises.

-

A long at‑the‑money call has delta = 0.5, gamma = 0.2, theta = –0.4, vega = 0.3 (per option, per day, per 1% volatility). Which change is most harmful to the option’s value over the next day, holding all else equal?

- a) Stock rises slightly.

- b) Stock is unchanged and time passes.

- c) Implied volatility increases by 1%.

- d) Implied volatility decreases by 1%.

Introduction

Options strategies are used to construct risk/return profiles for a wide range of financial goals. Basic payoff diagrams at expiry are important, but they are only a snapshot. Option values change continuously before expiry as the asset price, volatility, interest rates, and time to maturity change. Managing an options position therefore requires understanding how sensitive the option’s price is to each of these factors.

The most widely used sensitivity measures are the option “greeks.” At CFA Level 1, the focus is on four key greeks:

- delta (directional sensitivity)

- gamma (curvature or convexity)

- theta (time decay)

- vega (volatility sensitivity)

These greeks allow candidates and practitioners to assess risk exposures, adjust hedges, and understand how an option or strategy will behave under small market moves. They are “local” measures: they describe how value changes for very small changes in inputs right now, not what will happen for very large moves or over long horizons.

Key Term: options strategy

An options strategy is a position or combination of options and/or the reference asset designed to achieve a specific risk/return or hedge profile. Key Term: greeks

Greeks are quantitative measures that represent the sensitivity of an option’s price to changes in various factors, including the price of the reference asset, volatility, time to expiry, and interest rates. Key Term: payoff diagram

A payoff diagram is a graph of an option or strategy’s payoff at expiry (on the vertical axis) against the reference asset price at expiry (on the horizontal axis).

For the exam, formulas for the greeks are not required. What is required is a clear understanding of:

- what each greek measures

- the typical sign and magnitude patterns

- how greeks differ for long versus short positions and for different moneyness levels

- how to use greeks to interpret and compare strategies

Level 1 questions about greeks are often:

- purely conceptual (for example, “Which strategy is long volatility?”)

- qualitative numerical (for example, “If delta is 0.4, will the call gain or lose when the stock rises?”)

- simple approximations (for example, “Given delta and vega, estimate the new price after a small change in price and volatility.”)

You are not expected to derive greeks from an option pricing model, but you do need strong intuition about their economic meaning.

Test Tip: When revising Delta gamma theta and vega, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Why Payoff Diagrams Are Not Enough

Standard option questions often show payoff diagrams at expiry. These diagrams capture:

- how the position behaves for large price changes

- the maximum loss and maximum gain

However, they do not reveal:

- how the option will move when the asset price changes slightly today

- how time decay affects the value between now and expiry

- how changes in expected volatility will affect the position

Two options can have the same payoff shape at expiry but very different behaviour before expiry. For example:

- A 1‑month at‑the‑money call and a 6‑month at‑the‑money call have identical payoff diagrams at expiry, but the 6‑month call:

- is more expensive

- has higher vega (more sensitive to volatility)

- has less severe daily time decay (smaller magnitude theta) right now

Payoff diagrams ignore these dynamic aspects. Greeks fill this gap by providing a local, or marginal, view of risk—similar to how marginal product or marginal cost is more informative than total output in microeconomics.

In microeconomics:

- total product shows the total quantity produced with a given amount of input

- marginal product shows how much extra output results from one additional unit of input

Total product alone can be misleading: a firm might have high total output but low productivity compared with competitors. Average and marginal product reveal that difference. Likewise:

- total payoff at expiry shows overall outcome

- greeks show how the option value changes when the asset price, volatility, or time changes slightly

For example, total payoff for a long call is zero below the strike and then increases linearly. Knowing only this diagram does not tell you:

- how strongly the call reacts if the stock moves by $0.50 today (delta)

- whether your directional sensitivity itself will jump if the stock moves (gamma)

- how much value you lose each day if nothing else changes (theta)

- how sensitive your position is to a volatility shock (vega)

Greeks are therefore central to day‑to‑day option risk management and to many exam questions that ask about “small changes” or “immediate impact” of a scenario.

Core Concepts: Moneyness and Volatility

Two concepts strongly influence the greeks and frequently appear in exam questions.

Key Term: moneyness

Moneyness describes the relationship between the current asset price and the option’s strike price: in‑the‑money (ITM), at‑the‑money (ATM), or out‑of‑the‑money (OTM).

-

A call is:

- ITM if asset price > strike

- ATM if asset price ≈ strike

- OTM if asset price < strike

-

A put is:

- ITM if asset price < strike

- ATM if asset price ≈ strike

- OTM if asset price > strike

Key Term: exercise value (option)

\quad \text{where } S_0 \text{ is the current asset price and } K \text{ is the strike.}$$ **Key Term: time value (option)** Time value is the portion of an option’s premium above its exercise value, reflecting the possibility of favourable price movements before expiry.

Exercise value is the immediate exercise value of an option:

At any time before expiry:

- Option premium = exercise value + time value.

- Deep ITM and deep OTM options have relatively low time value.

- ATM options usually have the highest time value, because there is a significant probability of finishing either ITM or OTM.

You can think of time value as what you pay for “possibility.” Even a currently OTM option can end up ITM if there is enough time and volatility. That possibility is what time value measures.

Key Term: volatility

Volatility is the standard deviation of returns of the reference asset over a given period; in options, markets usually refer to annualized volatility. Key Term: implied volatility

Implied volatility is the volatility level that, when input into an option pricing model, produces the current market price of the option.

Implied volatility is forward looking. It reflects the market’s expectation of future variability of the asset price. Changes in implied volatility (rather than historical volatility) drive vega profits and losses.

Time value is very sensitive to both time to expiry and implied volatility:

- more time to expiry → more time value

- higher implied volatility → more time value

Moneyness, time to expiry, and volatility together determine both the option’s price and the pattern of its greeks. For most equity options:

-

ATM, longer‑dated options have:

- deltas near ±0.5

- the greatest gamma and vega

- moderate (in magnitude) theta

-

Deep ITM or deep OTM options have:

- deltas near ±1 (deep ITM) or 0 (deep OTM)

- very small gamma and vega

- relatively small theta in absolute value

Recognizing where an option sits on this spectrum is important for quickly inferring greek magnitudes on the exam.

