Learning Outcomes

This article explains investment policy statements (IPS) in portfolio construction, including:

- Defining the purpose and key functions of an IPS for individual and institutional investors.

- Describing how an IPS links client circumstances, objectives, and constraints to portfolio strategy and asset allocation.

- Distinguishing between return objectives and risk tolerance, and showing how they are expressed and justified in exam-style IPS questions.

- Classifying the primary constraint types—liquidity, time horizon, tax, legal/regulatory, and unique—and evaluating how each influences suitable asset mixes.

- Outlining the structured process for drafting, reviewing, and revising an IPS, from initial fact-finding to ongoing monitoring.

- Applying IPS concepts to CFA Level 1 item sets by identifying missing information, spotting inconsistent objectives or constraints, and proposing appropriate portfolio responses.

- Interpreting worked examples that highlight common exam traps, such as confusing risk tolerance with investment experience or overlooking multi-stage time horizons.

- Using the IPS as a reference framework for performance evaluation, risk control, and documenting investment decisions in a professional, standards-consistent manner.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the role of the investment policy statement within portfolio management, its typical components, and how various constraints and objectives inform the selection, monitoring, and construction of portfolios, with a focus on the following syllabus points:

- Describe the purposes, benefits, and structure of an investment policy statement (IPS).

- Distinguish between investment objectives (return and risk) and investment constraints (liquidity, time horizon, tax, legal/regulatory, and unique).

- Identify how client circumstances and preferences affect the IPS and portfolio construction.

- Explain the process of formulating, revising, and applying an IPS in a wealth or institutional context.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Name two major client constraints that must typically be identified and documented in an investment policy statement.

- True or false? An IPS should always specify the return objective as a specific annual percentage.

- Briefly describe the difference between a risk objective and a risk constraint in an IPS.

- Give one example each of a legal and a unique constraint for an investor.

Introduction

The investment policy statement (IPS) forms the core document governing portfolio management and construction for individual and institutional clients. It clarifies the client’s objectives, documents all critical constraints, and provides a consistent reference for long-term investment decision making, monitoring, and evaluation. The IPS translates a client's circumstances, preferences, and goals into practical, actionable guidance for portfolio construction and ongoing review.

Key Term: investment policy statement (IPS)

A formal written document articulating an investor’s return objectives, risk tolerance, constraints, and overall investment strategy, serving as the basis for all portfolio management decisions.Test Tip: When revising Investment policy statement and constraints, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Role and Principles of the Investment Policy Statement

An effective IPS is client-specific and must be tailored to the needs and context of each individual or institution. It anchors portfolio construction and monitoring, serving as both a strategic guide and a risk-control tool. For private wealth and institutional clients, a robust IPS:

- Establishes the investment objectives (risk and return).

- Identifies all key constraints.

- Details governance, roles, and responsibilities.

- Specifies strategic asset allocation frameworks.

- Outlines procedures for review and revisions.

The IPS must strike a balance between specificity—providing clear guidance for the manager—and flexibility, allowing for some professional judgment in response to changing markets or circumstances.

Key Components of the IPS

The following elements make up a standard IPS and should appear in some form in all CFA exam scenarios:

Objectives: Return and Risk

- Return Objective: The required or desired return, which considers such factors as inflation, withdrawals, capital growth, and the investor’s real goals. It may be expressed in terms of absolute values, relative benchmarks, or as a minimum necessary rate to achieve client aims.

- Risk Tolerance: The degree of portfolio volatility, loss, or probability of shortfall a client can financially and psychologically withstand. The risk objective is shaped by both client preferences and financial circumstances.

Key Term: risk tolerance

The maximum degree of risk an investor is both willing and able to bear, determined by goals, financial capacity, investment knowledge, and psychological comfort with loss or fluctuations.

Typical Constraints in an IPS

Constraints document all limitations that may affect asset allocation, portfolio construction, trading, or ongoing management. The CFA curriculum recognizes five primary constraint types:

Liquidity

The need for cash to meet spending, withdrawals, liabilities, or emergencies. Higher liquidity needs generally require portfolios to hold larger proportions of cash or low-volatility assets.

Key Term: liquidity constraint

A limitation arising from the investor’s need to convert assets into cash quickly or regularly, with minimal impact on value. Key Term: time horizon constraint

The length of time until the assets will be needed for spending, distribution, or liquidation. Shorter horizons generally increase the need for less risky, more liquid portfolios. Key Term: tax constraint

Any feature of the investor's situation that affects the tax treatment of returns or investments—such as income tax rates, capital gains taxes, or tax-exempt status. Key Term: legal/regulatory constraint

Limitations on investment caused by laws, regulations, or legal status—for example, restrictions imposed by pension or trust law, or by charitable status. Key Term: unique constraint

Any client-specific factor not covered under other headings, such as ethical preferences, religious exclusions, or employer-related investment restrictions.