Major Options Strategies

Options can be used to create directional, neutral, or volatility‑based positions. Common strategies include:

- long or short calls and puts: simple bullish or bearish bets

- spreads: combinations of two or more options of the same type

- straddles and strangles: long or short volatility bets using both calls and puts

- covered or protective positions: combining options with the asset

For each strategy, identifying its profit/loss diagram and doing scenario analysis is fundamental, but understanding the strategy’s greeks is essential to managing risk over time and answering many exam questions quickly.

Single‑Option Positions

Single‑option positions are the building blocks for all strategies.

Key Term: long position in an option

A long position in an option means the investor has bought the option and holds the right (but not the obligation) to exercise it. Key Term: short position in an option

A short position in an option means the investor has written or sold the option and has the obligation to deliver if the option is exercised.

Long Call

- View: bullish.

- Payoff at expiry: zero if asset price ≤ strike; increases linearly above the strike.

- Risk/return: limited loss (premium), theoretically unlimited upside.

- Greeks (typical): positive delta, positive gamma, negative theta, positive vega.

More detail:

-

Delta is between 0 and +1.

- Deep OTM call: delta close to 0 (hardly moves when the stock moves).

- ATM call: delta typically around +0.5.

- Deep ITM call: delta close to +1 (moves almost one‑for‑one with the stock).

-

Gamma is positive and largest when the call is near the money, especially as expiry approaches.

-

Theta is negative because time passing erodes time value. For a long‑dated call, daily theta may be small in magnitude; for a near‑expiry ATM call, daily theta can be large.

-

Vega is positive: an increase in expected volatility raises the chance of large favourable moves, increasing the call’s value. Longer‑dated calls have higher vega.

Exam intuition: a long call is long direction, long volatility, long convexity, and short time (because of negative theta).

Short Call

- View: neutral to slightly bearish, expecting limited upside in the asset price.

- Payoff: receives premium; must pay off if the asset finishes above strike.

- Risk/return: limited gain (premium), potentially very large loss.

- Greeks: opposite signs to a long call (negative delta, negative gamma, positive theta, negative vega).

Short calls:

- lose when the asset price rises (negative delta)

- lose from sharp moves in either direction (negative gamma)

- lose when volatility rises (negative vega)

- gain steadily as time passes (positive theta), if the asset price does not move too much

For the exam: any short option is short volatility (negative vega) and usually short gamma, positive theta.

Long Put

- View: bearish.

- Payoff: increases as the asset price falls below strike; zero if above strike.

- Risk/return: limited loss (premium), upside if price falls, bounded above by strike (minus premium).

- Greeks: negative delta, positive gamma, negative theta, positive vega.

Details:

-

Delta is between –1 and 0.

- Deep ITM put: delta ≈ –1.

- ATM put: delta ≈ –0.5.

- Deep OTM put: delta ≈ 0.

-

Gamma and vega are positive, just like for a long call.

-

Theta is negative for the same reason as for a call: time value decays.

A long put is the mirror image of a long call in directional terms (it benefits from price falls) but has a very similar convexity and volatility profile.

Short Put

- View: neutral to slightly bullish, willing to buy the asset if it falls.

- Payoff: earns premium if the asset stays above strike; suffers loss if price falls below strike.

- Risk/return: limited gain (premium), substantial downside if price collapses.

- Greeks: opposite of a long put (positive delta, negative gamma, positive theta, negative vega).

A short put:

- gains from mild price increases or stability (positive delta, positive theta)

- is hurt by sharp downward moves (negative gamma, downside exposure)

- is hurt by volatility increases (negative vega)

Exam language such as “willing to buy the stock if it falls below the strike” or “generating income when comfortable owning the stock on a dip” usually points to selling puts.

Knowing the sign of each greek for these basic positions is a powerful way to reason through more complex strategies under exam pressure.

Quick Sign Summary for Single Options

For European options on non‑dividend‑paying stocks:

- Long call: Δ > 0, Γ > 0, Θ < 0, vega > 0

- Short call: Δ < 0, Γ < 0, Θ > 0, vega < 0

- Long put: Δ < 0, Γ > 0, Θ < 0, vega > 0

- Short put: Δ > 0, Γ < 0, Θ > 0, vega < 0

Remember: short positions flip the sign of every greek relative to the corresponding long position.

Spreads

Key Term: spread strategy

A spread is a combination of two or more options of the same type (all calls or all puts) on the same reference asset and expiry, but with different strike prices.

Spreads use long and short options to modify payoffs and reduce cost. They typically:

- cap both maximum profit and maximum loss

- reduce net vega, gamma, and theta compared with an outright long option

- retain a directional bias (bullish or bearish)

Bull Spread

-

Construction (call bull spread): buy a lower‑strike call and sell a higher‑strike call with the same expiry.

-

View: moderately bullish.

-

Payoff:

- profit if the asset price rises moderately

- upside profit capped at (higher strike − lower strike − net premium)

- downside loss limited to net premium paid

-

Greeks:

- net positive delta (bullish), smaller magnitude than an outright long call

- net positive gamma (long convexity), but smaller than for a single long call

- net vega usually smaller than for an outright long call because the short call offsets some vega

- theta can be slightly negative or slightly positive depending on exact strikes and moneyness; often mildly negative when constructed with both options near the money

There is also a put bull spread (long higher‑strike put, short lower‑strike put). It has similar risk/return and greek properties but with puts instead of calls. Put‑call parity ensures that, with appropriate strikes and financing, call and put bull spreads are economically similar.

Key exam point: compared with a lone long call, the bull spread:

- requires less premium

- has lower vega and gamma exposure

- limits both upside and downside

Bull spreads are directional trades with reduced exposure to volatility and convexity.

Bear Spread

- Construction (put bear spread): buy a higher‑strike put and sell a lower‑strike put with the same expiry.

- View: moderately bearish.

- Payoff: profit from a moderate fall in the asset price; gains and losses both limited.

- Greeks:

- net negative delta (bearish)

- positive gamma (long convexity)

- reduced vega and theta exposure compared with an outright long put

There is also a call bear spread (long higher‑strike call, short lower‑strike call). Again, the key is that spreads trade some potential profit for lower net greeks, especially lower vega and lower magnitude theta.

On the exam, wording such as “seeks to profit from a moderate rise/fall in the stock while limiting both upside and downside” usually indicates a vertical spread (bull or bear).

Straddles and Strangles

Key Term: straddle

A straddle is a combination of a call and a put on the same reference asset, with the same strike price and expiry. Key Term: strangle

A strangle is a combination of a call and a put on the same reference asset and expiry, but with different (usually out‑of‑the‑money) strikes.

These strategies are classic tools for trading volatility rather than direction.

Long Straddle

- Construction: buy an ATM call and an ATM put with the same strike and expiry.

- View: expecting a large price move in either direction (high volatility), unsure of direction.

- Payoff: loses if the asset price stays near the strike; profits if price moves significantly up or down.

Breakeven prices (ignoring time value at expiry):

-

Upper breakeven ≈ strike + total premium paid.

-

Lower breakeven ≈ strike − total premium paid.

-

Greeks at initiation:

- delta: approximately zero (call’s positive delta plus put’s negative delta)

- gamma: large positive (both options are long gamma)

- theta: large negative (sum of both options’ negative theta)

- vega: large positive (sum of both options’ positive vega)

A long straddle is the classic long‑volatility strategy: positive gamma and positive vega paid for by large negative theta. It benefits from either:

- large realized price moves (in either direction), or

- an increase in implied volatility (even if price does not move much).

Long Strangle

-

Construction: buy an OTM call and an OTM put with different strikes but same expiry (for example, a call with strike above spot and a put with strike below spot).

-

View: similar to a straddle (bet on volatility), but with lower cost and a wider “dead zone.”

-

Payoff:

- lower upfront cost than a straddle

- needs a larger move in either direction to become profitable

- breakeven points further from the current price

-

Greeks: similar signs to the straddle but smaller magnitudes:

- delta: near zero at initiation

- gamma: positive but lower than for a straddle

- theta: negative but smaller in magnitude than for a straddle

- vega: positive but smaller than for a straddle

Short versions (short straddle, short strangle) are mirror images:

- short volatility (negative vega)

- short gamma

- positive theta

They earn small, steady profits when the market is quiet but are exposed to large losses when the asset price moves sharply or volatility spikes. Descriptions like “collecting premium while expecting low volatility” usually refer to such strategies.

Covered and Protective Positions

Covered Call

Key Term: covered call

A covered call is a strategy where an investor holds the asset and sells a call option on that asset.

-

Construction: hold the stock and sell a call on that stock (same number of shares as the call exposure).

-

View: mildly bullish to neutral; willing to sell the stock at the strike if it rises.

-

Risk/return:

- downside risk similar to stock (partly offset by premium)

- upside capped at strike plus premium

- premium provides limited downside buffer

-

Greeks:

- stock has delta +1; short call has negative delta (between 0 and –1). Net delta is positive but less than +1.

- combined gamma is negative (from short call), because the stock has zero gamma.

- vega is negative (short volatility).

- theta is positive: the short call gains from time decay.

A covered call thus:

- softens small losses if the stock drifts sideways (premium income)

- gives up some upside potential

- introduces negative gamma and negative vega

On the exam, covered calls are typically associated with:

- income enhancement when the investor is mildly bullish or neutral

- willingness to sell the stock at the call strike

- a short‑volatility profile

Protective Put

Key Term: protective put

A protective put is a strategy where an investor holds the asset and buys a put option on that asset to insure against downside risk.

-

Construction: hold the stock and buy a put.

-

View: bullish on the stock’s long‑term prospects but wanting downside protection.

-

Risk/return:

- downside limited (floor roughly at strike minus net premium)

- upside similar to stock (minus the cost of the put)

- the put premium is like an insurance premium

-

Greeks:

- stock delta +1; long put has negative delta. Net delta remains positive but closer to zero around the put strike.

- gamma is positive (from the long put).

- vega is positive: benefits from volatility rising.

- theta is negative: the long put loses time value.

Protective puts are “insurance‑like” strategies: they trade negative theta (insurance cost) for positive gamma and vega (protection in adverse moves and benefit from rising risk). An exam question describing a “floor” or “minimum value” on a stock position is usually pointing to a protective put.

On the exam, questions often ask:

- which strategy a risk‑averse investor holding a stock should use to protect against downside risk (answer: protective put)

- which strategy is suitable for an investor holding stock who expects it to remain range‑bound and wants additional income (answer: covered call)

Option Greeks Overview

The greeks quantify how an option’s price responds to small changes in factors affecting its value. The main greeks to understand for CFA Level 1 are delta, gamma, theta, and vega. Each greek is defined for a single option, but portfolio greeks are simply the sum across all positions.

From a calculus viewpoint, greeks are partial derivatives of the option price with respect to key variables (price, volatility, time). At Level 1, the intuition and qualitative patterns are far more important than any mathematical derivations. However, thinking of delta as a slope and gamma as curvature can anchor your intuition.

Delta

Key Term: delta

Delta is the expected change in an option’s price for a small change in the price of the reference asset, holding all else constant.

Delta measures directional exposure:

-

For a call option:

- delta ranges from 0 (deep OTM) to +1 (deep ITM)

- ATM European calls typically have delta around +0.5

-

For a put option:

- delta ranges from –1 (deep ITM) to 0 (deep OTM)

- ATM European puts typically have delta around –0.5

Key Term: delta of a portfolio

Portfolio delta is the sum of individual position deltas, each multiplied by the number of contracts and contract size.

Key interpretations:

-

Delta as share equivalent: A call with delta 0.52 behaves roughly like owning 0.52 shares of the stock; a put with delta –0.40 behaves like shorting 0.40 shares. This interpretation is very important for delta hedging and for quickly estimating profit and loss from small price moves.

-

Sign matches directional view for long options:

- long call: positive delta (benefits from price increases)

- long put: negative delta (benefits from price decreases)

-

Short options invert the sign: A short call has negative delta of the same magnitude as a long call, and a short put has positive delta.

Under some option pricing models, the delta of a call on a non‑dividend‑paying stock can also be interpreted as the risk‑neutral probability that the option expires in‑the‑money, but Level 1 does not require this interpretation.