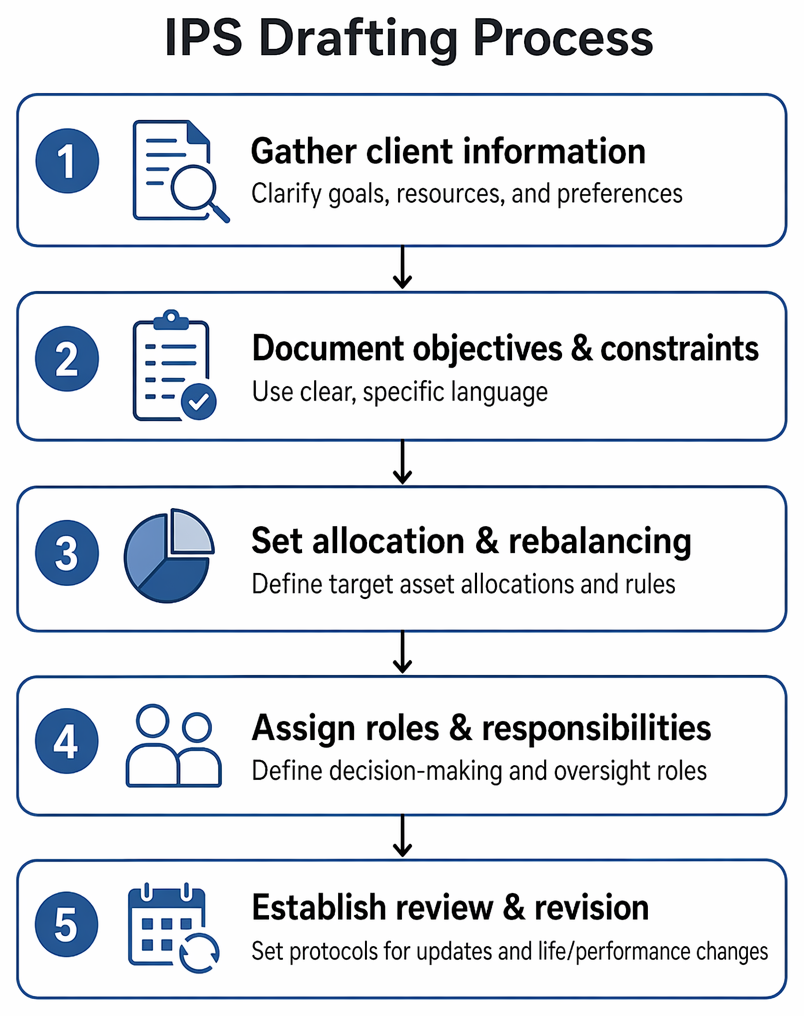

The IPS Drafting Process

A strong IPS will usually be drafted after fact-finding and interviews, involving:

Investment policy statement structure separates objectives from client constraints and identifies the principal constraint categories used in portfolio construction.

- Gathering all relevant client data and clarifying goals, resources, and preferences.

- Documenting objectives and constraints using clear, specific language.

- Setting target asset allocations and rebalancing rules.

- Assigning roles and responsibilities for investment decisions and oversight.

- Establishing review and revision protocols in response to life changes or investment performance.

Worked Example 1.1

A private client, age 55, is planning for retirement in 10 years, has $2 million in investable assets, requires $50,000 yearly withdrawals starting at retirement, is risk-averse, and cannot hold investments in alcohol or tobacco companies due to personal beliefs. Identify the key IPS objectives and constraints.

Answer:

The return objective is to provide sustainable withdrawals and maintain the real value of capital over a 10-year accumulation and subsequent decumulation phase. The risk objective should reflect high risk aversion and willingness to accept lower return for stability. Constraints: liquidity for future withdrawals, a dual-stage time horizon (accumulation and decumulation), tax considerations (if investments are taxable accounts), legal (if subject to trust or regulatory rules), and a unique constraint (ethical exclusion of alcohol and tobacco investments).Exam Warning: A common CFA exam error is to confuse a client's "lack of experience" with a true risk tolerance constraint. Distinguish between willingness (attitude) and ability (capacity) to bear risk—both must be specifically addressed and objectively documented in the IPS.

Applying the IPS in Portfolio Construction and Analytics

The IPS provides the basis for asset allocation and portfolio construction. Every investment decision must be consistent with documented objectives and constraints. Asset selection, manager choice, and performance measurement always refer back to the IPS. Periodic reviews test compliance, performance, and relevance as client circumstances change.

Worked Example 1.2

Question: Suppose a charitable endowment's IPS states: "Objective—preserve real value; spend 4% of assets per year." The portfolio earns 5% nominal, inflation is 3%. Did the portfolio meet the IPS objective?

Answer:

The real return is approximately 2% (5% nominal – 3% inflation), less than the 4% spending rate. The portfolio did not meet the IPS’s real value preservation objective, because the fund is spending more than the real return, reducing real capital over time.

Summary

A well-crafted IPS is essential in portfolio management. It defines the client’s objectives and all critical constraints, controls risk, and provides discipline for constructing, monitoring, and revising portfolios. The IPS is fundamental for professional conduct and examination performance.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify the core purposes and benefits of the investment policy statement (IPS).

- Distinguish between return objectives and risk tolerance.

- List and classify the five primary types of constraints: liquidity, time horizon, tax, legal/regulatory, unique.

- Apply the IPS drafting process: gather information, document objectives/constraints, specify allocation, set review procedures.

- Understand the IPS as the strategic anchor for portfolio construction, review, and monitoring.

Key Terms and Concepts

- investment policy statement (IPS)

- risk tolerance

- liquidity constraint

- time horizon constraint

- tax constraint

- legal/regulatory constraint

- unique constraint