Delta and Moneyness

Moneyness is the main driver of the delta value and sign:

-

Call options:

- deep ITM call: delta ≈ +1 (moves almost one‑for‑one with stock)

- ATM call: delta ≈ +0.5

- deep OTM call: delta ≈ 0 (very insensitive to small price changes)

-

Put options:

- deep ITM put: delta ≈ –1

- ATM put: delta ≈ –0.5

- deep OTM put: delta ≈ 0

As time passes, delta becomes more “binary” near expiry:

- a call that is slightly ITM close to expiry has delta very close to +1

- a call that is slightly OTM close to expiry has delta very close to 0

So near expiry, deltas of near‑the‑money options can change very quickly as the asset price crosses the strike. This is one reason gamma becomes very large for near‑expiry ATM options.

Delta and Directional Risk

Delta tells you:

- how much you gain or lose for a small move in the asset price today

- whether your position is effectively long or short the asset

For example:

- A long call with delta 0.4 on 1,000 shares behaves like +400 shares.

- A short put with delta +0.3 on 1,000 shares behaves like +300 shares (bullish).

- A covered call (long 1,000 shares, short call delta 0.6 on 1,000 shares) behaves like +400 shares.

This “share equivalent” view is exactly what traders use to hedge.

Delta Hedging

Key Term: delta hedging

Delta hedging is adjusting a position in the reference asset to offset the net delta of an options position, aiming to reduce sensitivity to small price changes. Key Term: dynamic hedging

Dynamic hedging is the process of frequently adjusting hedge positions (for example, in the reference asset) to maintain target risk characteristics, such as delta‑neutrality, over time. Key Term: delta‑neutral position

A delta‑neutral position is one whose net delta is approximately zero, so its value is relatively insensitive to small short‑term changes in the asset price.

Examples:

- If a trader holds options with total delta of +500 (equivalent to owning 500 shares of the stock), they can hedge asset price risk by shorting 500 shares.

- If portfolio delta is –250, buying 250 shares creates a delta‑neutral portfolio.

Delta hedging neutralizes first‑order price risk: the portfolio is approximately unaffected by small up or down moves in the asset price. However, delta itself changes as the asset price moves, which is where gamma becomes important.

Note the difference versus portfolio variance in modern portfolio theory:

- variances and covariances combine non‑linearly and depend on correlations

- deltas combine linearly: portfolio delta is a simple sum of position deltas

This makes delta hedging computationally straightforward. In practice, delta hedges can be implemented using:

- the asset itself (e.g., stocks), or

- closely related instruments (e.g., stock index futures to hedge index options)

For the exam, you only need the basic idea: choose the number of units of the asset so that total delta ≈ 0.

Gamma

Key Term: gamma

Gamma is the rate of change of delta with respect to changes in the reference asset’s price. It is the second derivative of the option price with respect to the asset price.

Gamma measures the curvature or convexity of the option’s value with respect to the asset price.

Key Term: convexity (in options)

Convexity in options refers to the property that gains accelerate and losses decelerate as the asset price moves, associated with positive gamma.

Key sign patterns:

- Long calls and long puts have positive gamma.

- Short calls and short puts have negative gamma.

- The asset itself (stock, index) has zero gamma.

Gamma is:

- highest for ATM options

- higher for shorter‑term options, especially very near expiry

- very small for deep ITM or deep OTM options

Gamma and convexity are closely analogous to bond convexity in fixed‑income analysis:

- A bond with higher convexity has more curvature in its price‑yield relationship and tends to benefit more from interest‑rate volatility.

- An options position with positive gamma tends to benefit from asset price volatility: gains on large moves up are larger than losses on large moves down (for a roughly delta‑hedged position).

Interpretation:

-

High positive gamma:

- as the market moves in your favour, your delta moves in the same direction, increasing your exposure to further favourable moves

- as the market moves against you, delta moves in the opposite direction, reducing your exposure

-

High negative gamma:

- delta changes in a way that tends to increase losses when the market moves against you

- short‑gamma positions can lose money rapidly in volatile markets

Gamma is critical in hedging:

- A position with high gamma requires frequent rebalancing of the delta hedge as the asset price changes.

- A position with low gamma can be hedged with less frequent adjustments.

Qualitatively, you can think of gamma as measuring whether the payoff diagram between now and expiry is “curved” (options) or “straight” (stock, forwards). Positive gamma means favourable curvature.

Theta

Key Term: theta

Theta is the expected change in an option’s value for a small decrease in the time to expiry, holding all else equal. It measures the effect of the passage of time on an option’s price.

Theta measures time decay:

- Often expressed per day: a theta of –0.05 means the option loses about $0.05 of value per day, all else equal.

- Time decay generally accelerates as expiry approaches, particularly for options near the money.

General patterns:

-

Long options (call or put) usually have negative theta:

- as time passes, there is less time for a large favourable move

- the time value component decays to zero by expiry

-

Short options usually have positive theta:

- the option writer benefits from time value decay and hopes the option expires worthless

Theta magnitude:

- largest in absolute value for ATM options with short time to expiry (where time value is high but remaining time is small)

- smaller in absolute value for:

- deep ITM and deep OTM options (little time value)

- very long‑dated options (time is long, so daily decay is slower)

At expiry, theta effectively goes to zero because there is no time left; time value is gone and only exercise value remains.

Special cases (advanced intuition, rarely tested):

- For certain American options on dividend‑paying stocks or deep ITM options, local theta can be slightly positive in some regions, reflecting optimal early exercise considerations. For Level 1, the main rule is sufficient: long options tend to have negative theta; short options tend to have positive theta.

Vega

Key Term: vega

Vega is the expected change in an option's value for a small increase in the volatility of the reference asset, holding other factors constant.

Vega measures sensitivity to volatility, usually implied volatility.

Key points:

-

Long calls and long puts have positive vega:

- if implied volatility rises by 1 percentage point (for example, from 20% to 21%), the option’s value increases by approximately vega.

-

Short options have negative vega:

- option writers lose if volatility rises, because the chance of large moves (and payoffs) increases.

Vega magnitude:

- highest for ATM options

- larger for options with longer time to expiry (more time for volatility to act)

- small for very short‑dated options or very deep ITM or OTM options

Vega is typically quoted per 1 percentage point change in volatility (for example, per 0.01 change in volatility expressed in decimals). If vega = 0.25, a 2‑percentage‑point increase in implied volatility (say, from 20% to 22%) increases the option’s price by approximately $0.50, all else equal.

Because volatility itself can move substantially (for example, before or after earnings announcements or macroeconomic events), vega can dominate profit and loss for strategies such as straddles, strangles, and calendar spreads.

Key Term: long volatility position

A long volatility position is an option or strategy with positive vega (and typically positive gamma) that benefits when implied or realized volatility increases. Key Term: short volatility position

A short volatility position is an option or strategy with negative vega (and typically negative gamma) that benefits when volatility stays low or decreases.

Examples:

- Long call, long put, long straddle, long strangle, protective put → long volatility.

- Short call, short put, covered call, short straddle, short strangle → short volatility.

On exam questions, descriptions such as “benefits from volatility increasing” or “profits from big moves in either direction” point to long‑volatility strategies. Descriptions like “earns premium if the stock stays in a narrow range” point to short‑volatility strategies.

How the Greeks Work Together

For a small change in the asset price and volatility over a short period, the change in an option’s value can be approximated using the greeks. Conceptually:

where:

- = change in option value

- = change in asset price

- = delta

- = gamma

- = vega

- = change in volatility (in decimal form, e.g., 0.01 for 1 percentage point)

- = theta (per unit of time)

- = change in time (in years; for “per day” theta, use 1 day)

For Level 1 purposes:

- Often only delta is used, sometimes combined with vega and theta.

- Gamma is usually discussed qualitatively: “delta will increase (or decrease) as the price moves” rather than via explicit calculations.

Typical exam applications:

- given a delta and a small price move, estimate the price change:

- include vega when a change in implied volatility is specified

- interpret the sign and relative size of greeks to identify risk exposures

Theta and vega effects can offset or complement delta effects. For example:

-

A long call with positive delta and positive vega:

- gains from the asset price rising (delta effect)

- gains from volatility rising (vega effect)

- loses from time passing (negative theta)

-

A short straddle:

- loses from large price moves in either direction (negative gamma)

- loses from volatility rising (negative vega)

- gains from time decay (positive theta)

The key trade‑off in many strategies is between convexity/volatility exposure (gamma and vega) and time decay (theta). Positions with attractive convexity (long gamma, long vega) usually pay for this with negative theta.

Applying the Greeks to Options Strategies

Options strategies combine positions, so total exposure to the greeks is the sum of each position’s greek exposure. For a portfolio:

- portfolio delta = sum of individual deltas (each multiplied by the number of contracts and contract size)

- similarly for gamma, theta, and vega

This linearity is simpler than variance and covariance in portfolio theory, where individual asset risks do not add directly because correlations matter. For greeks, exposures add directly, but the economic risk still depends on how asset prices and volatilities move.

The main risk for each strategy arises from the combination of greeks, which informs the investor’s risk–return trade‑offs.

Worked Example 1.1

You buy an at‑the‑money European call on XYZ stock (spot at $50, strike $50, 3 months to expiry). The call delta is 0.52, gamma is 0.11, theta is –0.08, vega is 0.21. What do these greeks imply for your position?

Answer:

- Delta 0.52: If XYZ stock rises by $1, the call gains approximately $0.52. The option behaves like owning about half a share of the stock, so you have moderate bullish exposure.

- Gamma 0.11: If the stock rises by another $1, delta increases by about 0.11 to 0.63, meaning your position becomes more sensitive to further price moves. This convexity means profits accelerate if the stock continues to rise, and losses decelerate somewhat if it falls.

- Theta –0.08: Each day, your option loses about $0.08 in value from time decay, all else constant. You are paying, in effect, $0.08 per day for the upside potential and convexity that the option provides.

- Vega 0.21: If implied volatility rises by 1 percentage point (e.g., from 25% to 26%), the call gains about $0.21 in value. Your position benefits from volatility increasing. If volatility falls, vega works against you.

This profile (positive delta, positive gamma, negative theta, positive vega) is typical for a long call.

Worked Example 1.2

Suppose you construct a long straddle by buying an at‑the‑money call and an at‑the‑money put on the same stock with the same strike and expiry. How are your greek exposures affected?

Answer:

- Delta: At initiation, the call’s positive delta is roughly offset by the put’s negative delta, so total delta is near zero. The position is initially not directional.

- Gamma: Both options have positive gamma, so the combined position has high positive gamma. Delta will change rapidly as the stock moves, causing the position to become strongly long if the stock rises and strongly short if the stock falls.

- Theta: Both options have negative theta. Adding them together gives large negative theta: you lose from time decay if the stock stays near the strike.

- Vega: Both options have positive vega. The straddle has large positive vega: it gains value if volatility rises, regardless of price direction.

A long straddle is therefore a long‑volatility, long‑gamma, negative‑theta trade: you pay time decay in exchange for exposure to large moves and volatility increases.

Worked Example 1.3

A trader is short an at‑the‑money put, with delta –0.50, gamma 0.13, theta 0.09, vega –0.19 (all per option). What are the risk implications?

Answer:

For a long put, the greeks are: delta –0.50, gamma +0.13, theta –0.09, vega +0.19. For the short put position, the signs reverse:

- Delta +0.50: The short put gains value as the asset price rises (because the put becomes less likely to finish in‑the‑money) and loses value as the asset price falls. A $1 rise in the stock price increases the value of the short position by about $0.50.

- Gamma –0.13: As the stock falls, the put’s delta becomes more negative, so the short seller’s net position becomes increasingly exposed to further declines. Losses can accelerate if the stock drops sharply.

- Theta +0.09: Positive theta means the trader gains about $0.09 per day from time decay. If the stock price does not move much, the trader profits as the option premium erodes.

- Vega –0.19: If volatility falls by 1 percentage point, the put’s price decreases by about $0.19, benefiting the short seller. Conversely, an increase in volatility hurts the trader.

This is a typical short‑volatility, short‑gamma, positive‑theta position: it can earn steady income in quiet markets but is exposed to large losses if the stock falls sharply or volatility spikes.

Worked Example 1.4

You are short 200 European call options on stock ABC. Each contract is on 100 shares. The delta of each call is 0.40. How many shares of ABC must you trade, and in which direction, to create a delta‑neutral position?

Answer:

- Total call exposure = 200 contracts × 100 shares = 20,000 shares.

- Delta per call (long) = +0.40, so total long‑side delta = 20,000 × 0.40 = 8,000.

- Because you are short the calls, your position delta is –8,000 (equivalent to being short 8,000 shares).

- To make the overall position delta‑neutral, you must hold +8,000 shares of stock ABC (go long 8,000 shares).

After buying 8,000 shares, the stock’s delta (+8,000) offsets the option position’s delta (–8,000), leaving portfolio delta approximately zero. You are now hedged against small stock price moves, although gamma and vega risk remain.

Worked Example 1.5

A call option on stock DEF is currently priced at $3.00. Its greeks are: delta 0.60, gamma 0.05, theta –0.02 (per day), vega 0.10 (per 1 percentage point of volatility). Over the next day, the stock price rises by $1 and implied volatility increases by 2 percentage points. Ignoring gamma, what is the approximate new option price?

Answer:

Approximate change in option value ≈ change from delta + change from vega + change from theta.

- Change from delta: $0.60 × $1 = +$0.60

- Change from vega: $0.10 × 2 = +$0.20

- Change from theta for 1 day: –$0.02

- Total approximate change: 0.60 + 0.20 – 0.02 = +$0.78

Approximate new option price = 3.00 + 0.78 = $3.78. In many Level 1 questions, you use this type of simple approximation, focusing on the sign and rough magnitude of each effect rather than exact pricing.

Worked Example 1.6

You hold 1,000 shares of stock GHI and write 10 call option contracts on GHI with a delta of 0.60 each. Each contract represents 100 shares. What is the net delta of this covered call position?

Answer:

- Stock position: 1,000 shares, each with delta +1 → stock delta = +1,000.

- Call options: 10 contracts × 100 shares = 1,000 shares of exposure.

- Long call delta per contract = +0.60; short call delta = –0.60.

- Total option delta from short calls = 1,000 × (–0.60) = –600.

- Net portfolio delta = +1,000 + (–600) = +400.

The covered call behaves like a position that is long 400 shares. Compared with holding 1,000 shares outright, the covered call has reduced directional exposure, is short volatility (negative vega from the short call), and has positive theta.

Worked Example 1.7

Three European call options on the same stock have the same expiry but different strikes. Their deltas are 0.15, 0.52, and 0.90. Which option is deepest in the money, and which is most out of the money?

Answer:

For calls, higher delta indicates a deeper in‑the‑money position.

- The call with delta 0.90 is deepest ITM.

- The call with delta 0.52 is approximately at the money.

- The call with delta 0.15 is far OTM and has the smallest sensitivity to price changes.

Similar reasoning applies to puts but with negative deltas: a put with delta –0.90 is deep ITM, whereas a put with delta –0.10 is far OTM.

Worked Example 1.8

A trader is long a straddle on stock JKL with the following combined greeks: delta 0.05, gamma 0.40, theta –0.30 per day, vega 0.80. What type of market scenario is most favorable for this position over the next month?

Answer:

The straddle has:

- almost zero delta (little directional bias)

- high positive gamma (benefits from large price swings in either direction)

- large negative theta (loses from time decay)

- high positive vega (benefits from volatility rising)

The position is most favorable in a scenario with high realized volatility and/or a rise in implied volatility: large price movements in either direction and increasing volatility expectations that occur quickly enough to offset the time decay. A quiet market with falling volatility would be the worst scenario (theta and vega both negative for the holder).

Worked Example 1.9

You hold a portfolio of options on index MNO with total delta +2,000 and total gamma +50. You want to stay approximately delta‑neutral. If the index rises by 10 points, what is your new approximate delta, and what adjustment is needed?

Answer:

Approximate new delta after a price change is:

- New delta ≈ old delta + gamma × change in price

- New delta ≈ 2,000 + 50 × 10 = 2,000 + 500 = 2,500.

To restore delta‑neutrality (delta ≈ 0), you need to short an additional 2,500 units of the index (or equivalent futures contracts). This example illustrates how positive gamma causes delta to increase as the index rises, requiring re‑hedging. If the index had fallen, delta would have decreased, and you would instead have needed to buy index units to maintain neutrality.

Worked Example 1.10

An investor sells a strangle on stock PQR (short OTM call and short OTM put). The combined greeks are: delta 0.10, gamma –0.25, theta +0.40 per day, vega –0.70. What is the main risk of this strategy?

Answer:

The short strangle has:

- small positive delta (slight bullish bias)

- negative gamma (loses from large price moves in either direction)

- positive theta (earns time decay)

- negative vega (loses if volatility rises)

The main risk is that a large price move or a sharp increase in implied volatility will cause substantial losses, outweighing the steady income from theta. The strategy benefits in quiet markets but is exposed to “tail risk” when the stock moves sharply or volatility spikes. This is the typical profile of a short‑volatility, short‑gamma, positive‑theta strategy.

Exam Warning: On CFA exam questions, always pay careful attention to the sign (positive or negative) of each greek and whether the position is long or short:

- Long call: positive delta, positive gamma, negative theta, positive vega.

- Long put: negative delta, positive gamma, negative theta, positive vega.

- Short call: negative delta, negative gamma, positive theta, negative vega.

- Short put: positive delta, negative gamma, positive theta, negative vega.

Short positions invert the signs of all greeks relative to long positions. This simple rule can help quickly eliminate incorrect multiple‑choice answers.

Also check the moneyness and time to expiry described in the question. A “near‑expiry ATM option” suggests large gamma, large |theta|, and moderate vega; a “deep OTM, long‑dated option” suggests small delta and gamma but meaningful vega.

How Greeks Help Manage Options Risk

Greeks are central to risk management and hedging with options. They are analogous to the concepts of risk and covariance in portfolio theory: instead of variance and correlation, traders monitor deltas, gammas, vegas, and thetas to understand how their portfolio responds to changes in the market environment.

Option value comprises intrinsic and time components, and the time component depends on moneyness, remaining maturity, and implied volatility.

Delta Hedging (risk management)

-

Objective: Neutralize small price movements in the asset by offsetting option delta with a position in the reference asset.

-

Mechanism:

- If portfolio delta is +1,000, short 1,000 shares to create a delta‑neutral position.

- If portfolio delta is –500, buy 500 shares.

-

Practical points:

- Delta hedging is approximate: it is effective for small price moves over short horizons.

- As the asset moves, delta changes (because of gamma), so hedges must be updated—this is dynamic hedging.

Delta hedging does not eliminate all risk: it removes first‑order price risk but leaves exposure to:

- larger moves (gamma risk)

- volatility changes (vega risk)

- time decay (theta risk)

Exam questions may ask which greek remains after delta hedging an options portfolio (answer: gamma, vega, and theta remain).

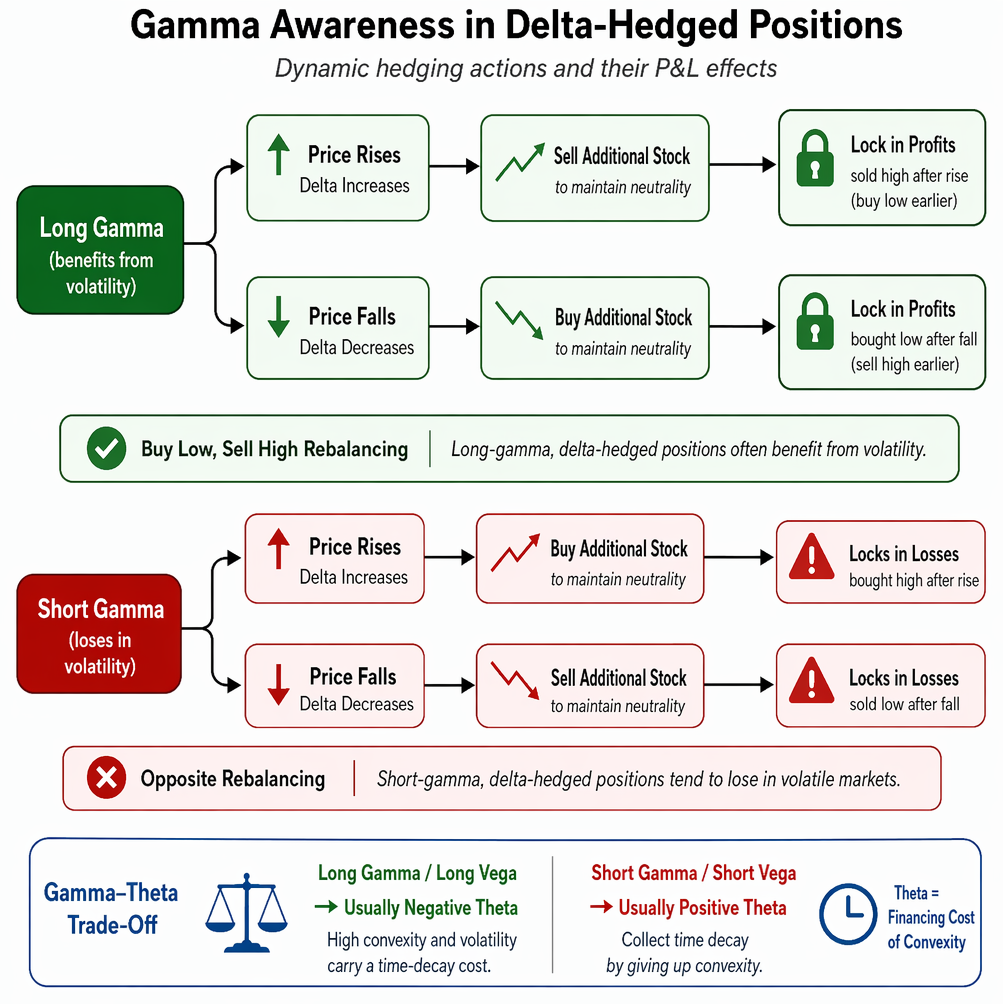

Gamma Awareness

High gamma positions—such as long straddles or near‑expiry ATM options—are sensitive to even small price moves.

For a trader who is long gamma and who delta‑hedges:

-

when the asset price rises:

- delta increases

- the trader must sell additional stock after a rise to maintain neutrality

- this tends to lock in profits (buy low earlier, sell high now)

-

when the asset price falls:

- delta decreases

- the trader must buy stock after a fall to maintain neutrality

- again, this tends to lock in profits (sell high earlier, buy low now)

In a volatile environment, this “buy low, sell high” rebalancing can generate trading profits; long‑gamma, delta‑hedged positions often benefit from realized volatility.

For a trader who is short gamma and delta‑hedges:

- the rebalancing is in the opposite direction:

- buying after price rises and selling after price falls

- this tends to lock in losses in volatile markets

Because gamma and theta are closely related, high positive gamma usually comes with large negative theta, and high negative gamma comes with positive theta. This reflects the fundamental trade‑off between convexity and time decay:

- long gamma / long vega → usually negative theta

- short gamma / short vega → usually positive theta

You can think of theta as the “financing cost” of convexity and volatility exposure.

Theta Management

Time decay is often the main cost or benefit of an options strategy:

- Long, multi‑leg positions (e.g., long straddles, long strangles, long butterflies) often have large negative theta. If the asset does not move as expected, losses accumulate purely from time passing.

- Income‑oriented strategies (e.g., covered calls, short puts, short straddles) often have positive theta: they profit from options expiring worthless, but they bear downside or tail risk.

Key points:

- Time decay accelerates as expiry approaches, particularly for ATM options.

- Strategies with large negative theta require the investor to be correct not only on direction or volatility, but also on timing.

- Positive‑theta strategies can perform well for a long time and then suffer large losses in rare events; exam wording such as “small, steady income with occasional large losses” describes short‑volatility, positive‑theta positions.

Theta interacts with other greeks:

- For a long call that is deep ITM, theta may be small in magnitude because most of the value is exercise value.

- For a long, near‑expiry ATM straddle, theta is very large in magnitude: the position loses time value quickly unless a big move happens soon.

Vega Sensitivity

Vega is important for volatility‑based trading and risk management.

Strategies with large positive vega include:

- long straddles and long strangles

- long calendar (time) spreads (buying longer‑dated options and selling shorter‑dated options)

- protective puts on existing stock holdings

These strategies:

- gain if implied volatility rises, even if the asset price does not move much

- lose if implied volatility falls, unless offset by directional gains

Strategies with negative vega include:

- short straddles and short strangles

- covered calls

- short calendar spreads (selling long‑dated options and buying short‑dated options)

These strategies:

- benefit if implied volatility falls

- are at risk if volatility rises sharply

For Level 1, the key classification is:

- Long volatility strategies: positive vega, usually positive gamma, negative theta (e.g., long call, long put, long straddle, long strangle, protective put).

- Short volatility strategies: negative vega, usually negative gamma, positive theta (e.g., short call, short put, covered call, short straddle, short strangle).

Recognizing this helps quickly identify which strategies are appropriate when a question describes expectations about volatility. For example:

- “Investor expects volatility to increase but has no strong directional view” → long straddle or long strangle.

- “Investor expects low volatility and wants income” → covered call or short strangle.

Greeks by Strategy: Quick Intuition

For the main strategies discussed:

-

Long call or long put:

- directional view (delta ≠ 0)

- long optionality (positive gamma and vega)

- negative theta (time decay cost)

-

Vertical spread (bull or bear):

- directional view but with limited risk and reward

- greeks smaller in magnitude because long and short legs partially offset

- reduced vega and gamma compared with a single long option

- theta often closer to zero than for a single long option (may be slightly negative or slightly positive)

-

Long straddle/strangle:

- little initial directional view (delta near zero)

- big bet on volatility (positive gamma, positive vega)

- large negative theta (time decay is costly)

-

Short straddle/strangle:

- little initial directional view

- short volatility and short gamma (exposed to large moves)

- large positive theta (collects premium)

-

Covered call:

- moderately bullish; reduces upside but provides some downside buffer from premium

- positive theta and negative vega (short volatility)

- net delta less than pure stock, negative gamma

-

Protective put:

- bullish with downside protection

- positive vega (insurance value increases with volatility)

- positive gamma (benefits from large downward moves relative to stock alone)

- negative theta (insurance cost)

Being able to characterize a strategy in terms of the signs of delta, gamma, theta, and vega is a fast way to interpret its risk profile under exam conditions.

Common Exam Pitfalls and Quick Checks

Some frequent traps in Level 1 questions:

-

Confusing vega with delta:

- delta relates to price of the reference asset

- vega relates to volatility

-

Forgetting to flip signs for short options:

- always reverse all greeks (delta, gamma, theta, vega) when moving from long to short

-

Misinterpreting “time decay”:

- long options usually lose value over time (negative theta)

- short options usually gain value over time (positive theta)

-

Ignoring moneyness:

- deep OTM or deep ITM options have small vega and gamma compared with ATM options

- delta for deep ITM options is near ±1; for deep OTM options, near 0

-

Ignoring contract size and number of contracts when aggregating greeks:

- portfolio greeks must account for how many options are held and the number of shares per contract

-

Mixing up per‑unit greeks and total greeks:

- if greeks are “per option,” multiply by contracts and contract size to get the position greek

-

Misreading question wording:

- “small change in price” → think delta (and possibly gamma)

- “change in expected volatility” → think vega

- “effect of time passing with no other change” → think theta

Quick checks:

- If a strategy is described as “benefiting from large moves in either direction” → think positive gamma and positive vega (long straddle, long strangle, protective positions).

- If a strategy is “earning income when the market is quiet” → think negative gamma, positive theta, negative vega (short options, covered call, short straddle/strangle).

- If a question asks about hedging small price movements but not volatility → think delta hedging.

Summary

Options strategies allow precise risk/return exposures, but effective management requires interpreting and combining the major greeks:

- Delta shows directional sensitivity and acts like the effective number of shares in an option.

- Gamma shows curvature or convexity: how delta itself changes as the asset price moves.

- Theta measures time decay, capturing how the option’s value erodes or benefits as expiry approaches.

- Vega measures volatility risk: how much the option’s price changes when implied volatility changes.

At CFA Level 1 it is important to:

- Describe the payoff and basic greek profile of common strategies (long/short calls and puts, spreads, straddles/strangles, covered calls, protective puts).

- Use given greek values to approximate the effect of small changes in price, volatility, or time on an option’s value.

- Aggregate greeks across positions to identify overall portfolio exposures and understand which risk dimensions dominate.

- Recognize the trade‑off between convexity/volatility exposure (gamma and vega) and time decay (theta).

- Identify whether a strategy is long or short volatility and whether it is mainly a directional bet or a volatility bet.

- Use delta hedging and awareness of gamma, theta, and vega to interpret hedging and risk‑management questions.

- Link moneyness and time to expiry to expected greek magnitudes (e.g., ATM near‑expiry options have high gamma and theta).

- Translate qualitative descriptions (“expects high volatility but no direction”, “wants to earn premium in a range‑bound market”) into appropriate strategies using greek intuition.

Understanding the sign and approximate magnitude of each greek for basic positions, and how these change with moneyness and time to expiry, allows quick elimination of incorrect answer choices and supports clear economic reasoning in options questions.

Key Point Checklist

This article has covered the following key knowledge points:

- Describe and compare major options trading strategies and their risk/return goals.

- Define and interpret delta, gamma, theta, and vega for CFA Level 1.

- Explain how the sign and magnitude of each greek depend on moneyness, time to expiry, and whether the position is long or short.

- Distinguish exercise value and time value and relate them to moneyness and volatility.

- Calculate simple greek‑based approximations for changes in option value under small moves in price, volatility, and time.

- Aggregate greek exposures for individual options and combined strategies to evaluate portfolio risk.

- Use greeks to analyze, hedge, and manage options strategies in dynamic markets, including delta‑hedging applications.

- Recognize the impact of time decay and volatility changes on strategies such as straddles, strangles, covered calls, and protective puts.

- Distinguish between long‑volatility and short‑volatility strategies using vega, gamma, and theta.

- Understand the relationship between gamma and convexity, and how high gamma affects the frequency of hedge rebalancing.

- Apply sign rules for greeks to quickly identify and eliminate incorrect answer options in multiple‑choice questions.

- Interpret exam wording that implicitly signals particular greek exposures or strategies.

Key Terms and Concepts

- options strategy

- greeks

- payoff diagram

- moneyness

- exercise value (option)

- time value (option)

- volatility

- implied volatility

- long position in an option

- short position in an option

- spread strategy

- straddle

- strangle

- covered call

- protective put

- delta

- delta of a portfolio

- delta hedging

- dynamic hedging

- delta‑neutral position

- gamma

- convexity (in options)

- theta

- vega

- long volatility position

- short volatility position